brk = pd.read_csv('data/MacroTrends_Data_Download_BRK.A.csv', skiprows = 14) # skipping the first 14 rows8 Time Series

8.1 What is time series?

Time series analysis is used for non-stationary data—things that are constantly fluctuating over time or are affected by time. Industries like finance, retail, and economics frequently use time series analysis because currency and sales are always changing. Stock market analysis is an excellent example of time series analysis in action, especially with automated trading algorithms. Likewise, time series analysis is ideal for forecasting weather changes, helping meteorologists predict everything from tomorrow’s weather report to future years of climate change. Examples of time series analysis in action include:

- Weather data

- Rainfall measurements

- Temperature readings

- Heart rate monitoring (EKG)

- Brain monitoring (EEG)

- Quarterly sales

- Stock prices

- Automated stock trading

- Industry forecasts

- Interest rates

There are two main types of time series forecasting.

Univariate Time Series Forecasting:

- Uses only the previous values of the time series to predict its future values.

- Example: t-1, t-2, t-3

Multivariate Time Series Forecasting:

- Uses predictors other than the series (exogenous variables) to forecast.

- Example: to predict the number of bicycle rides: temperature, city, etc.

Example 1

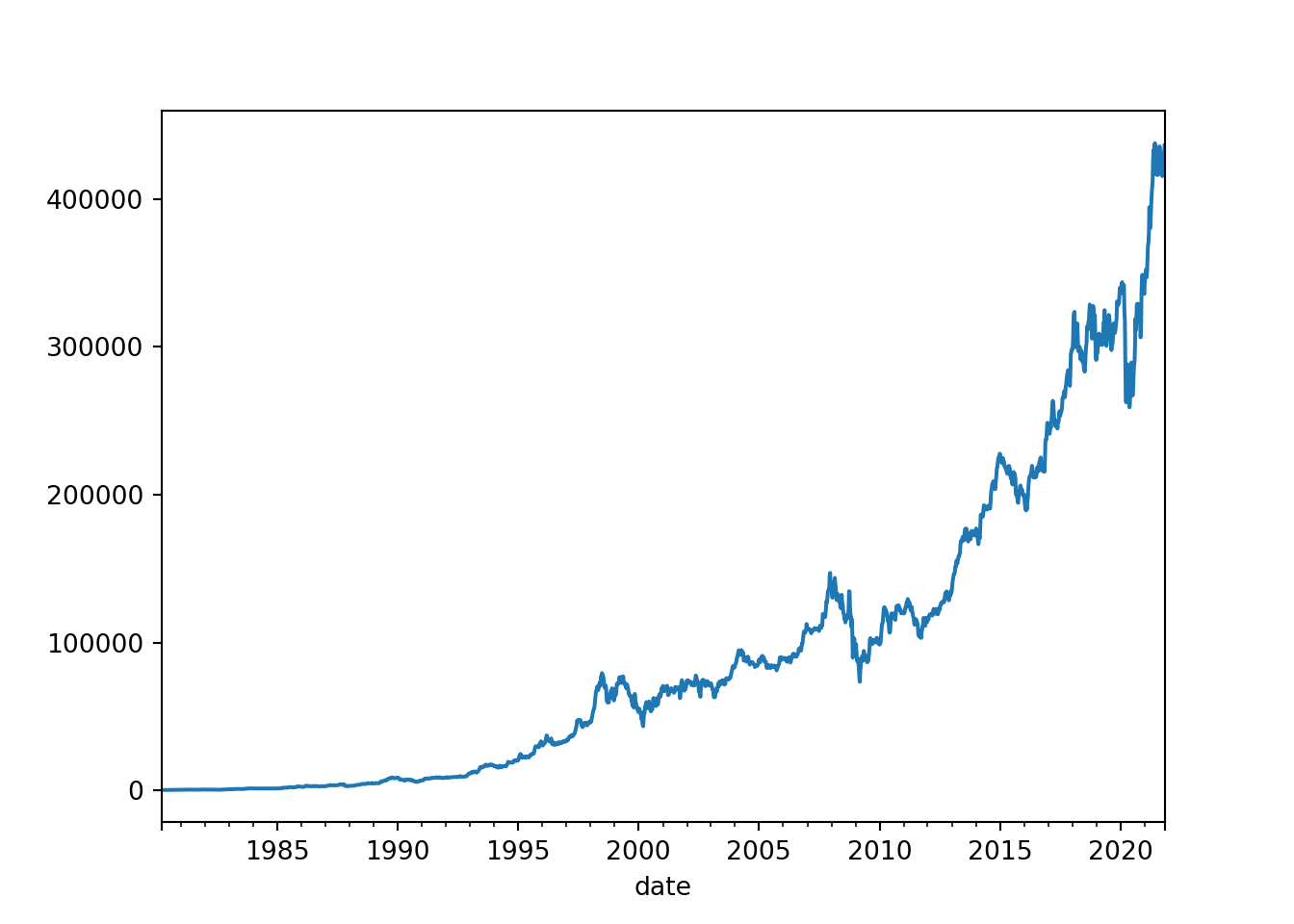

The first dataset we will be using is from this website: https://www.macrotrends.net/stocks/charts/BRK.A/berkshire-hathaway/stock-price-history. It is the stock price history from the last 44 years of a company called Berkshire Hathaway.

brk.head() date open high low close volume

0 1980-03-17 290.0 310.0 290.0 290.0 10000

1 1980-03-18 290.0 290.0 290.0 290.0 0

2 1980-03-19 290.0 310.0 290.0 290.0 20000

3 1980-03-20 290.0 290.0 290.0 290.0 0

4 1980-03-21 290.0 290.0 290.0 290.0 0# information about the dataset

brk.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 10498 entries, 0 to 10497

Data columns (total 6 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 date 10498 non-null object

1 open 10498 non-null float64

2 high 10498 non-null float64

3 low 10498 non-null float64

4 close 10498 non-null float64

5 volume 10498 non-null int64

dtypes: float64(4), int64(1), object(1)

memory usage: 492.2+ KB8.2 Date formatting

As a recap: https://docs.python.org/3/library/datetime.html#strftime-and-strptime-behavior

# converting the date column to the datetime format

brk['date'] = pd.to_datetime(brk['date'], format ='%Y-%m-%d')brk.info() # note the change of datatype for `date`<class 'pandas.core.frame.DataFrame'>

RangeIndex: 10498 entries, 0 to 10497

Data columns (total 6 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 date 10498 non-null datetime64[ns]

1 open 10498 non-null float64

2 high 10498 non-null float64

3 low 10498 non-null float64

4 close 10498 non-null float64

5 volume 10498 non-null int64

dtypes: datetime64[ns](1), float64(4), int64(1)

memory usage: 492.2 KB8.3 Time series structure

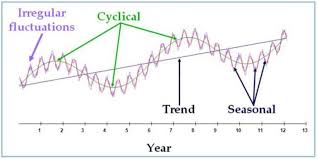

8.3.1 Cycles

A seasonal pattern exists when a series is influenced by seasonal factors (e.g., the quarter of the year, the month, or day of the week). Seasonality is always of a fixed and known period. Hence, seasonal time series are sometimes called periodic time series.

A cyclic pattern exists when data exhibit rises and falls that are not of fixed period. The duration of these fluctuations is usually of at least 2 years. Think of business cycles which usually last several years, but where the length of the current cycle is unknown beforehand.

Many people confuse cyclic behaviour with seasonal behaviour, but they are really quite different. If the fluctuations are not of fixed period then they are cyclic; if the period is unchanging and associated with some aspect of the calendar, then the pattern is seasonal. In general, the average length of cycles is longer than the length of a seasonal pattern, and the magnitude of cycles tends to be more variable than the magnitude of seasonal patterns.

Example 2

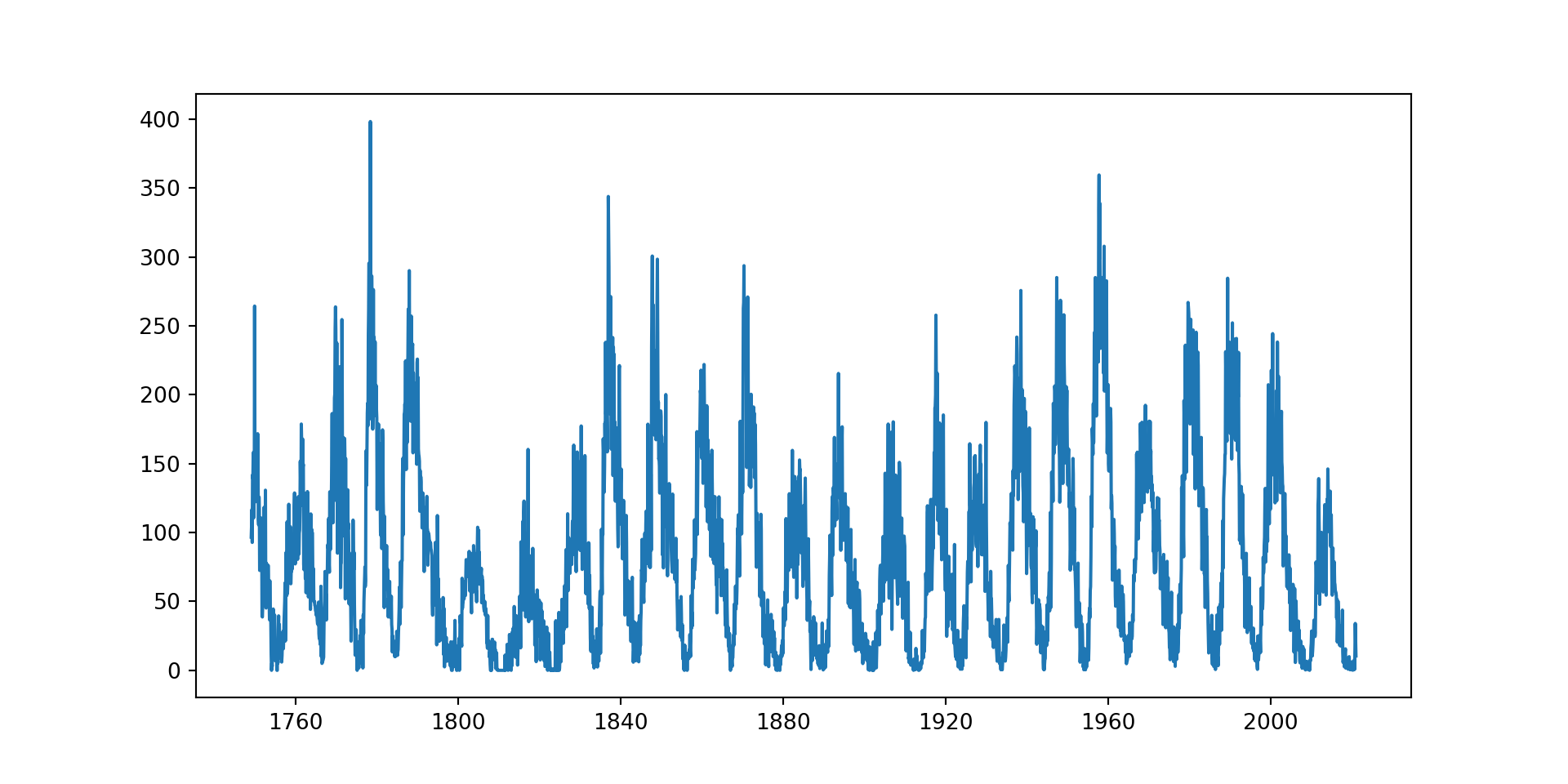

# read in sunspots data

sunspots = pd.read_csv('data/sunspots.csv')

sunspots.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 3265 entries, 0 to 3264

Data columns (total 3 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Unnamed: 0 3265 non-null int64

1 Date 3265 non-null object

2 Monthly Mean Total Sunspot Number 3265 non-null float64

dtypes: float64(1), int64(1), object(1)

memory usage: 76.7+ KB# convert date column to datetime

sunspots['Date'] = pd.to_datetime(sunspots['Date'])# plotting the time series graph

plt.figure(figsize = (10,5))

plt.plot(sunspots['Date'], # x axis

sunspots['Monthly Mean Total Sunspot Number']) # y axis

Data that are truly periodic have a behavior that repeats exactly over a fixed time frame.

Example 3

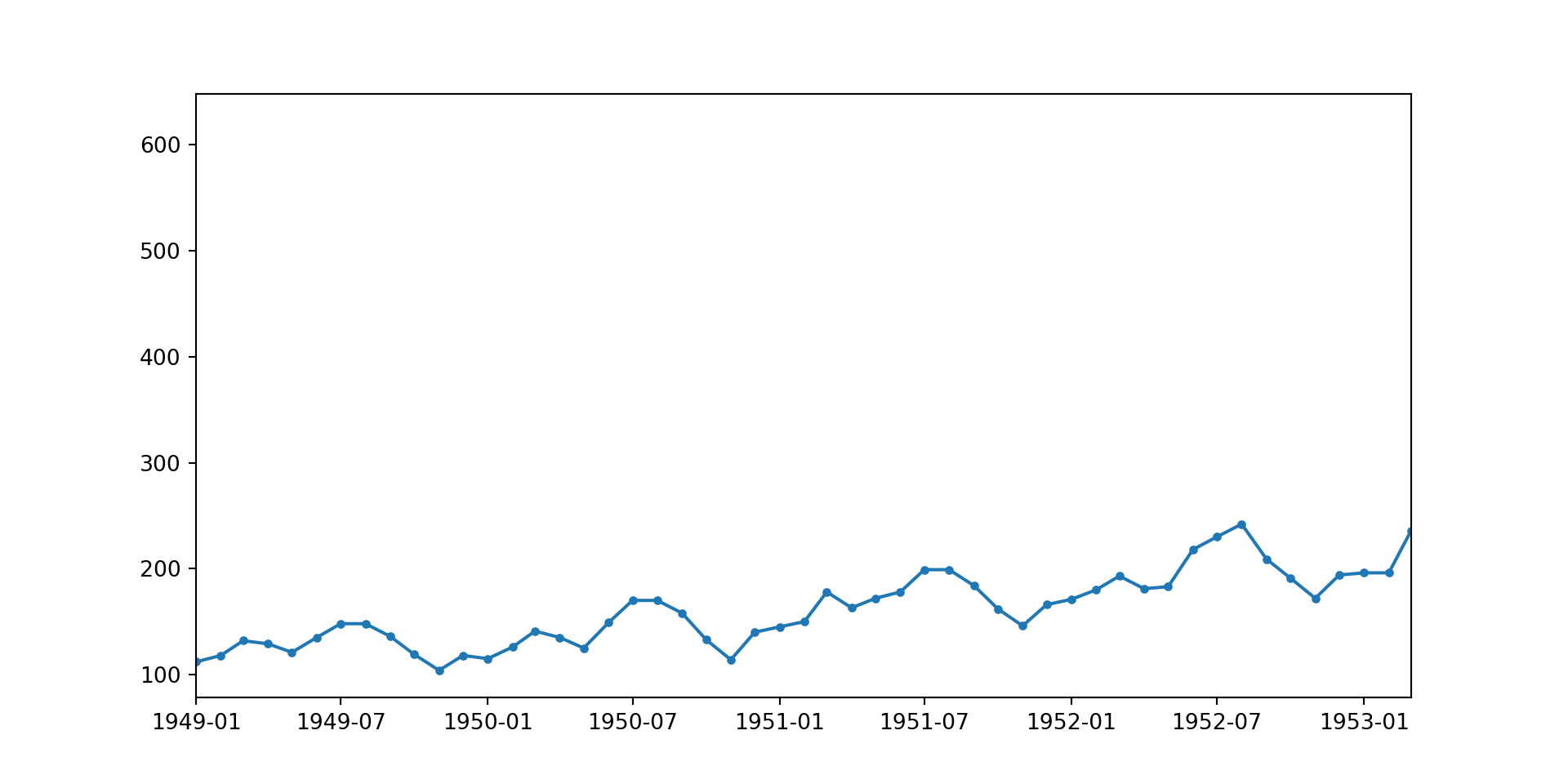

# read in airpass data

airpass = pd.read_csv('data/AirPassengers.csv')

airpass.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 144 entries, 0 to 143

Data columns (total 2 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Month 144 non-null object

1 #Passengers 144 non-null int64

dtypes: int64(1), object(1)

memory usage: 2.4+ KBairpass.head() Month #Passengers

0 1949-01 112

1 1949-02 118

2 1949-03 132

3 1949-04 129

4 1949-05 121# convert date column to datetime

airpass['Month'] = pd.to_datetime(airpass['Month'])

airpass.head() Month #Passengers

0 1949-01-01 112

1 1949-02-01 118

2 1949-03-01 132

3 1949-04-01 129

4 1949-05-01 121plt.figure(figsize = (10,5))

plt.plot(airpass['Month'], airpass['#Passengers'], marker = '.')

plt.xlim(left = airpass['Month'][0], right = airpass['Month'][50])(-7670.0, -6150.0)

# plt.axvline(airpass['Month'][12], color = 'red', ls = '--', lw = 0.5)

# plt.axvline(airpass['Month'][24], color = 'red', ls = '--', lw = 0.5)

# plt.axvline(airpass['Month'][36], color = 'red', ls = '--', lw = 0.5)

# plt.axvline(airpass['Month'][48], color = 'red', ls = '--', lw = 0.5)

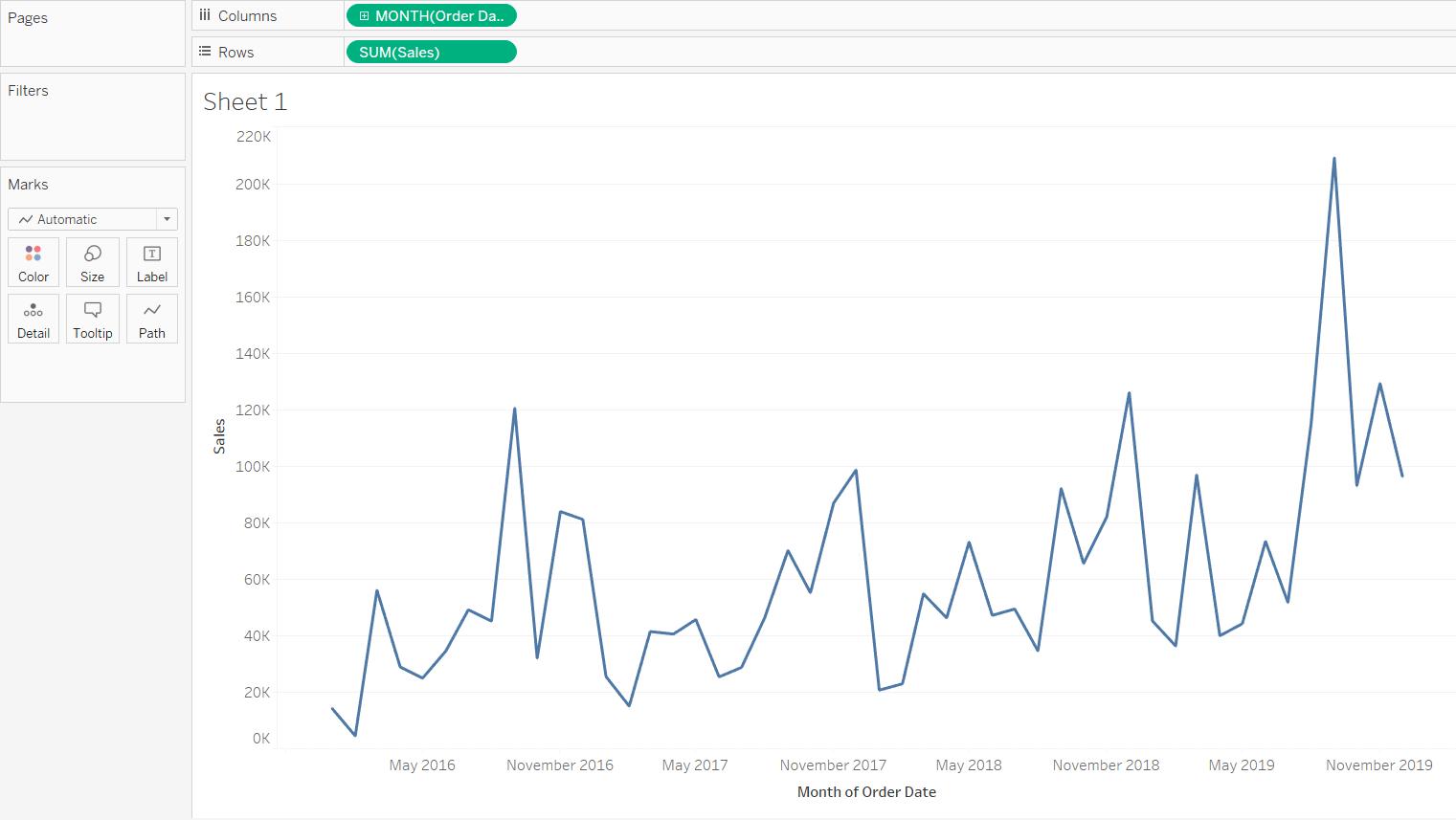

The cyclic behavior of the air passenger data is repeated on an annual basis. This can be better visualised by uncommenting the last four lines in the code cell above.

The data suggests cyclic growth in travel with peaks likely during popular travel months (July, August).

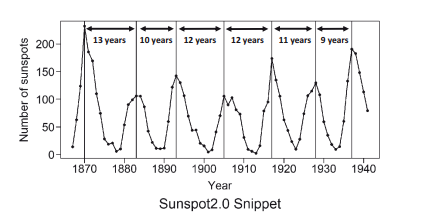

Example 2 showed seasonality over 12 years, and example 3 showed seasonality over 1 year. It’s also possible to have seasonality over a month, for example you might have higher sales at the beginning and end of a month and less sales in the middle of the month. Seasonality could also occur over a week, where a call centre receives more calls on a Monday and less calls on a Friday, and it could also occur over a day, where traffic data shows high volume of cars in the morning and late afternoon, and low volume of cars in the middle of the night.

It’s important to identify the seasonality in your dataset to allow you to recognise the level of granularity needed for your time series model.

8.3.2 Trends

In time series analysis, a trend represents the general direction in which the data moves over time. It is a pattern that persists over a long period, regardless of short-term fluctuations.

a) Linear Trend

This is a straightforward, consistent upward or downward movement at a steady rate. It can be represented by a straight line when plotted on a graph, indicating a constant increase or decrease over time.

b) Exponential Trend

Characterised by data that increases or decreases at an increasingly higher rate. On a graph, this is shown as a curve that moves away from the baseline more and more sharply as time progresses. It’s common in phenomena that spread rapidly, like viral internet content or population growth in certain conditions.

c) Downward Trend

This is a specific type of trend where the data is consistently decreasing over time. It can be linear, with a steady rate of decline, or it can be exponential, with the rate of decline accelerating as time goes on.

d) Random Walk

This describes a time series that moves up and down seemingly at random, without any long-term direction. This type of data can be challenging to predict and may often require more sophisticated models to understand any underlying structure that isn’t immediately apparent.

8.4 Date as an index

For time series, specifically the ARIMA model, the date needs to be converted to an index.

# before

brk.head() date open high low close volume

0 1980-03-17 290.0 310.0 290.0 290.0 10000

1 1980-03-18 290.0 290.0 290.0 290.0 0

2 1980-03-19 290.0 310.0 290.0 290.0 20000

3 1980-03-20 290.0 290.0 290.0 290.0 0

4 1980-03-21 290.0 290.0 290.0 290.0 0# after

brk = brk.set_index('date') # specify the column that needs to be indexed

brk.head() open high low close volume

date

1980-03-17 290.0 310.0 290.0 290.0 10000

1980-03-18 290.0 290.0 290.0 290.0 0

1980-03-19 290.0 310.0 290.0 290.0 20000

1980-03-20 290.0 290.0 290.0 290.0 0

1980-03-21 290.0 290.0 290.0 290.0 0This allows us to select specific dates from the index to use for analysis.

# example: select dates from 10th September 2008 to 20th September 2008

brk['2008-09-10':'2008-09-20'] open high low close volume

date

2008-09-10 118500.0 118500.0 117000.0 117000.0 59600

2008-09-11 116200.0 117500.0 115500.0 117500.0 52000

2008-09-12 116700.0 119500.0 116310.0 119500.0 86500

2008-09-15 117000.0 123100.0 115500.0 119900.0 223200

2008-09-16 119000.0 125010.0 118300.0 125000.0 256200

2008-09-17 125000.0 125600.0 122900.0 124800.0 180000

2008-09-18 126000.0 128900.0 121310.0 128010.0 276500

2008-09-19 130000.0 147000.0 127901.0 147000.0 422800Indexing the date also impacts the output of brk.info(). It will give us the range of dates in the dataset.

brk.info()<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 10498 entries, 1980-03-17 to 2021-10-29

Data columns (total 5 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 open 10498 non-null float64

1 high 10498 non-null float64

2 low 10498 non-null float64

3 close 10498 non-null float64

4 volume 10498 non-null int64

dtypes: float64(4), int64(1)

memory usage: 750.1 KBExamine the dates from the output above. What is missing? It seems to be the days that correspond with the weekend, which makes sense, as the stock markets aren’t open.

8.5 Filling data gaps

For our model to be effective, we need to have consecutive dates, because the model assumes the points are evenly spaced over time. If not, this implies there are missing values and can distort the model’s understanding.

When forecasting, irregular intervals could lead to misleading results because the model may not correctly attribute changes in the data to either trends or seasonality.

brk[4:6] # can view the missing weekend open high low close volume

date

1980-03-21 290.0 290.0 290.0 290.0 0

1980-03-24 290.0 290.0 270.0 270.0 10000We can use the .resample() method for frequency conversion and resampling of time series data. We can also use .asfreq() which allows the datetime index to have a different frequency, while keeping the same values at the current index.

Link to resample documentation`

brk[4:6].resample('1d').asfreq() # specify 1 day open high low close volume

date

1980-03-21 290.0 290.0 290.0 290.0 0.0

1980-03-22 NaN NaN NaN NaN NaN

1980-03-23 NaN NaN NaN NaN NaN

1980-03-24 290.0 290.0 270.0 270.0 10000.0Now, the missing dates have been added, but we are missing data for the four columns in the dataset.

First we will apply the above function to the entire dataset.

# apply .resample() to whole dataset

brk_resampled = brk.resample('1d').asfreq()brk_resampled open high low close volume

date

1980-03-17 290.00 310.00 290.00 290.0 10000.0

1980-03-18 290.00 290.00 290.00 290.0 0.0

1980-03-19 290.00 310.00 290.00 290.0 20000.0

1980-03-20 290.00 290.00 290.00 290.0 0.0

1980-03-21 290.00 290.00 290.00 290.0 0.0

... ... ... ... ... ...

2021-10-25 435962.98 437144.50 433064.07 436401.0 1793.0

2021-10-26 437165.12 439849.99 435446.02 437890.0 1902.0

2021-10-27 437526.91 439229.22 433050.00 433050.0 3228.0

2021-10-28 434702.73 436873.99 432516.47 436249.5 2409.0

2021-10-29 435052.79 436511.89 431713.81 432902.0 2072.0

[15202 rows x 5 columns]We can also plot this data. As we have ‘date’ as an index, we can select any other column and a line plot will be returned.

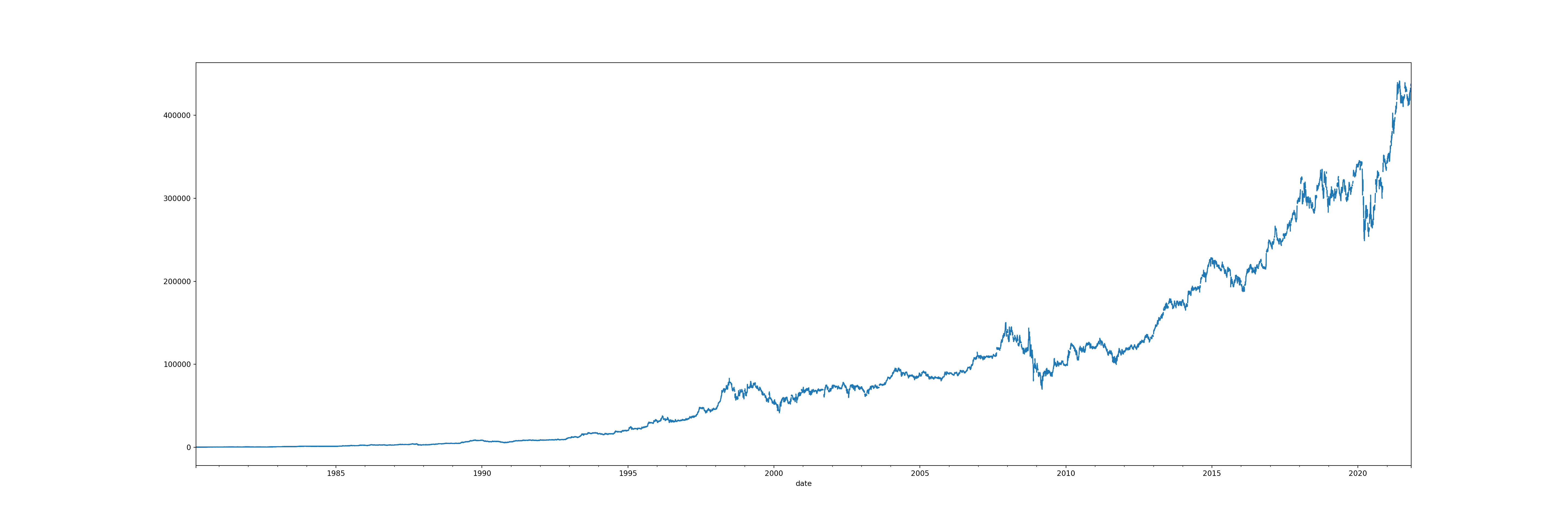

# plot 'open' over time

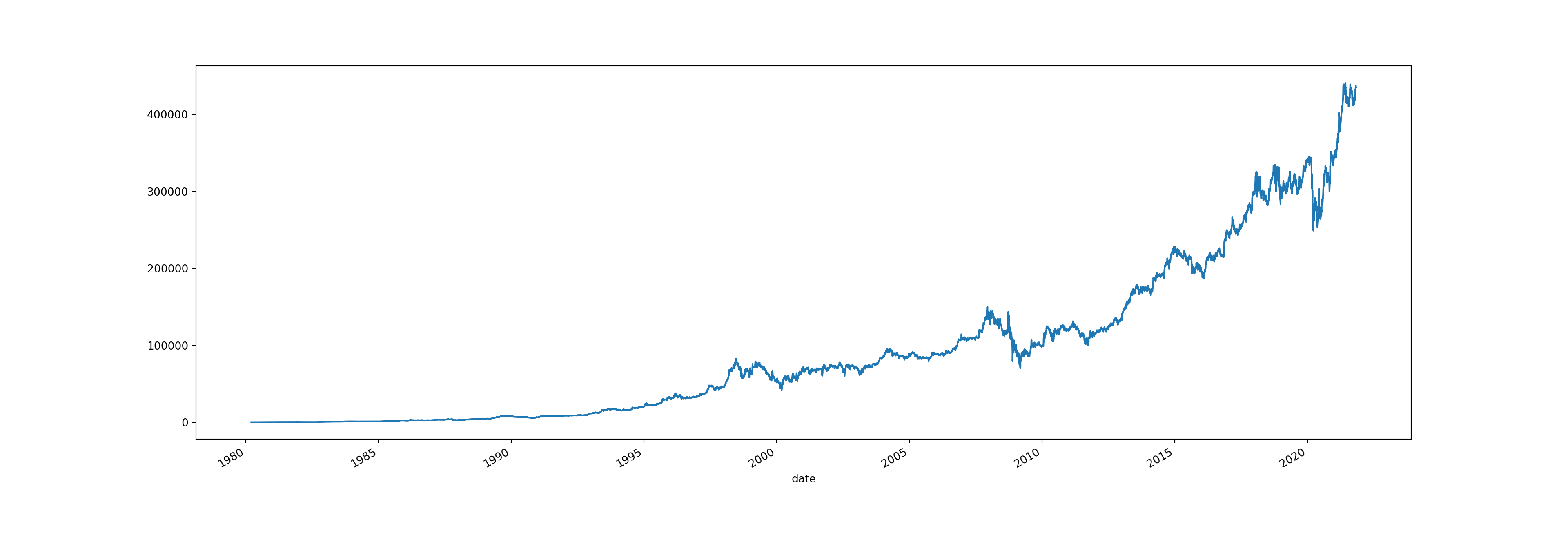

brk_resampled['open'].plot(figsize = (30, 10))

However, double clicking on the graph, we can see there are some gaps - this is where the weekend missing values are. The next step will be to solve this problem.

We have the following options:

.pad()- pads the data with the previous valid values. (forward filling).bfill()- The backward fill will replace NaN values that appeared in the resampled data with the next value in the original sequence. Missing values that existed in the original data will not be modified..ffill()- Forward fill the values.

# resampling with .pad()

brk_filled = brk[4:6].asfreq('1d', method='pad')

brk_filled open high low close volume

date

1980-03-21 290.0 290.0 290.0 290.0 0

1980-03-22 290.0 290.0 290.0 290.0 0

1980-03-23 290.0 290.0 290.0 290.0 0

1980-03-24 290.0 290.0 270.0 270.0 10000# resampling with .bfill()

brk[4:6].resample('1d').bfill() open high low close volume

date

1980-03-21 290.0 290.0 290.0 290.0 0

1980-03-22 290.0 290.0 270.0 270.0 10000

1980-03-23 290.0 290.0 270.0 270.0 10000

1980-03-24 290.0 290.0 270.0 270.0 10000# using .bfill() on the resampled data

brk_resampled_bfill = brk_resampled.bfill()

brk_resampled_bfill open high low close volume

date

1980-03-17 290.00 310.00 290.00 290.0 10000.0

1980-03-18 290.00 290.00 290.00 290.0 0.0

1980-03-19 290.00 310.00 290.00 290.0 20000.0

1980-03-20 290.00 290.00 290.00 290.0 0.0

1980-03-21 290.00 290.00 290.00 290.0 0.0

... ... ... ... ... ...

2021-10-25 435962.98 437144.50 433064.07 436401.0 1793.0

2021-10-26 437165.12 439849.99 435446.02 437890.0 1902.0

2021-10-27 437526.91 439229.22 433050.00 433050.0 3228.0

2021-10-28 434702.73 436873.99 432516.47 436249.5 2409.0

2021-10-29 435052.79 436511.89 431713.81 432902.0 2072.0

[15202 rows x 5 columns]brk_resampled_bfill.info()<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 15202 entries, 1980-03-17 to 2021-10-29

Freq: D

Data columns (total 5 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 open 15202 non-null float64

1 high 15202 non-null float64

2 low 15202 non-null float64

3 close 15202 non-null float64

4 volume 15202 non-null float64

dtypes: float64(5)

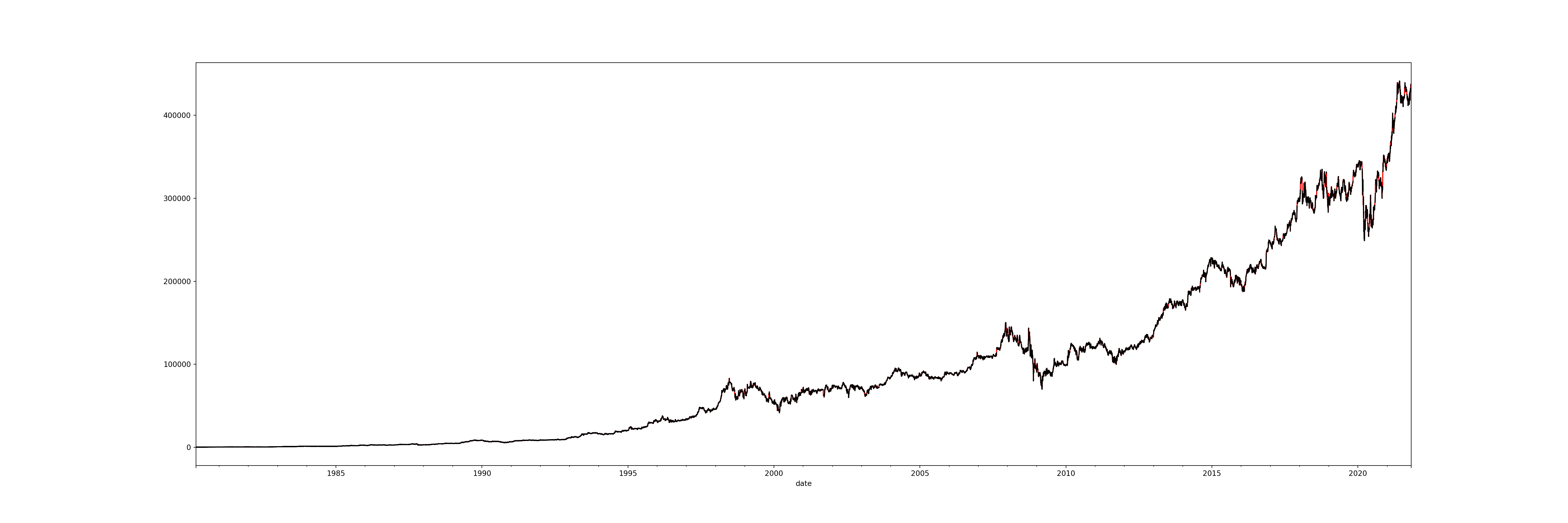

memory usage: 712.6 KBbrk_resampled_bfill['open'].plot(figsize=(30, 10), color='red') # new data

brk_resampled['open'].plot(figsize=(30, 10), color='black') # old data

With the red line as the new data and the black line as the old data, we can see that all the gaps have now been covered.

The above is one method we can use to fill in missing values, but there are others which may be more effective.

Ways to fill the missing values:

- with the nearest value

- with the mean, median, most frequent value

- with the predictions of a regressor model (using linear regression to predict the missing values)

- by using the interpolation technique

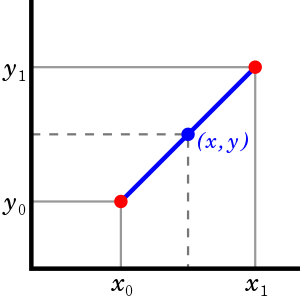

For example, one of the interpolation methods available is linear interpolation. Linear interpolation can be used to input missing data by drawing a straight line between the two points surrounding the missing value(in time series: it looks at prior past value and the next future value to draw a line between them).

A polynomial interpolation will attempt to draw a curved line between the two points.

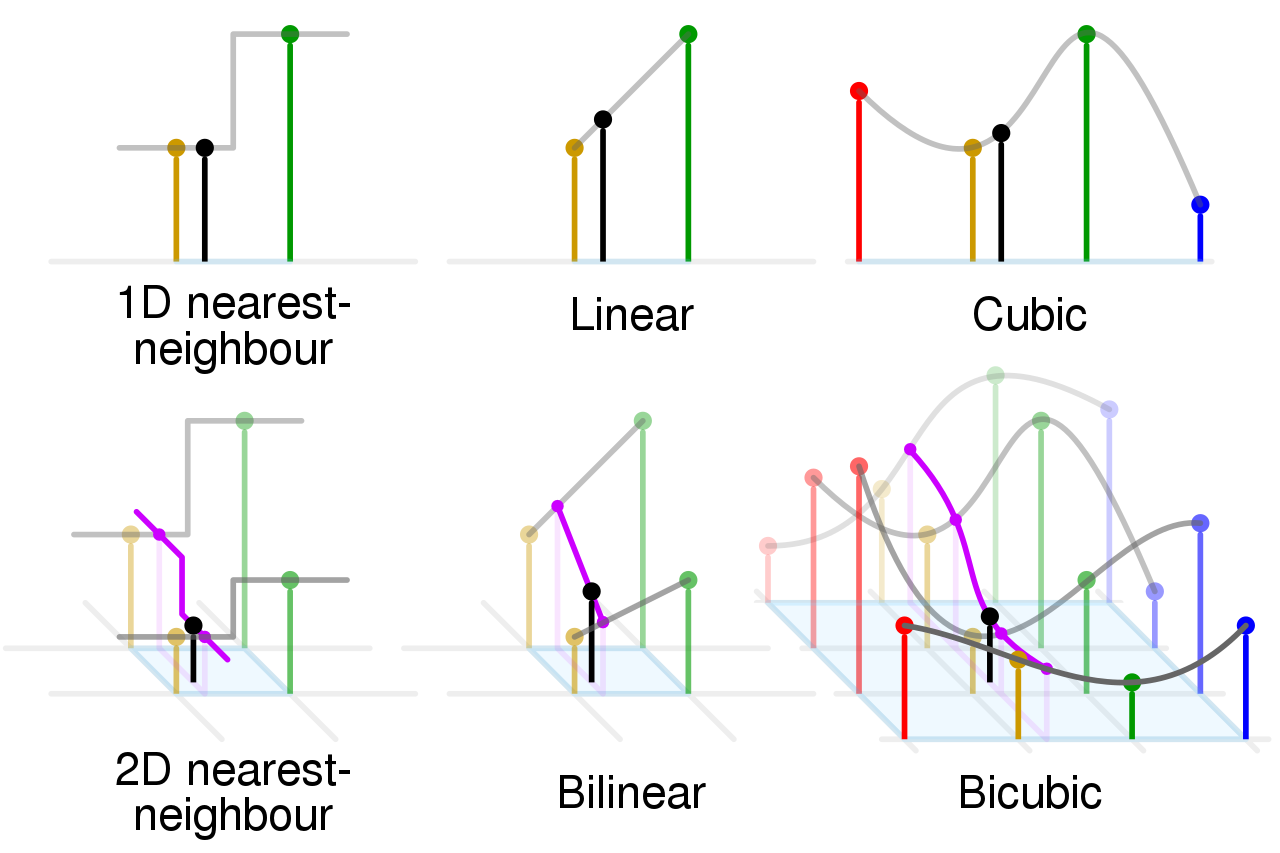

1D Nearest-Neighbour: Assigns the value of the nearest data point to a given x-value without considering the other points. It results in a step-like graph where the interpolated value abruptly changes at the midpoint between neighbouring data points.

Linear: Draws a straight line between two adjacent data points and uses this line to estimate intermediate values. This results in a piecewise linear graph.

Cubic: Uses cubic polynomials to connect the data points, creating a smoother curve than linear interpolation. It takes into account more neighbouring points, which often results in a smoother and more natural-looking curve.

2D Nearest-Neighbour: This technique is an extension of the 1D nearest-neighbour to two dimensions. It assigns the value of the nearest data point to a given (x, y) position, resulting in a block-like pattern in the interpolated surface.

Bilinear: Extends the concept of linear interpolation to two dimensions. It interpolates linearly in both the x and y directions by taking the four nearest grid points to create a smooth surface.

Bicubic: Similar to cubic interpolation in 1D, bicubic interpolation in 2D uses 16 nearby points to estimate the value at a given (x, y) position, resulting in a much smoother surface than both the nearest-neighbour and bilinear methods.

# interpolating the 'open' column using linear

brk_resampled['open_linear'] = brk_resampled['open'].interpolate('linear')

# 'quadratic', 'nearest', 'cubic'brk_resampled_bfill['open'].plot(figsize = (30, 10), color='black') # old data

brk_resampled['open_linear'].plot(figsize = (30, 10), color='red') # new data

Although there is not a big difference visible, there will be a much larger difference when your dataset has multiple missing values, especially if they are very close to one another.

8.6 Resampling

We can reduce the granularity of the data even further, for example by breaking it down into periods of 6 hours.

# view two days worth of data

brk[2:4] open high low close volume

date

1980-03-19 290.0 310.0 290.0 290.0 20000

1980-03-20 290.0 290.0 290.0 290.0 0# resample to periods of 6 hours

brk[2:4].resample('6h').asfreq() open high low close volume

date

1980-03-19 00:00:00 290.0 310.0 290.0 290.0 20000.0

1980-03-19 06:00:00 NaN NaN NaN NaN NaN

1980-03-19 12:00:00 NaN NaN NaN NaN NaN

1980-03-19 18:00:00 NaN NaN NaN NaN NaN

1980-03-20 00:00:00 290.0 290.0 290.0 290.0 0.08.7 Downsampling

We can also do the opposite process, to decrease the granularity of the data. Instead of daily data, we may wish to view our data in 1 week bins. This would sum the values of the timestamps falling into a bin.

# view first 2 weeks

brk[:15] open high low close volume

date

1980-03-17 290.0 310.0 290.0 290.0 10000

1980-03-18 290.0 290.0 290.0 290.0 0

1980-03-19 290.0 310.0 290.0 290.0 20000

1980-03-20 290.0 290.0 290.0 290.0 0

1980-03-21 290.0 290.0 290.0 290.0 0

1980-03-24 290.0 290.0 270.0 270.0 10000

1980-03-25 270.0 270.0 270.0 270.0 0

1980-03-26 270.0 270.0 270.0 270.0 0

1980-03-27 270.0 270.0 270.0 270.0 0

1980-03-28 270.0 270.0 270.0 270.0 0

1980-03-31 270.0 280.0 260.0 260.0 10000

1980-04-01 260.0 280.0 260.0 260.0 30000

1980-04-02 260.0 260.0 260.0 260.0 0

1980-04-03 260.0 280.0 260.0 260.0 10000

1980-04-07 265.0 285.0 265.0 265.0 10000We can use the .resample() method, specifying 1 week. Instead of asfreq(), we use.sum()` to add the values.

# resample on just one column (volume)

brk['volume'].resample('1w').sum()date

1980-03-23 30000

1980-03-30 10000

1980-04-06 50000

1980-04-13 120000

1980-04-20 70000

...

2021-10-03 4989

2021-10-10 6059

2021-10-17 6360

2021-10-24 7283

2021-10-31 11404

Freq: W-SUN, Name: volume, Length: 2172, dtype: int64

<string>:2: FutureWarning: 'w' is deprecated and will be removed in a future version, please use 'W' instead.8.8 Exploratory Data Analysis

# select the 'open' column as a series

series = brk['open']# descriptive statistics about the dataset

series.describe()count 10498.000000

mean 92531.835852

std 101720.441234

min 245.000000

25% 7556.250000

50% 68900.000000

75% 123703.750000

max 441063.000000

Name: open, dtype: float64Things to pay attention to:

- The large standard deviation and the size of the first and third quantiles suggest that the data is widely spread around the mean.

- The mean and median(50%) are not equal. The mean is higher, indicating there may be some large outliers.

- There are 10498 data points.

8.8.1 Plotting

Line plot

# plotting the 'open' column as a time series

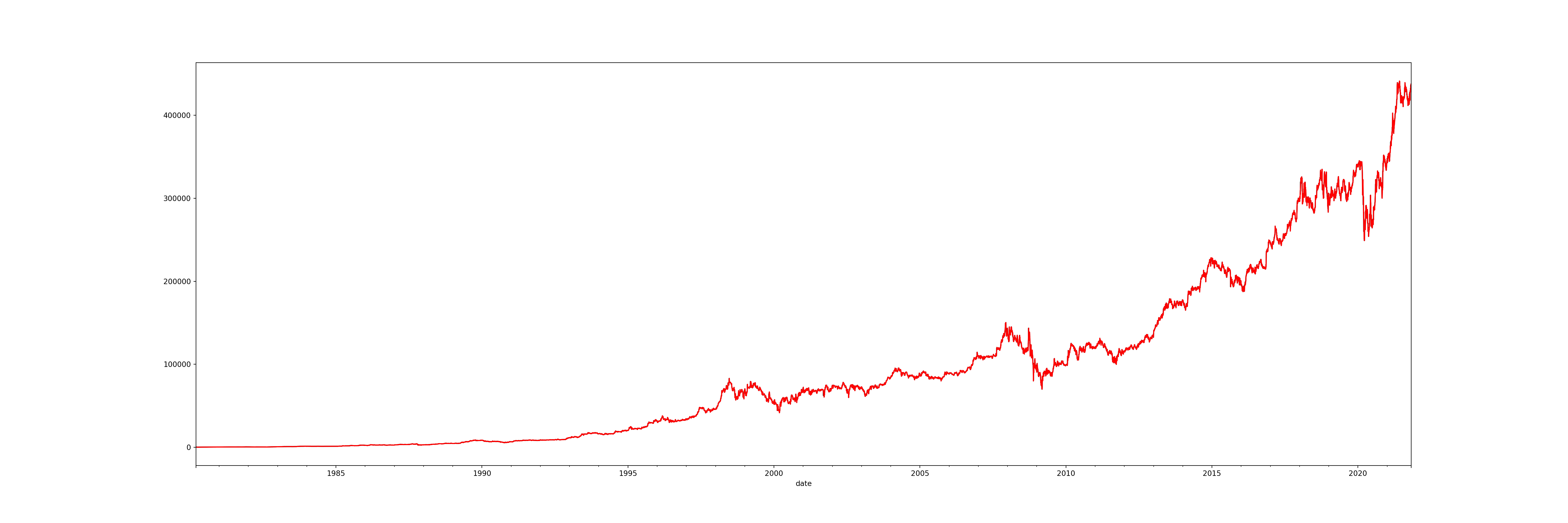

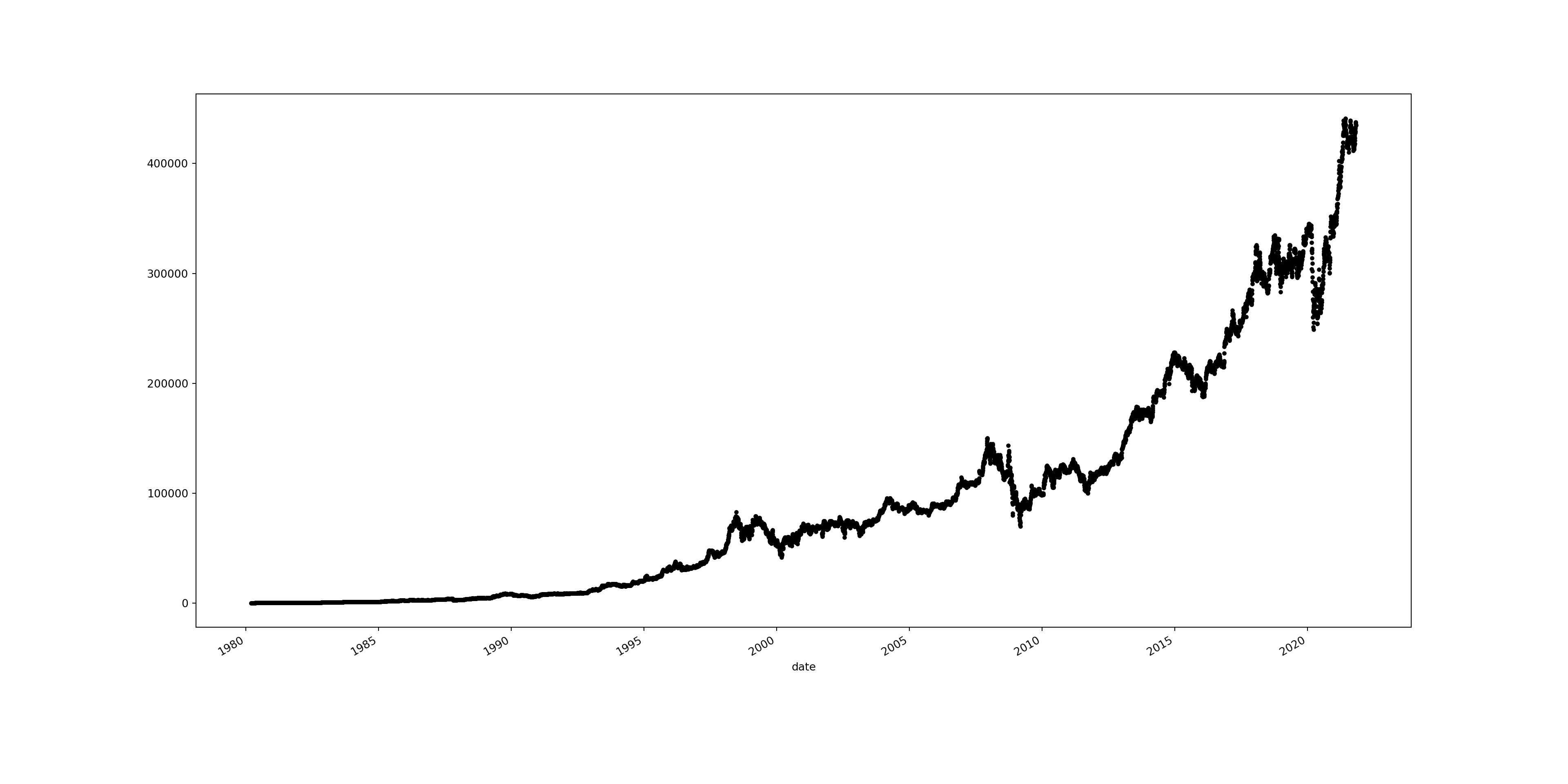

brk['open'].plot(figsize = (20, 7))

However this just demonstrates the time series graph for one column. By using .plot() on the entire dataframe, we can plot each column on the same graph, with a legend for each column.

# plotting entire dataset

brk.plot(figsize = (20, 10))

Sometimes this can be useful because you might want to compare different variables across the same period of time. However, in this case it isn’t too useful as the graph is not overly readable. We can also split them into multiple subplots to make it more readable.

plt.style.use('default')

# plt.style.use('fivethirtyeight')

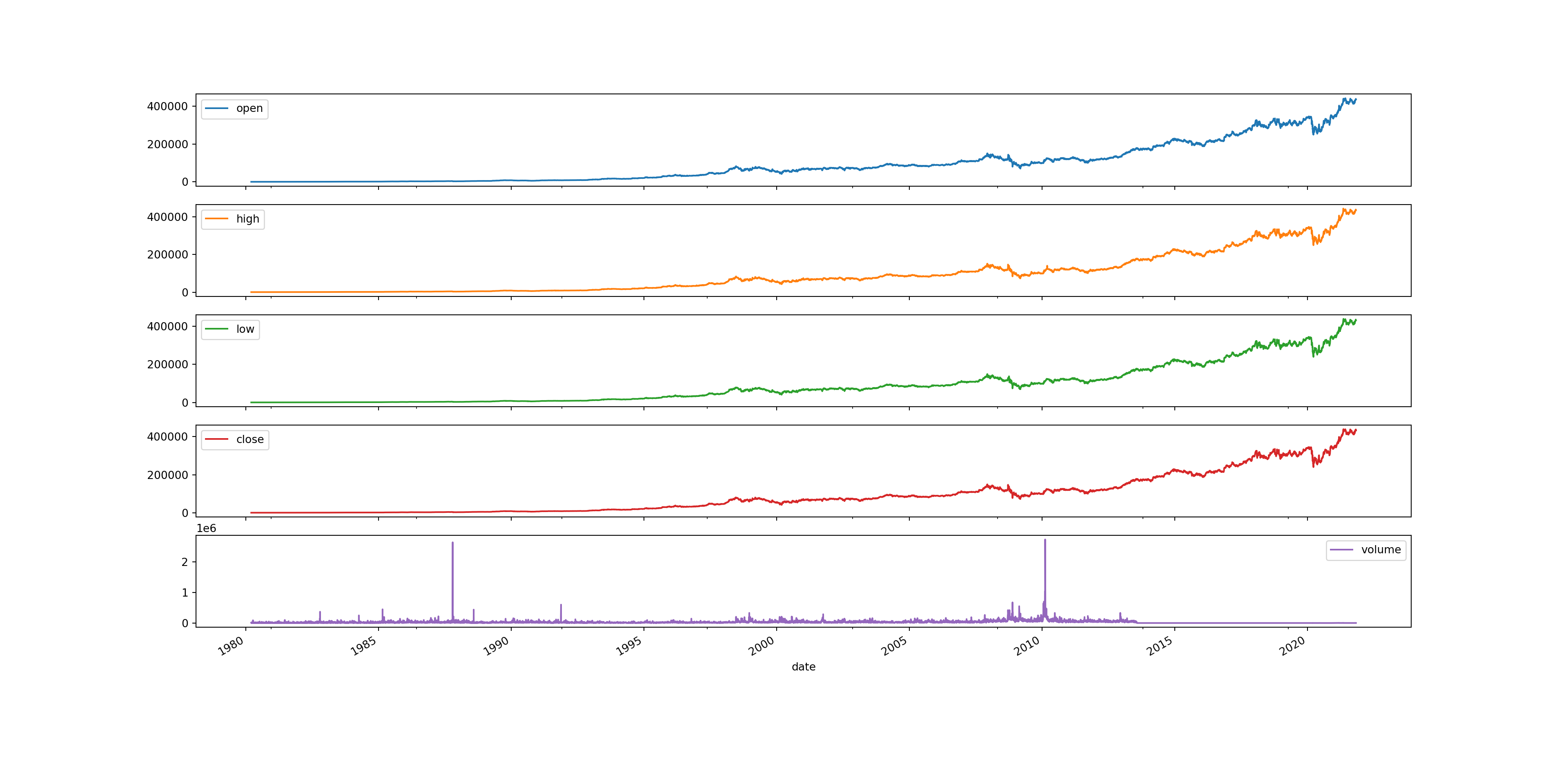

brk.plot(figsize = (20,10), subplots = True);

# styles: 'fivethirtyeight', 'dark_background', 'seaborn-dark', 'tableau-colorblind10', 'default'

We can also check the correlation of different variables. Checking correlation helps to understand the relationship between different variables over time, identify leading/lagging indicators, and uncover potential causal links, which are important for forecasting and model building.

# view correlation of variables

brk.corr() open high low close volume

open 1.000000 0.999952 0.999950 0.999912 -0.096983

high 0.999952 1.000000 0.999922 0.999954 -0.095437

low 0.999950 0.999922 1.000000 0.999952 -0.098510

close 0.999912 0.999954 0.999952 1.000000 -0.096585

volume -0.096983 -0.095437 -0.098510 -0.096585 1.000000Dot plot

A dot plot represents individual data points plotted along a timeline, allowing for the visualisation of trends, patterns, or changes over time. Each dot corresponds to an individual observation at a specific point in time, making it a straightforward method for displaying discrete measurements and detecting outliers or shifts within the time series data.

# creating a dot plot for the 'open' column

brk['open'].plot(style = 'k.', figsize = (20, 10))

More style options: https://matplotlib.org/stable/users/prev_whats_new/dflt_style_changes.html

Group by years

# view the data by week

brk_week = brk.resample('1w').mean()<string>:2: FutureWarning: 'w' is deprecated and will be removed in a future version, please use 'W' instead.# create an empty dataframe

years = pd.DataFrame()

# create groupby object containing annual data

groups = brk_week.groupby(pd.Grouper(freq = 'A'))<string>:3: FutureWarning: 'A' is deprecated and will be removed in a future version, please use 'YE' instead.

# extract name and group from the groupby object

for name, group in groups:

# The year is extracted from the name

year = name.year

years[year] = group['open'].reset_index(drop=True)

years.head() 1980 1981 1982 ... 2019 2020 2021

0 290.0 423.75 560.0 ... 300178.750 339276.680 343964.0500

1 274.0 427.00 560.0 ... 295379.980 340219.200 346625.0000

2 262.5 425.00 548.0 ... 296125.500 342061.218 350187.4000

3 264.0 426.00 528.0 ... 302580.250 343636.500 352288.0625

4 254.0 430.00 506.0 ... 305244.998 336103.000 346884.9740

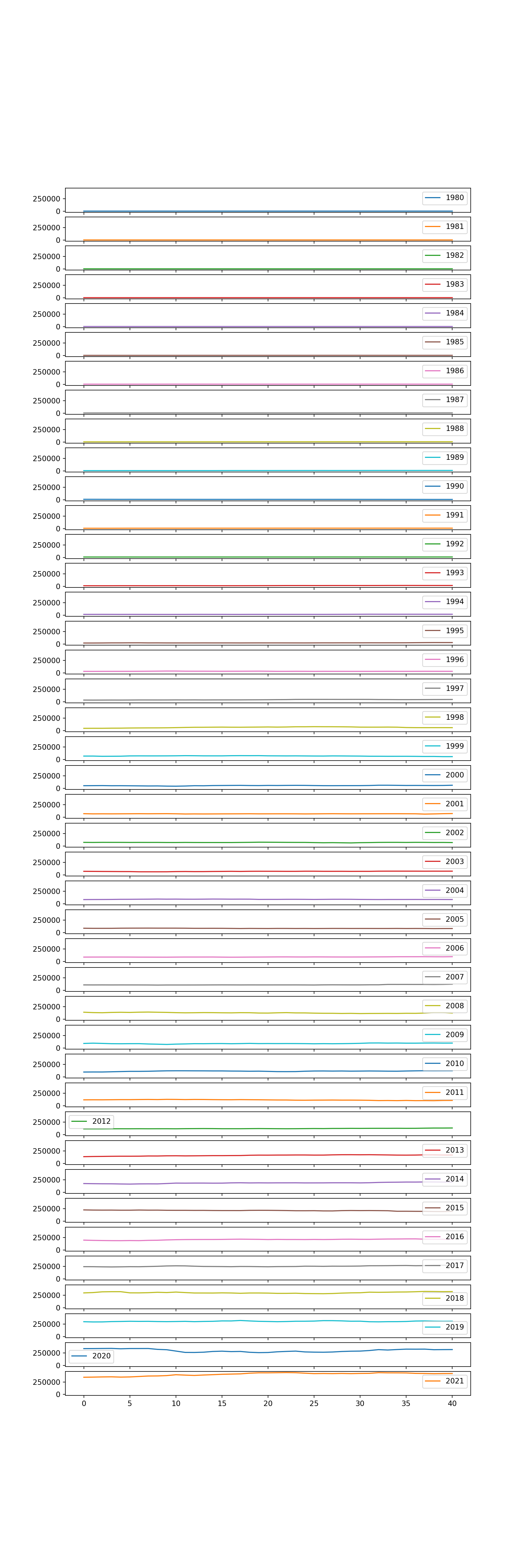

[5 rows x 42 columns]# create a plot for each year

years.plot(subplots = True, legend = True, figsize = (10, 30), sharex = True, sharey = True);

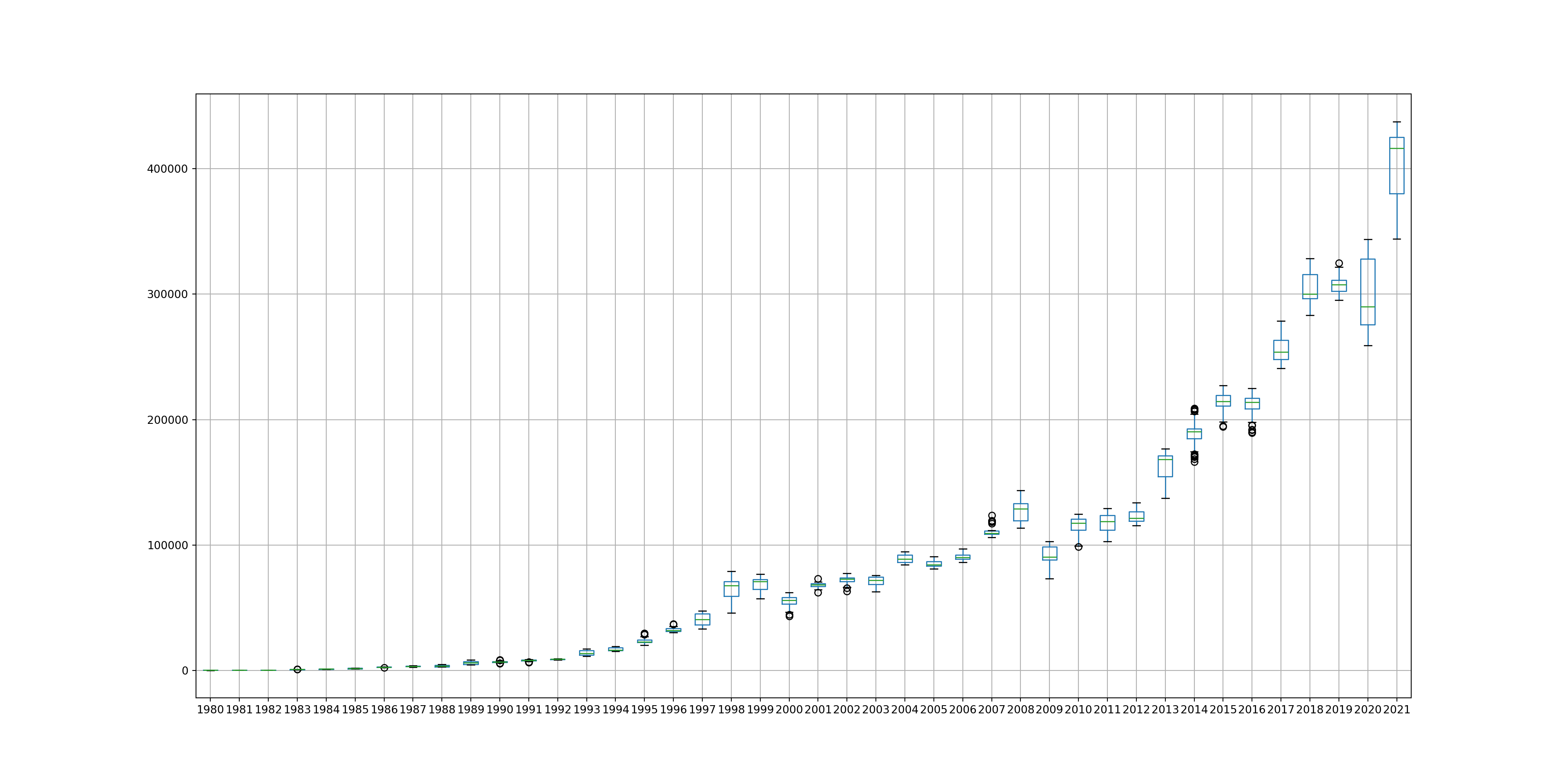

Box and Whisker plots

We can also create box and whisker plots in order to help us interpret the data. This can be very useful as it can help us to view outliers for a particular year, as well as see how spread the data is. This is particularly useful for identifying changes in data distribution over time.

years.boxplot(figsize = (20, 10))

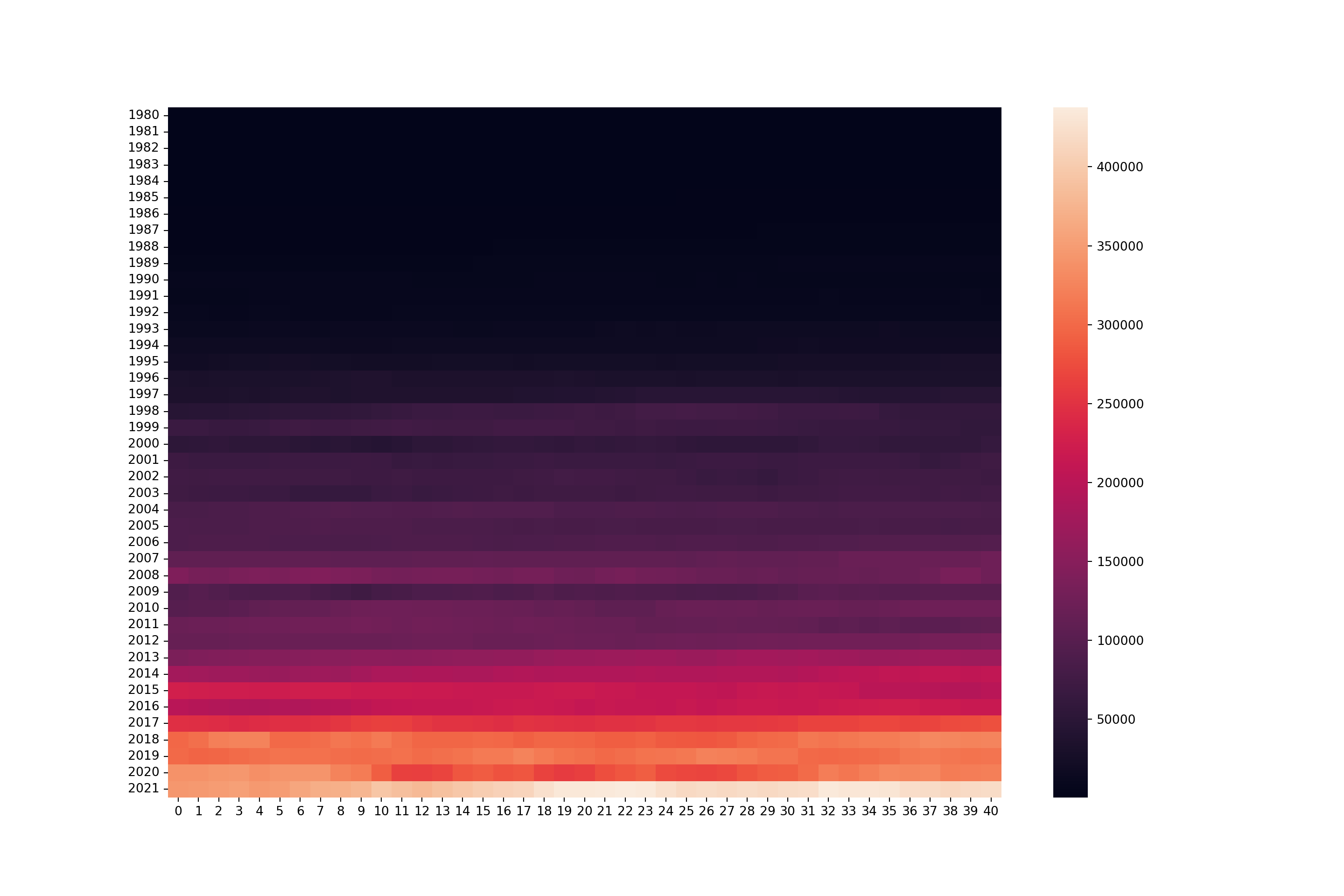

Heat Maps

Heatmaps are useful for analysing time series data because they provide a visual summary of complex information, allowing for quick identification of patterns, trends, and anomalies across time. By representing data values with colours, heatmaps make it easy to spot variations in intensity at a glance, such as periods of high or low activity.

# transpose the data

years_inverse = years.Tyears_inverse.head() 0 1 2 3 ... 37 38 39 40

1980 290.00 274.0 262.5 264.0 ... 454.0 456.0 425.0 423.75

1981 423.75 427.0 425.0 426.0 ... 485.0 481.0 461.0 460.00

1982 560.00 560.0 548.0 528.0 ... 525.0 543.0 550.0 559.00

1983 772.00 776.0 787.0 775.0 ... 1153.0 1168.0 1232.0 1242.00

1984 1330.00 1300.0 1356.0 1348.0 ... 1291.0 1295.0 1301.0 1305.00

[5 rows x 41 columns]# create heatmap with seaborn

fig, ax = plt.subplots(figsize = (15, 10))

sns.heatmap(years_inverse)

How would this be interpreted, taking into consideration what values the heatmap is showing?

Histogram and density plots

Histograms and density plots are valuable for analysing time series data as they provide insights into the distribution and density of data points over a specific period. These visualisations help identify patterns such as skewness, multimodality, and outliers, offering potential clues about underlying trends.

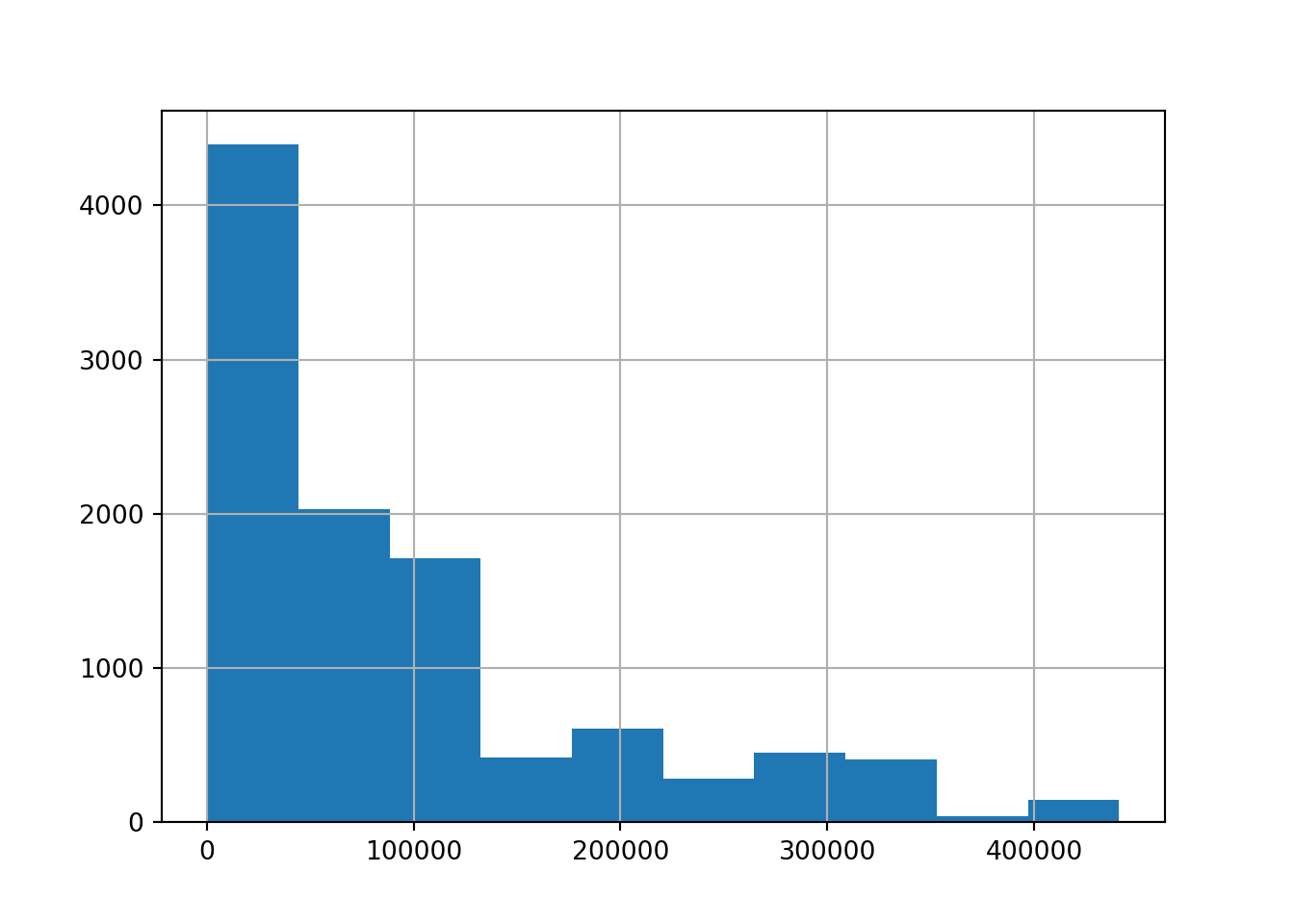

# create a histogram of the 'open' column

brk['open'].hist();

What does the histogram tell us about the data?

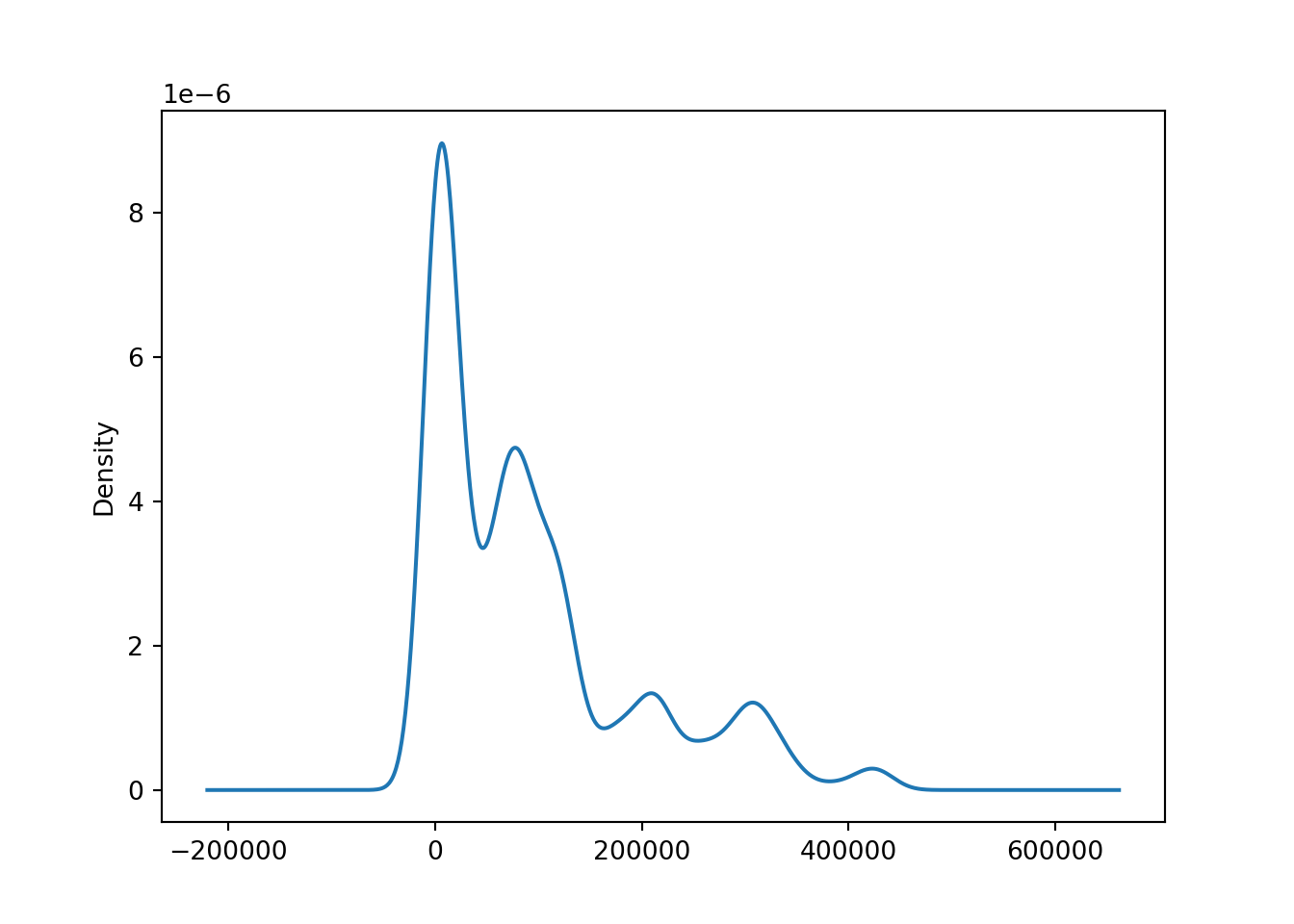

# create a kde plot of the data

brk['open'].plot(kind = 'kde');

A kernel density estimate (KDE) plot is a method for visualizing the distribution of observations in a dataset, similar to a histogram. KDE represents the data using a continuous probability density curve in one or more dimensions

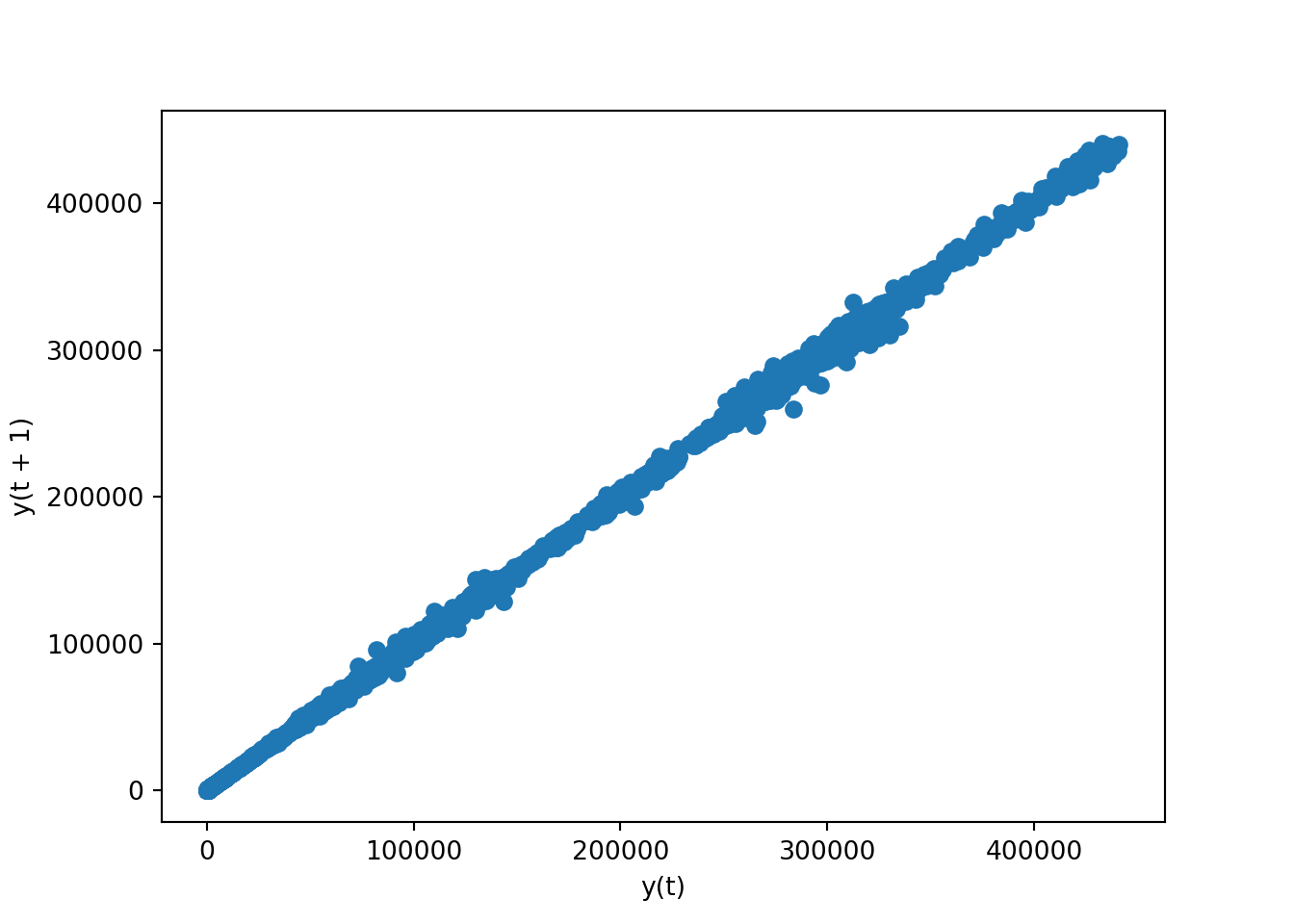

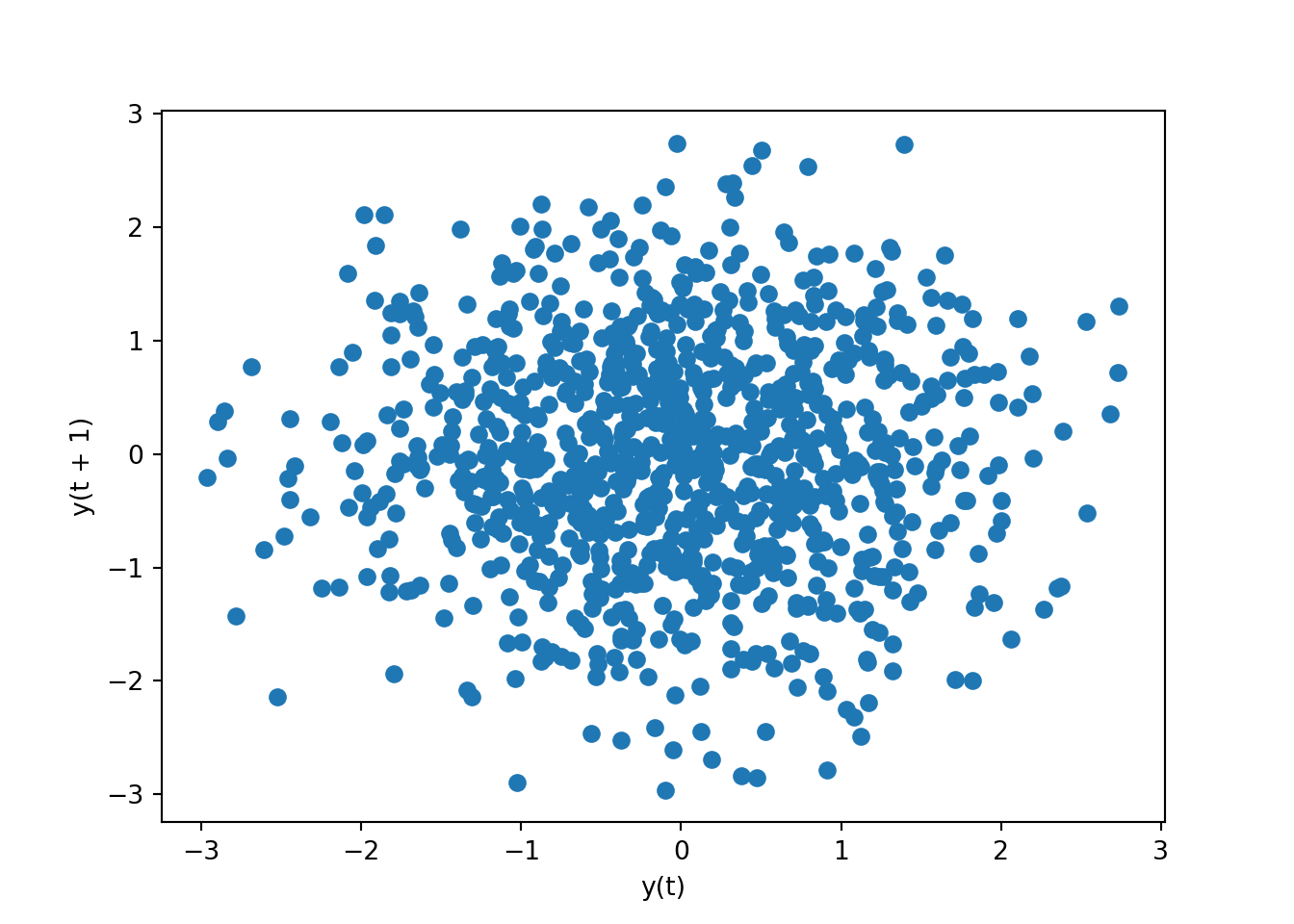

Scatter plot (lag plot)

A lag plot is a scatter plot used in time series analysis to help evaluate whether a data set or variable is random or has some time-dependent structure. It plots data points at time \(t\) on the x-axis and the data points at time \(t+n\) on the y-axis, where \(n\) is the lag amount.

If the points cluster along a diagonal line from the bottom-left to top-right, there is likely an autocorrelation indicating that the data is influenced by its prior values. Randomly scattered points suggest no such autocorrelation, indicating randomness in the data.

# lag plot for 'open' column

pd.plotting.lag_plot(brk['open'])

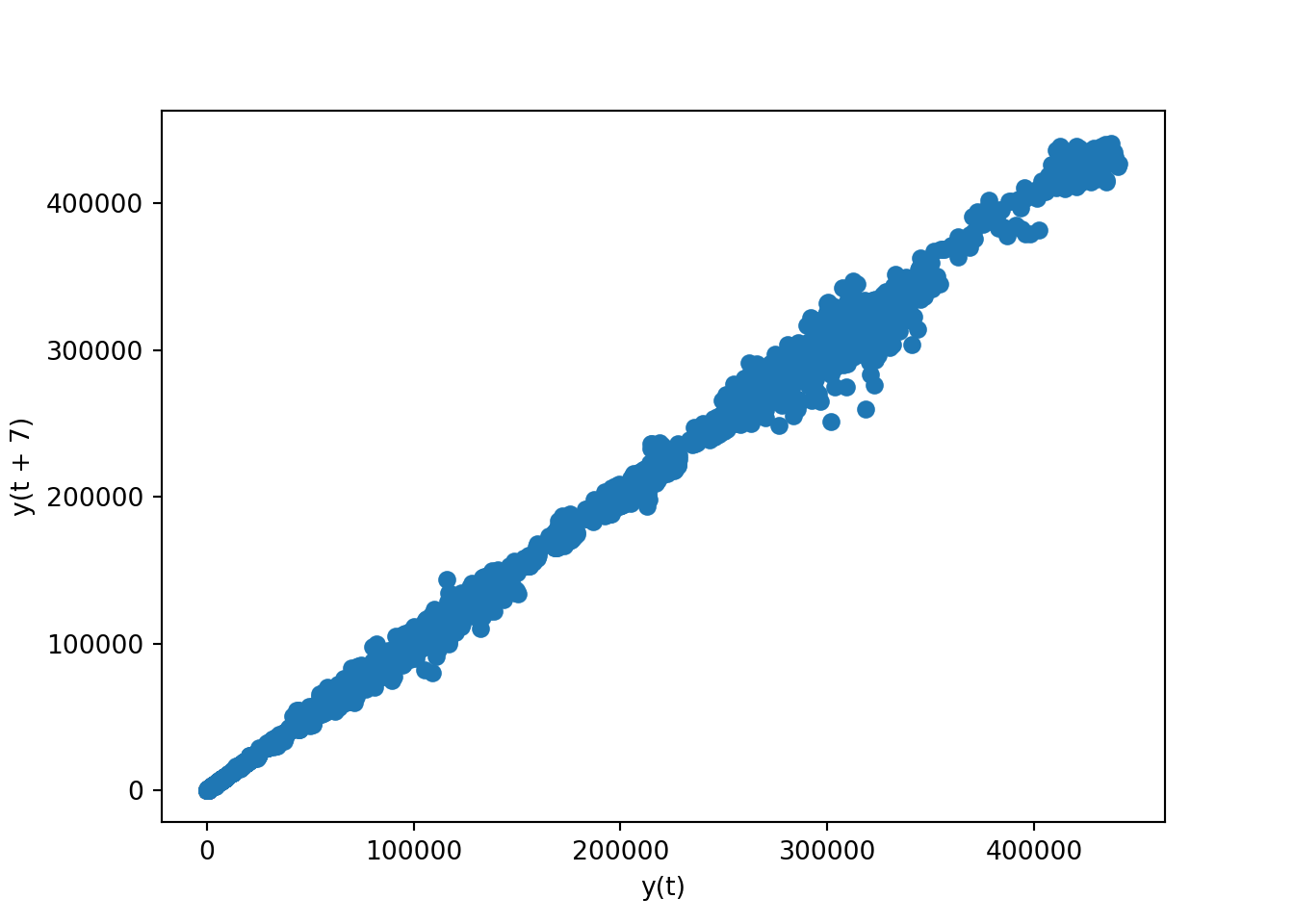

We can also use the lag parameter, which specifies the lag amount (the number of time periods to go back when comparing data points). With lag=7, the plot will compare each data point with the data point that is 7 periods before it. This is particularly useful in time series analysis to check for weekly seasonality – for instance, if you have daily data, lag=7 would help to see the correlation from one week to the next.

pd.plotting.lag_plot(brk['open'], lag = 7)

8.9 Decomposing time series data

There are three major components for any time series process: trend, seasonality, residual.

- Trend gives a sense of the long-term direction of the time series and can be either upward, downward or horizontal.

- Seasonality is repeated pattern over time. Example: Increasing of sales around Christmas each year.

- The residuals are the remaining or unexplained data points once we extract trend and seasonality.

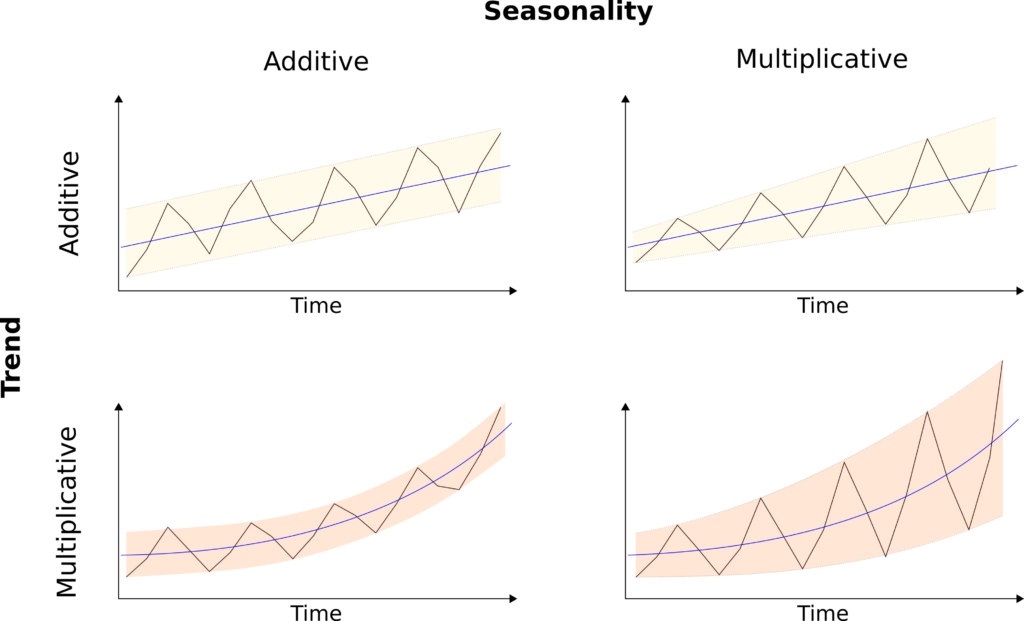

The decomposition of a time series is the process of extracting these three components. The modelling of the decomposed components can be either additive or multiplicative.

Based on the additive model we can reconstruct the original time series by adding all three components.

y = Trend + Seasonality + Residual

The additive model should be applied when the seasonal variations do not change over time.

Based on the multiplicative model we can reconstruct the time series data by multiplying the 3 components.

y = Trend x Seasonality x Residual

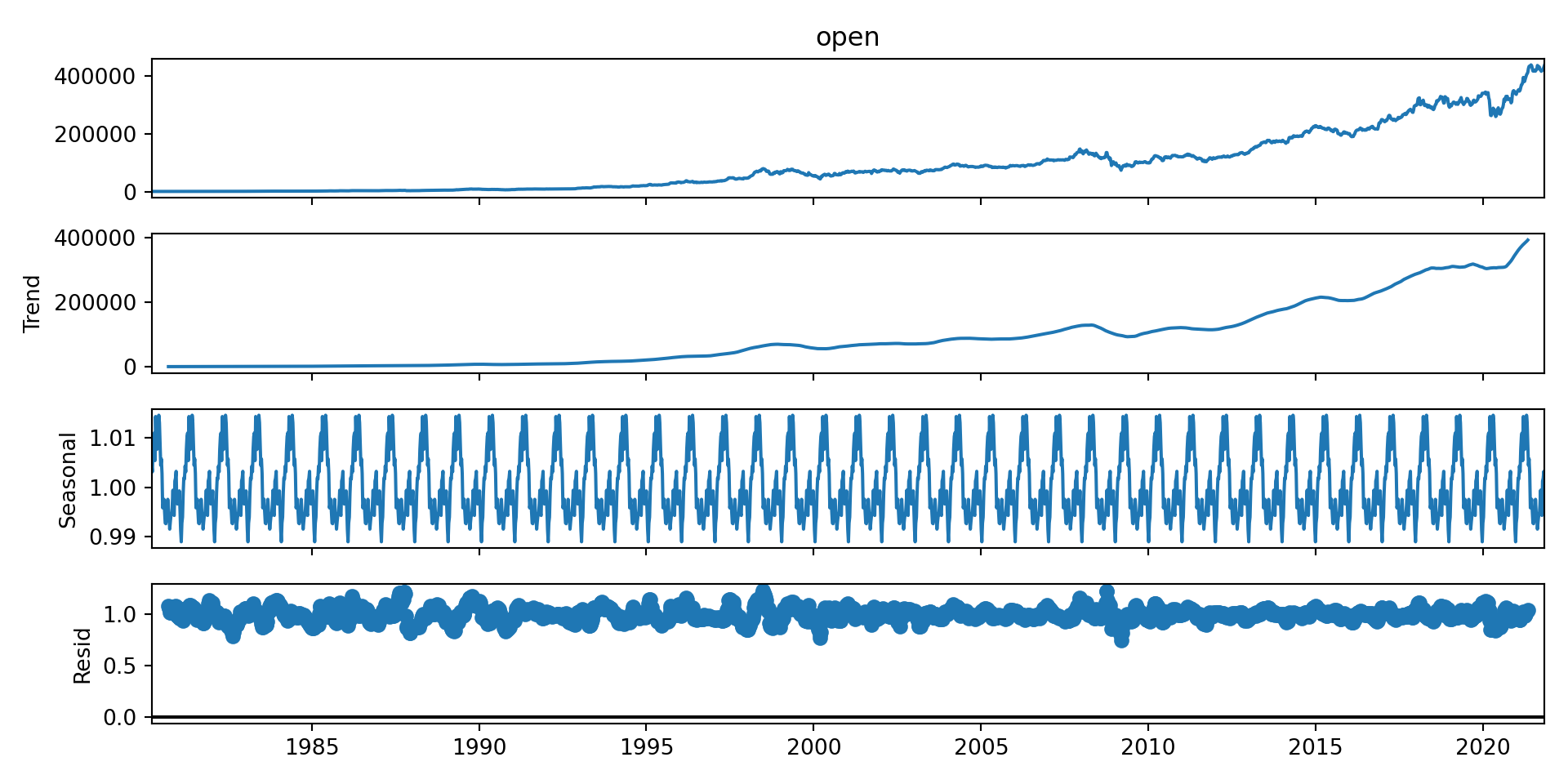

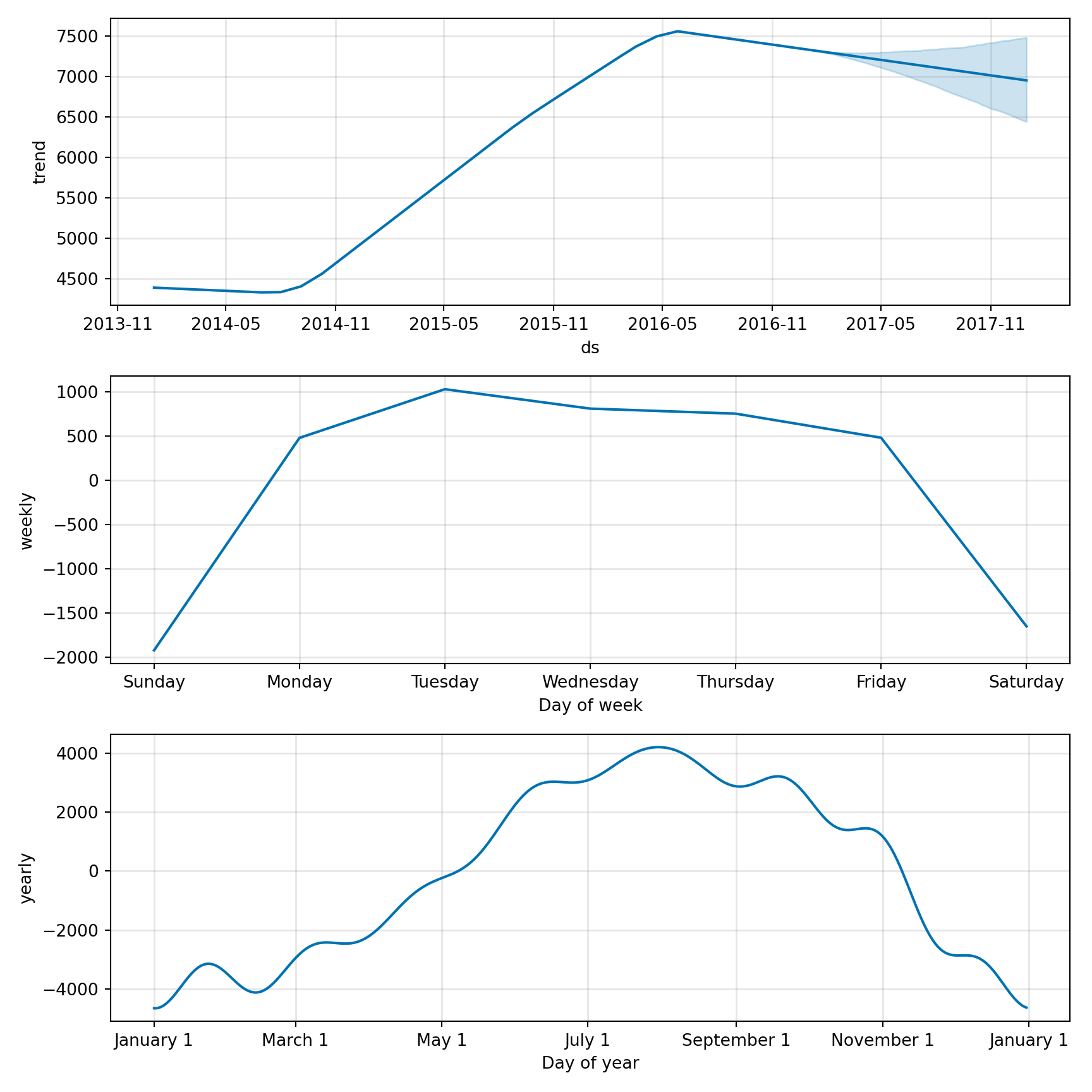

# plot the open column

brk_week['open'].plot()

# import packages

from statsmodels.tsa.seasonal import seasonal_decompose, STLLink to seasonal decomposition documentation:

brk_week_decomposed = seasonal_decompose(brk_week['open'], model = 'multiplicative') # model is optionalWhen you don’t specify the model parameter, seasonal_decompose defaults to using the “additive” model because many time series with a seasonal component can be adequately modeled with additive effects, especially when the seasonal fluctuations do not vary much in scale over time.

plt.rcParams['figure.figsize'] = (10,5)

brk_week_decomposed.plot()

- The first chart - The original observed data

- The trend shows an upward direction - positive(also can be negative or constant)

- The seasonal component shows the repeating pattern of highs and lows.

- The residual component shows the random variation in the data, and is what is left over after fitting a model.

8.10 Checking for Stationarity

Example - bicycle data

# read in data

bicycles = pd.read_csv("data/bicycle_rent.csv")

# convert start time column to datetime format

bicycles['starttime'] = pd.to_datetime(bicycles['starttime'], format ='%Y-%m-%d %H:%M:%S')

# convert start time column to index

bicycles_date = bicycles.set_index('starttime')

# resample data to months

bicycles_date['count'] = 1 # create a count column to tally eventd

bicycles_months = bicycles_date.resample('1m').count()<string>:1: FutureWarning: 'm' is deprecated and will be removed in a future version, please use 'ME' instead.bicycles_months.info()<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 33 entries, 2014-01-31 to 2016-09-30

Freq: ME

Data columns (total 4 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 stoptime 33 non-null int64

1 tripduration 33 non-null int64

2 temperature 33 non-null int64

3 count 33 non-null int64

dtypes: int64(4)

memory usage: 1.3 KB# create a series consisting of count column

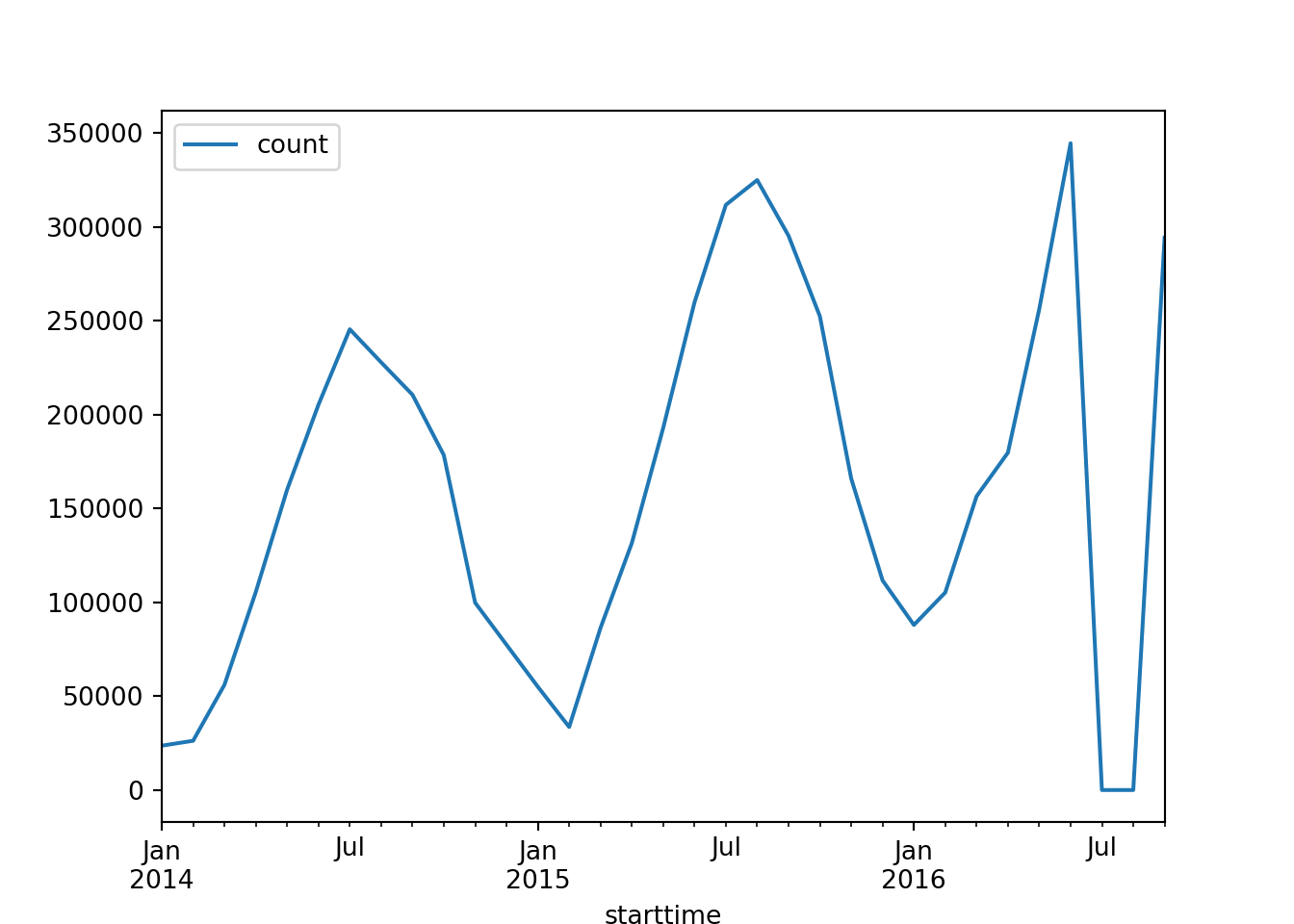

series = bicycles_months[['count']]# plot the series

series.plot()

Many forecasting techniques assume stationarity. That’s why it is crucial to understand if the data we are working with is stationary or non-stationary.

A stationary time series doesn’t have a trend or seasonality. Thus the data don’t have patterns or specific statistical properties that vary over time. This kind of data makes the process easier to model and predict.

Non-stationary data contains patterns that might vary over time, making the modelling process more complex due to the dynamic nature of the data.

8.10.1 The Augmented Dickey-Fuller Test

The Augmented Dickey-Fuller (ADF) test is used to check if a series is stationary.

- Null Hypothesis \((H_0)\): The series is non-stationary.

- Alternative Hypothesis \((H_1)\): The series is stationary.

How Does the ADF Test Work?

The test incorporates lagged (past) values of the time series to account for any autocorrelation. After running the test, we compare the test statistic to critical values at various confidence levels. If the test statistic is less than the critical value, we reject the null hypothesis, suggesting the series does not have a unit root and is likely stationary.

Why is the ADF Test Important?

Understanding whether a time series is stationary is essential before applying most forecasting models, as these models assume stationarity.

https://www.statsmodels.org/dev/generated/statsmodels.tsa.stattools.adfuller.html

from statsmodels.tsa.stattools import adfulleradfuller(series)(-1.732429016531073, 0.4144862524209757, 8, 24, {'1%': -3.7377092158564813, '5%': -2.9922162731481485, '10%': -2.635746736111111}, 555.2839223446316)

# pvalue of 1 > 0.05 ===> The null hypothesis cannot be rejected.

# Hence data is non-stationary (it has relation with time)The result is a tuple with the following information:

ADF Statistic: This is the value of the test statistic. The more negative this statistic, the stronger the rejection of the hypothesis that there is a unit root at some level of confidence. In other words, more negative values suggest the series is stationary.

p-value: This represents the probability of observing the test results under the null hypothesis. In this case, the p-value is relatively high, suggesting that there is not enough evidence to reject the null hypothesis of the presence of a unit root, meaning the time series might be non-stationary.

Critical values: These values represent the test statistic values needed to reject the null hypothesis of a unit root presence at the 1%, 5%, and 10% levels of significance, respectively. Our ADF statistic is not more negative than any of these, suggesting we cannot reject the null hypothesis for any usual level of significance.

Because the bike data is not stationary, we need to perform some transformations.

8.11 Detrending

Detrending refers to the process of removing trends from a time series. Trends represent long-term movements in data, which can be linear (steady increase or decrease over time) or non-linear (seasonal or cyclical patterns). The practice of detrending is pivotal for several reasons:

Achieving Stationarity: Time series analysis and forecasting models often presume stationarity, where the statistical properties (mean, variance) of the series are constant over time. Detrending is a critical step towards converting a non-stationary series into a stationary one by eliminating the underlying trends.

Understanding Data Better: By removing the trend, it becomes easier to isolate and analyze the data’s fluctuations or noise not explained by the trend. This can uncover insights into the data’s underlying mechanisms or reveal hidden patterns.

Enhancing Forecasting Accuracy: Forecasting models developed on detrended data can be more accurate, as they focus on predicting the stationary components of the series (like seasonal variations) without being influenced by long-term trends.

Comparing Different Time Series: Detrending allows for the comparison of different time series data on an equal footing by removing their underlying trends, facilitating a more straightforward analysis and understanding.

Detrending is an important preprocessing step in time series analysis, enabling more precise analysis, modelling, and forecasting by focusing on the intrinsic properties of the data, independent of any trend.

8.12 Differentiating

# creating a dataframe for the series - we want to add lag to the data and will need a new column for this

series_df = pd.DataFrame(series)

# add shifted data to new column

series_df['shifted_1lag'] = series_df.shift(1)

series_df.head() count shifted_1lag

starttime

2014-01-31 23617 NaN

2014-02-28 26221 23617.0

2014-03-31 56020 26221.0

2014-04-30 105428 56020.0

2014-05-31 159957 105428.0Next, we need to perform differentiation between the orginal series and the lagged series. This will then give us the difference between the two ‘count’ values.

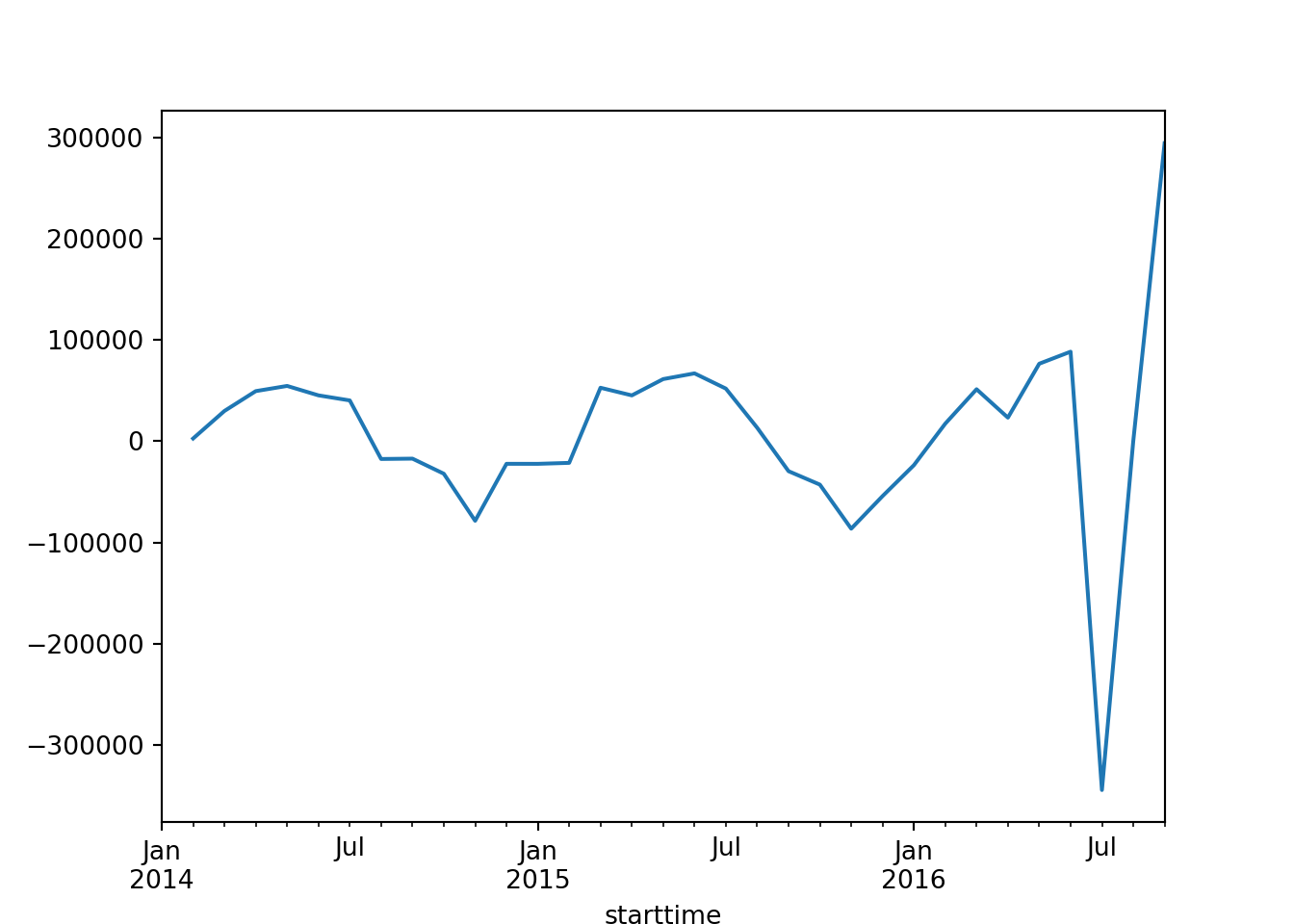

# create new column for the difference

series_df['series_diff'] = series_df['count'] - series_df['shifted_1lag']

series_df.head() count shifted_1lag series_diff

starttime

2014-01-31 23617 NaN NaN

2014-02-28 26221 23617.0 2604.0

2014-03-31 56020 26221.0 29799.0

2014-04-30 105428 56020.0 49408.0

2014-05-31 159957 105428.0 54529.0We now perform the ADF test again, this time on the series_diff column.

pvalue = adfuller(series_df['series_diff'][1:])[1] # from second row onwards

pvalue0.8341986459358672if pvalue > 0.05:

print('data is non-stationary')

else:

print('data is stationary')data is non-stationary# plot the series difference data

series_df['series_diff'].plot()

As the data is not stationary, we need to perform differencing again.

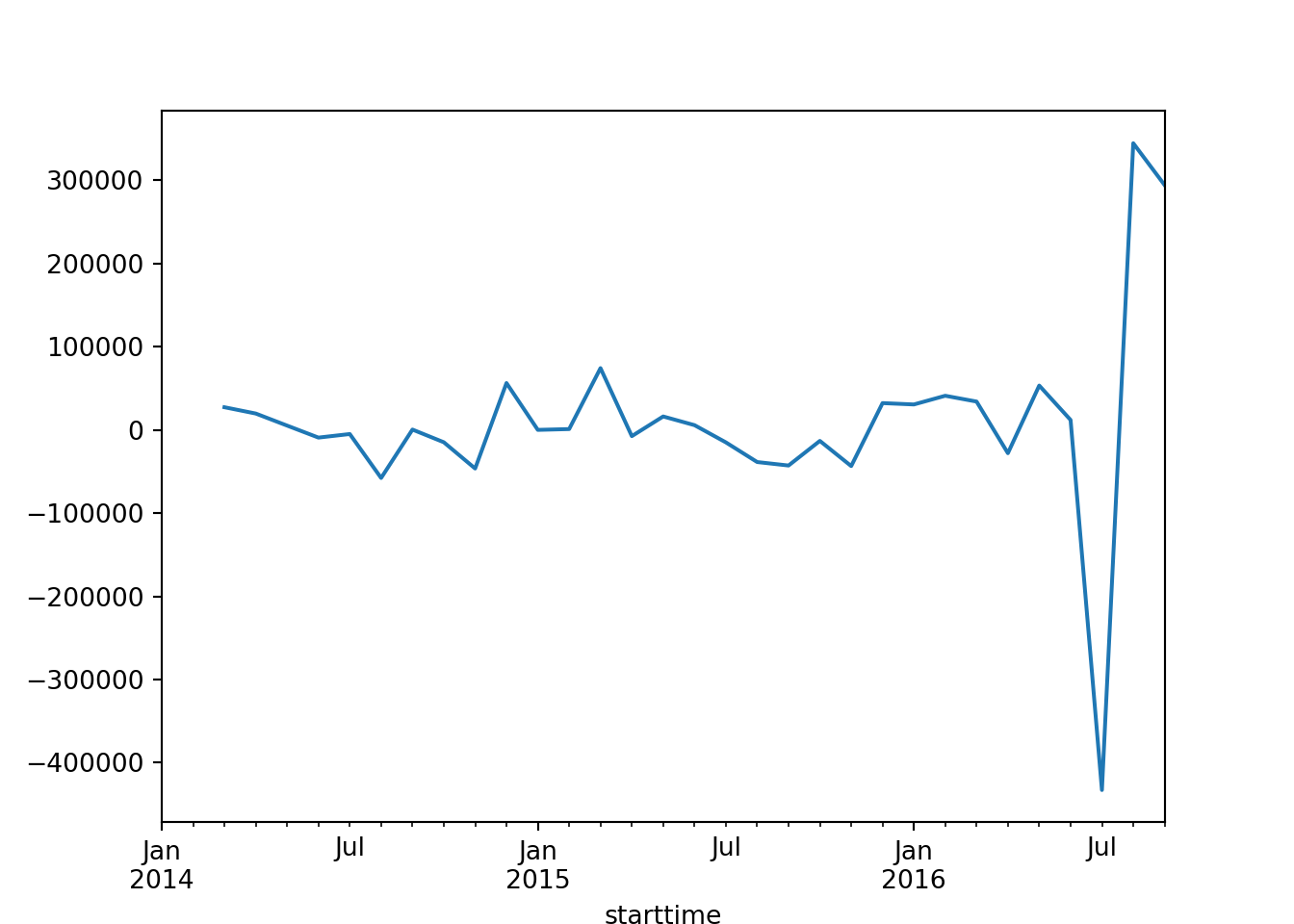

# Add second differencing

series_df['series_diff_2'] = series_df['series_diff'].diff()

# perform the ADF test on the second difference

pvalue_second_diff = adfuller(series_df['series_diff_2'].dropna())[1] # from the second row onwards due to differencing

print(pvalue_second_diff)2.1744798473897922e-06if pvalue_second_diff > 0.05:

print('Data is still non-stationary after second differencing.')

else:

print('Data is stationary after second differencing.')Data is stationary after second differencing.# plot the series difference data

series_df['series_diff_2'].plot()

8.13 White noise

Example

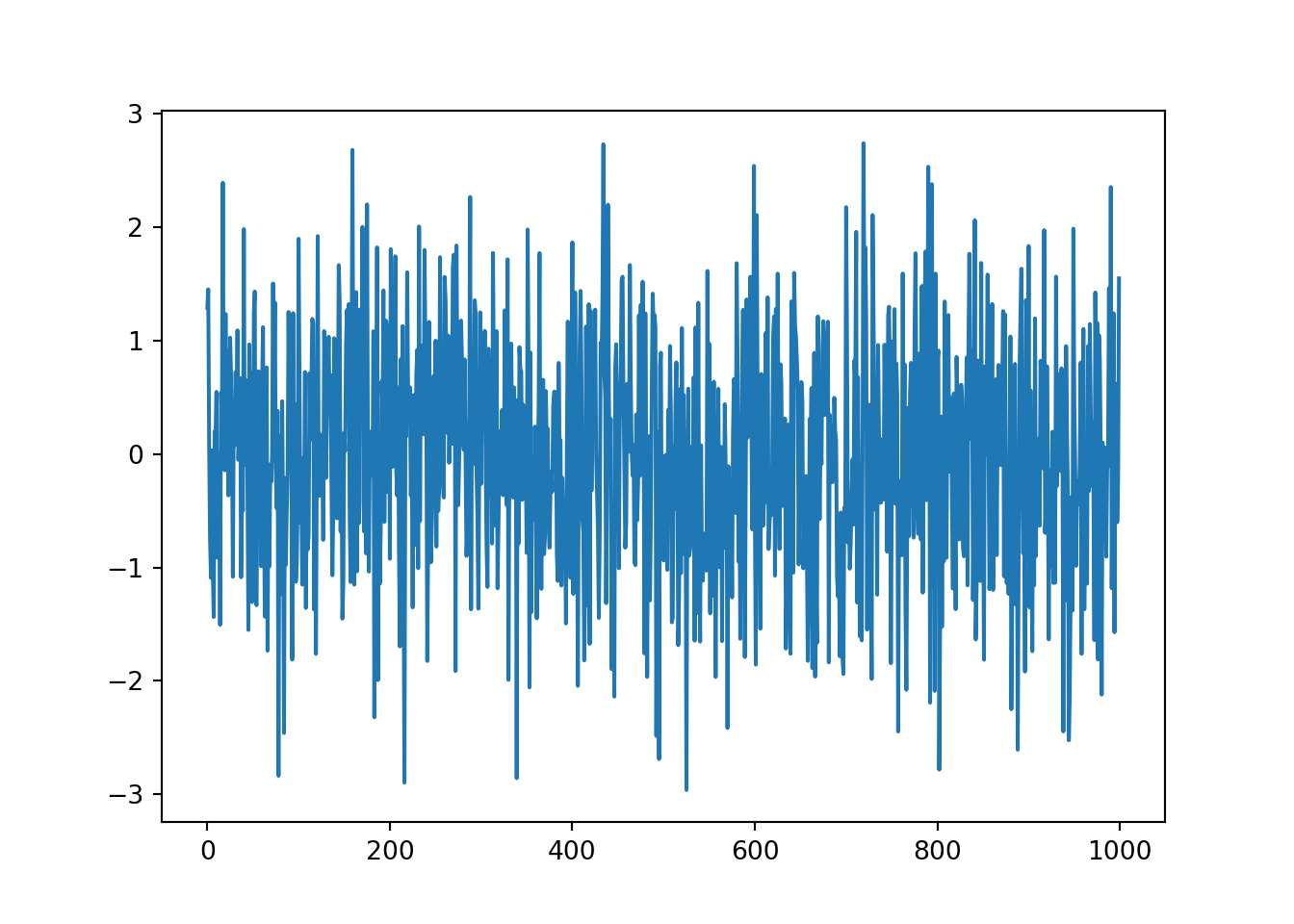

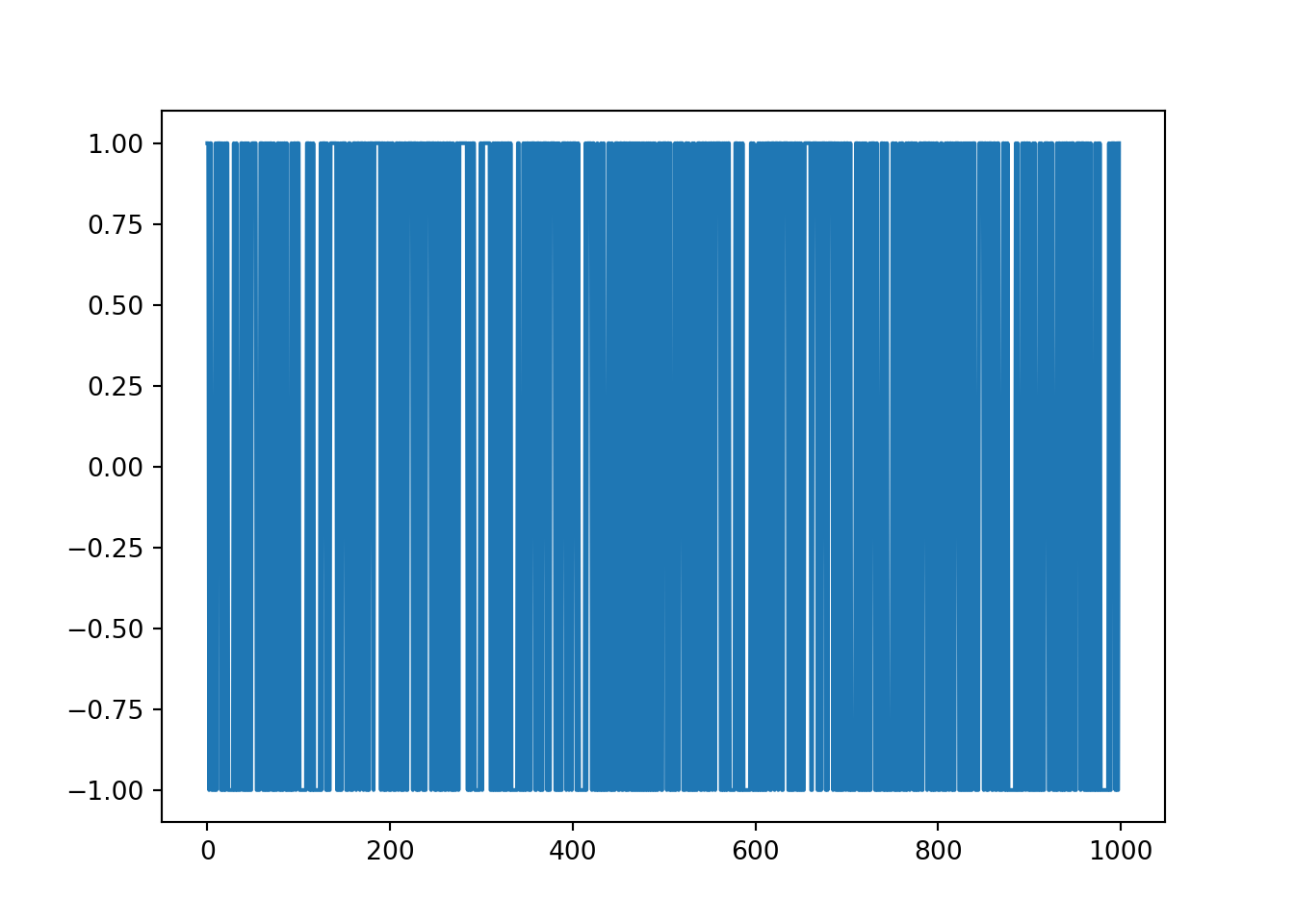

First, we will generate a series which will contain 1000 data points. It is drawn from a normal distribution with mean 0 and standard deviation of 1, meaning the numbers are very likely (99.9999%) to be between -4 and 4.

# generate data

import random

random.seed(1)

series = []

for i in range(1000):

n = random.gauss(0, 1)

series.append(n)# view information about the series

series = pd.Series(series)

series.describe()count 1000.000000

mean -0.013222

std 1.003685

min -2.961214

25% -0.684192

50% -0.010934

75% 0.703915

max 2.737260

dtype: float64What do we notice about the mean? Does this mean we have white noise?

# plot the data

series.plot()

It’s very hard to find patterns in the data at the moment.

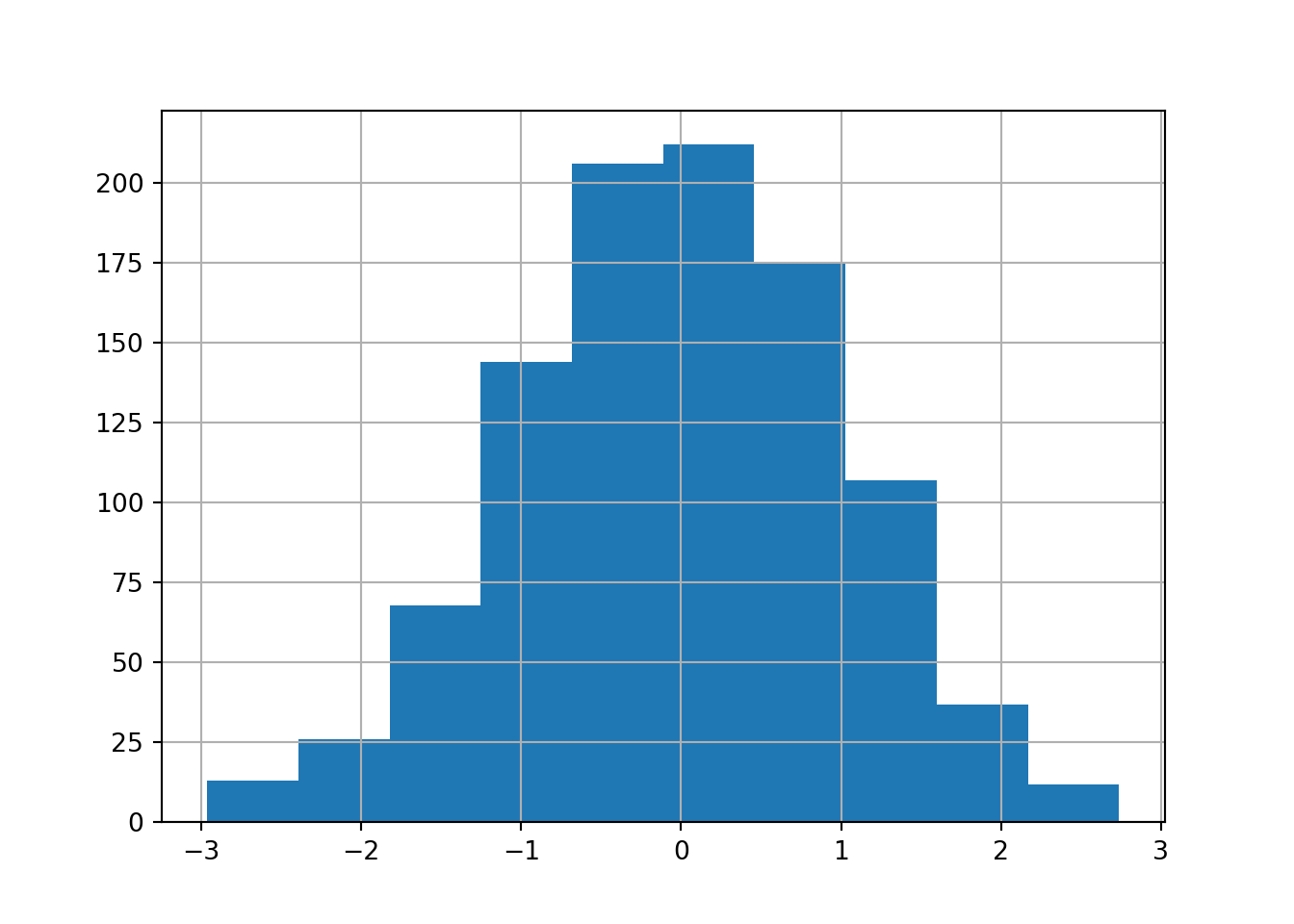

We can also view it as a histogram.

# view series as a histogram

series.hist()

# lag the data with default 1

pd.plotting.lag_plot(series)

There are no patterns, which means there is no autocorrelation between a specific time and its lag.

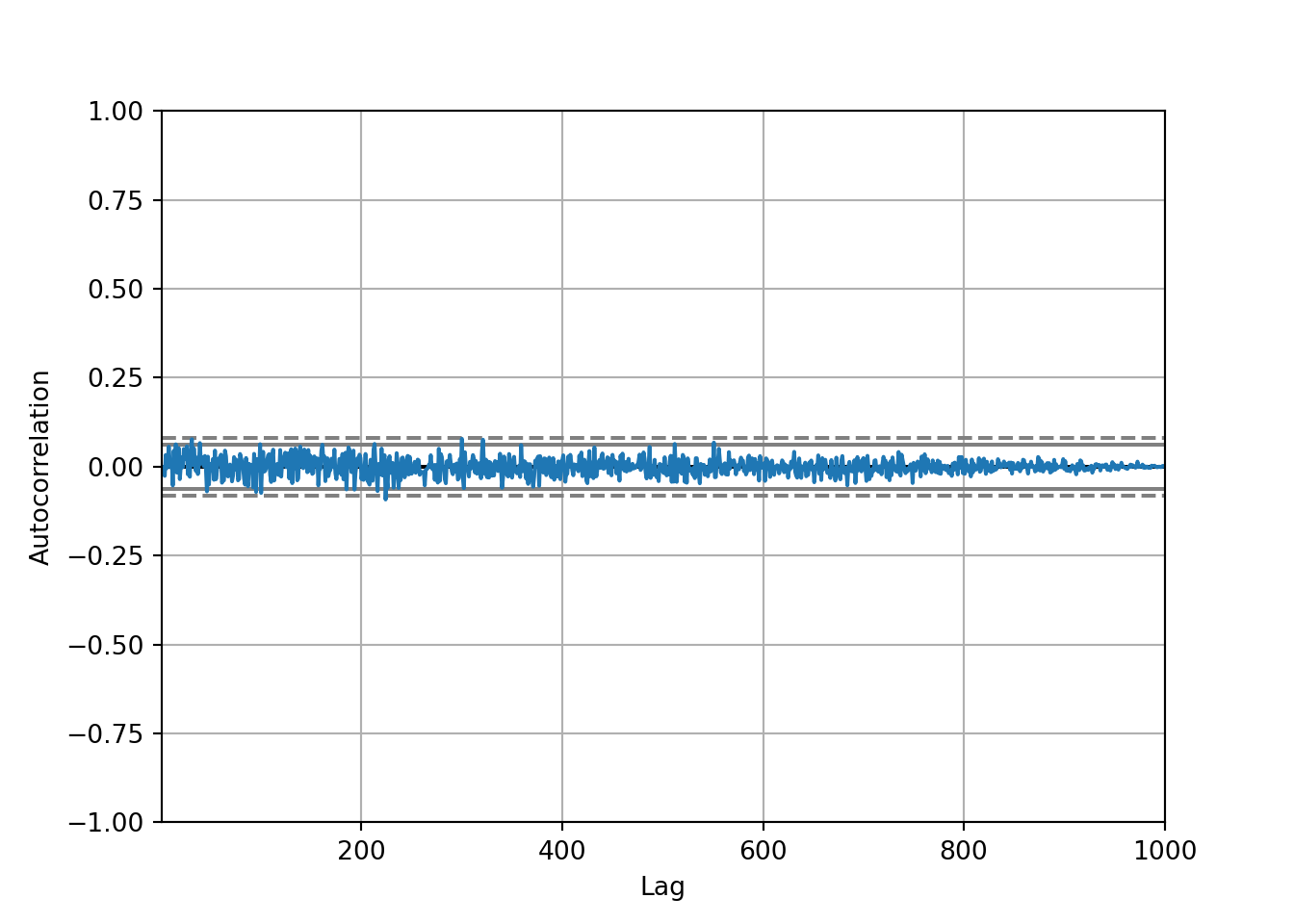

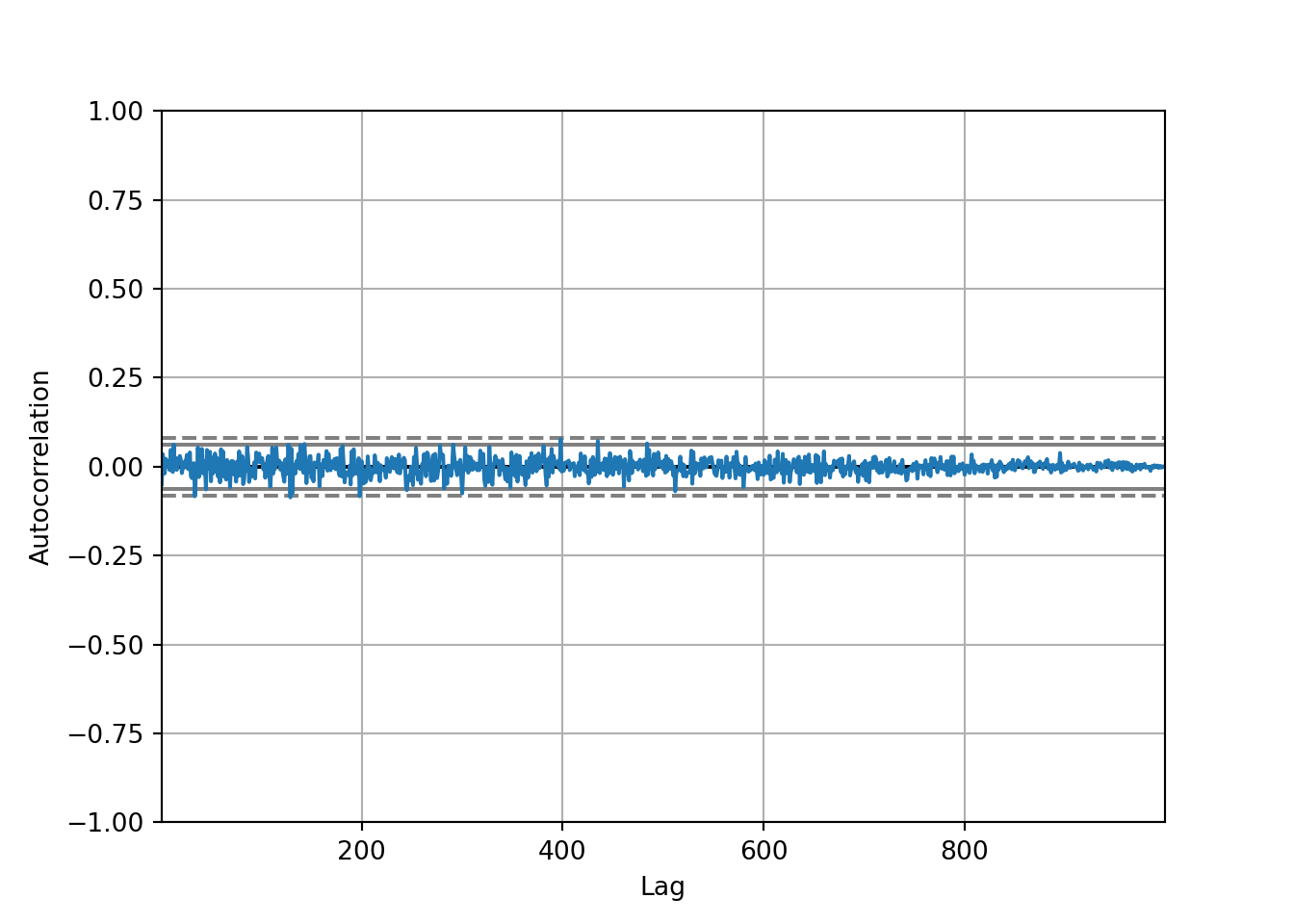

We can import a new package from pandas, called autocorrelation_plot, which shows whether the elements of a time series are correlated with each other. Lag is on the x axis and Autocorrelation is on the y axis (correlation between the original series and the lagged data.

from pandas.plotting import autocorrelation_plot

# plot the series

autocorrelation_plot(series)

To interpret the autocorrelation plot:

Autocorrelation represents the degree of similarity between a given time series and a lagged version of itself over successive time intervals.

Autocorrelation measures the relationship between a variable’s current value and its past values.

An autocorrelation of +1 represents a perfect positive correlation, while an autocorrelation of -1 represents a perfect negative correlation.

All of the values for autocorrelation are very low (around 0). The grey lines, which are the boundaries of confidence, shouldn’t have any blue points that cross it, which means there is no significant correlation in this dataset.

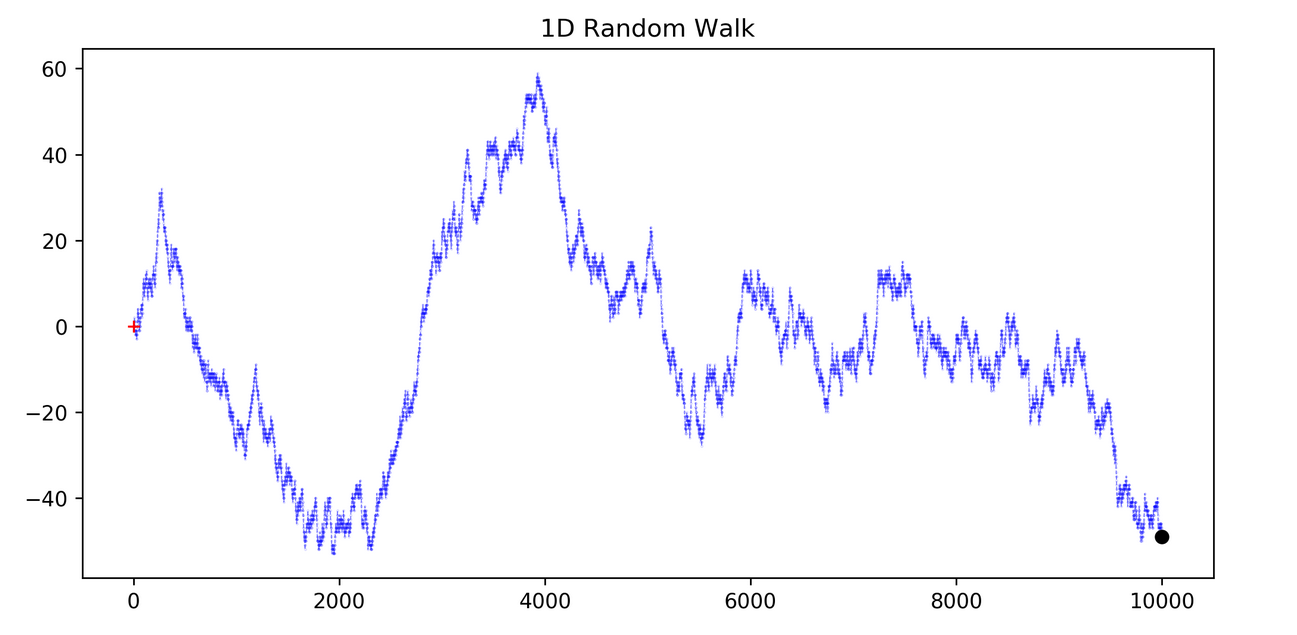

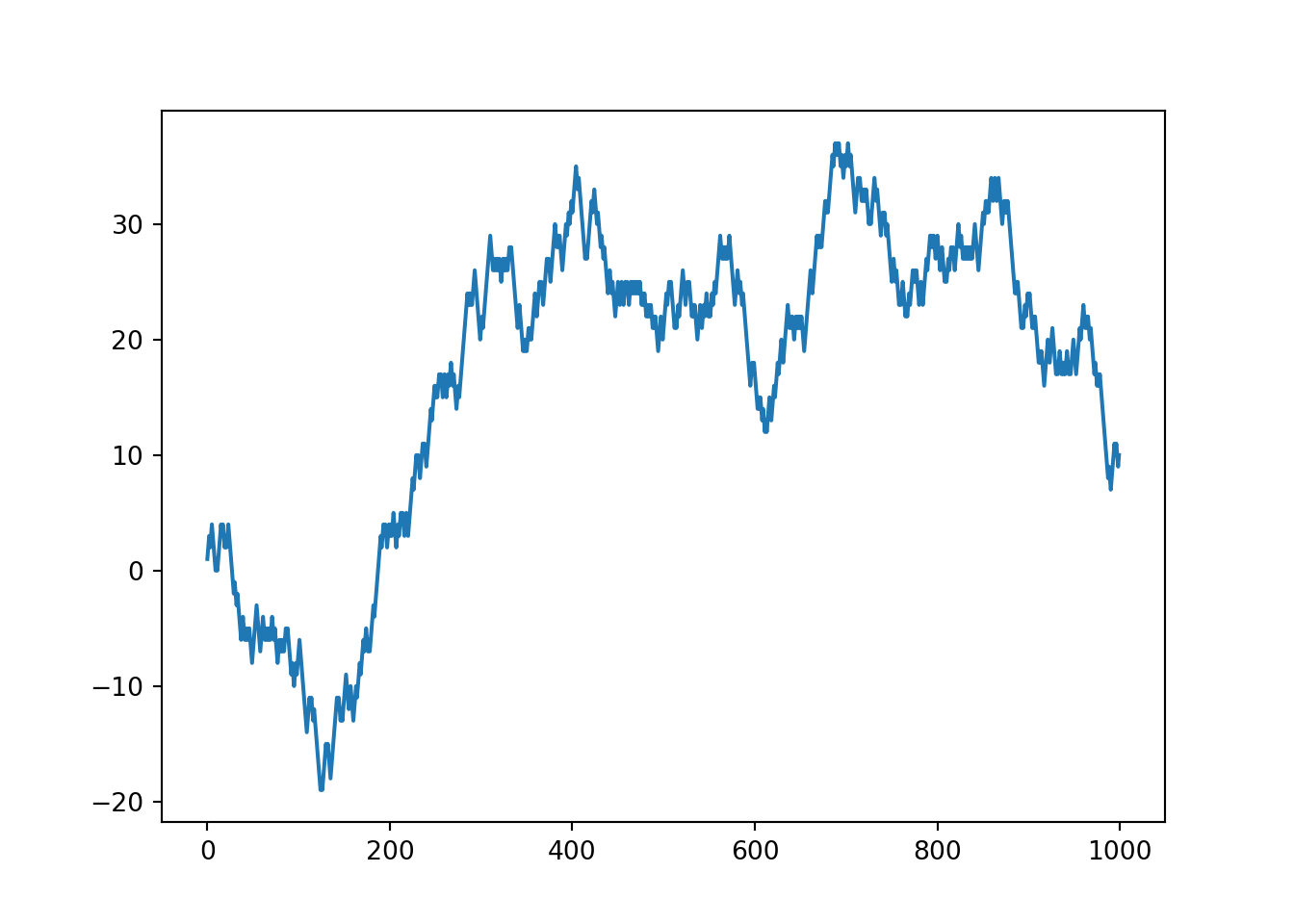

8.14 Random walk

Example

The below function will randomly add one or minus one value. This is to simulate a step in either the positive or negative direction.

random.seed(2021)

random_walk_values = []

random_walk_values.append(-1 if random.random() < 0.5 else 1)

for i in range(1, 1000):

movement = -1 if random.random() < 0.5 else 1

value = random_walk_values[i-1] + movement

random_walk_values.append(value)# plot the random walk values

plt.plot(random_walk_values)

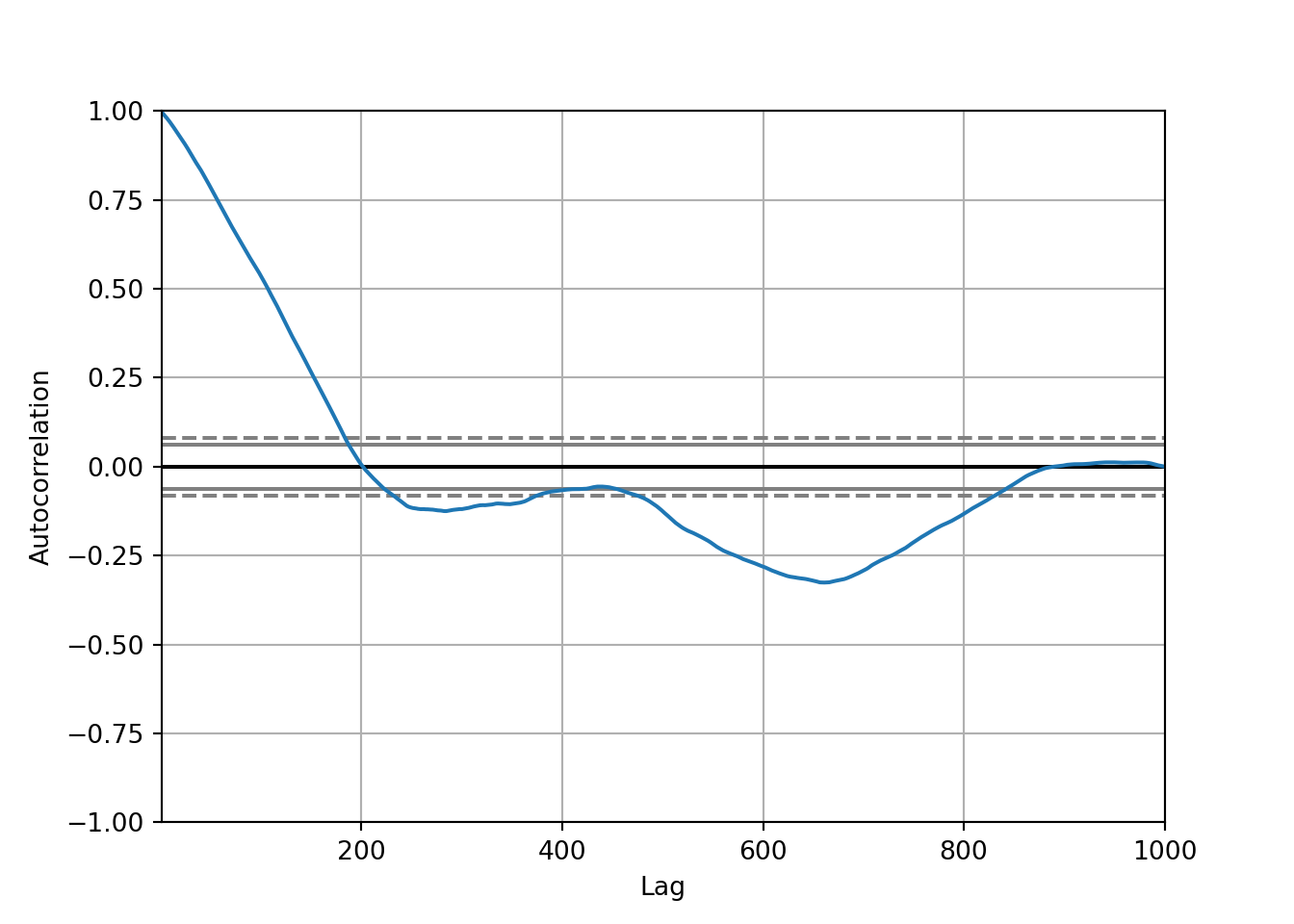

# autocorrelation plot of random walk values

autocorrelation_plot(random_walk_values)

Interpretation:

The autocorrelation starts off strong at lag 0 (as it always does) and decreases sharply as the lag increases. This is typical for many time series, where the immediate past is often more informative than the more distant past.

There are points where the autocorrelation dips below the lower confidence bound, suggesting significant negative autocorrelation at certain lags. This might indicate a cyclical pattern where the values oscillate in a fixed pattern over time.

Beyond a certain point, the autocorrelation seems to hover around zero, not crossing the significance bounds, implying no significant correlation at those lags.

We can now check the stationarity of this data using the ADF test.

# test stationarity of random walk values

adfuller(random_walk_values)(-1.326616691277989, 0.6169088978451089, 1, 998, {'1%': -3.4369193380671, '5%': -2.864440383452517, '10%': -2.56831430323573}, 2774.6156168271864)We need to differentiate the data to make it stationary.

# differentiate the data

diff = []

for i in range(1, len(random_walk_values)):

value = random_walk_values[i] - random_walk_values[i - 1]

diff.append(value)# plot the values

plt.plot(diff)

The output of this plot means that it is essentially white noise and there is no structure to the data. It is unable to be used for forecasting.

# autocorrelation plot of differentiated values

autocorrelation_plot(diff)

The autocorrelation is very close to 0 so we would have no information to give to our model.

8.15 Train-test split

First, we need to split the data into training data and test data, using the count column. It’s important to note we are using the original count column, not the differentiated column that we looked at in the last notebook. This is because the ARIMA model has a component which will automatically differentiate the data for us. When the ARIMA model gives you the results back, it will convert it to the original data, but if the differentiation is performed outside of the ARIMA, you have the difference between two months which is harder to interpret when forecasting.

bicycles_months.head() stoptime tripduration temperature count

starttime

2014-01-31 23617 23617 23617 23617

2014-02-28 26221 26221 26221 26221

2014-03-31 56020 56020 56020 56020

2014-04-30 105428 105428 105428 105428

2014-05-31 159957 159957 159957 159957series = series_df['count']Our training data will be the data before and including 31st December 2016. The test data will be everything after that.

Note: Train-test split is different to what we have previously performed, where the data was split randomly. Time series data should be split based on time to maintain the integrity of the temporal order. Typically, you would allocate the earlier portion of the data for training and the later portion for testing.

# defining train and test data

train = series[:'2015-12-31']

test = series['2015-10-31':]8.16 AR (Autoregressive) Model

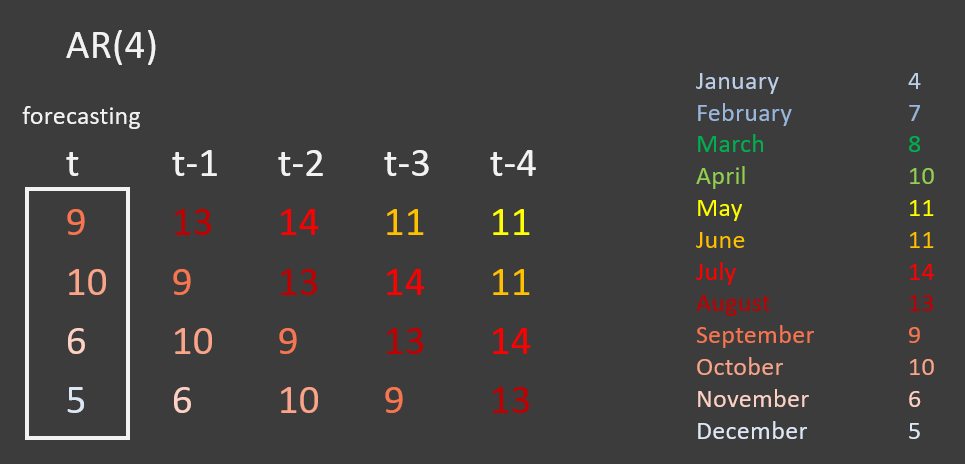

The image below shows data about the number of passengers on a certain bus route in a village. The original series, t, starts in September, but if we move backward to t-1, the series starts in August. If we move backward two units, the series starts with July, and so on.

The AR model will try to understand which predictor will be the most important - e.g, does t-1 predict t better than t-2?

This is called an AR(4) model as it is using the four previous time points to forecast the current time point, t. More generally it is called an AR(p) model.

The AR model formula:

Where \(\alpha\) is the constant (series mean),

\(\beta_n\) are the coefficients,

\(Y_{t-n}\) are the predictors,

\(\epsilon\) is the error term (white noise)

8.16.1 AR(1)

from statsmodels.tsa.arima.model import ARIMAThe ARIMA model, short for Autoregressive Integrated Moving Average, is a forecasting algorithm that is used to predict future points in a time series. It is composed of three parts:

AR (Autoregressive): The model uses the dependent relationship between an observation and some number of lagged observations (

p).I (Integrated): The model employs differencing of observations (the number of differences needed to make the series stationary, denoted by

d).MA (Moving Average): The model incorporates the dependency between an observation and a residual error from a moving average model applied to lagged observations (

q).

The model is typically denoted as ARIMA(p, d, q) where p is the order of the autoregressive terms, d is the degree of differencing, and q is the order of the moving average process.

# create the model on the train data

model = ARIMA(train, order = (1,0,0)) # 1 - number of lags

results = model.fit()

results.summary()| Dep. Variable: | count | No. Observations: | 24 |

| Model: | ARIMA(1, 0, 0) | Log Likelihood | -291.720 |

| Date: | Mon, 22 Apr 2024 | AIC | 589.441 |

| Time: | 17:09:23 | BIC | 592.975 |

| Sample: | 01-31-2014 | HQIC | 590.378 |

| - 12-31-2015 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

| const | 1.598e+05 | 5.02e+04 | 3.183 | 0.001 | 6.14e+04 | 2.58e+05 |

| ar.L1 | 0.8825 | 0.112 | 7.909 | 0.000 | 0.664 | 1.101 |

| sigma2 | 1.873e+09 | 0.643 | 2.91e+09 | 0.000 | 1.87e+09 | 1.87e+09 |

| Ljung-Box (L1) (Q): | 12.40 | Jarque-Bera (JB): | 1.50 |

| Prob(Q): | 0.00 | Prob(JB): | 0.47 |

| Heteroskedasticity (H): | 1.84 | Skew: | -0.15 |

| Prob(H) (two-sided): | 0.41 | Kurtosis: | 1.81 |

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

[2] Covariance matrix is singular or near-singular, with condition number 4.54e+25. Standard errors may be unstable.

Main points of interest from the summary of results:

There are 36 observations

AIC/BIC/HQIC - information criteria used to compare models with different numbers of parameters. They take into account the goodness of fit and the complexity of the model (penalizing for more parameters). A lower value indicates a better model according to that criterion

Coefficient - the constant is usually the mean of the series.

ar.L1 - this means we used one lag, and the coefficient (\(\beta\)) is 0.88

sigma2 - the error term.

P>|z| - The p-value associated with the z-test for each coefficient, testing the null hypothesis that the coefficient is zero against the alternative that it is not zero.

Ljung-Box (Q) - A test statistic for the null hypothesis that the model does not show lack of fit, i.e., the residuals are independently distributed. A small p-value (Prob(Q)) indicates that the residuals are uncorrelated.(white noise)

Jarque-Bera (JB) - A test statistic for the null hypothesis that the residuals are normally distributed. The p-value (Prob(JB)) indicates whether the residuals depart from normality.

Heteroskedasticity (H) - a test statistic for the null hypothesis that the residuals have constant variance (are homoskedastic). A high p-value (Prob(H)) indicates that you cannot reject the null of homoskedasticity.

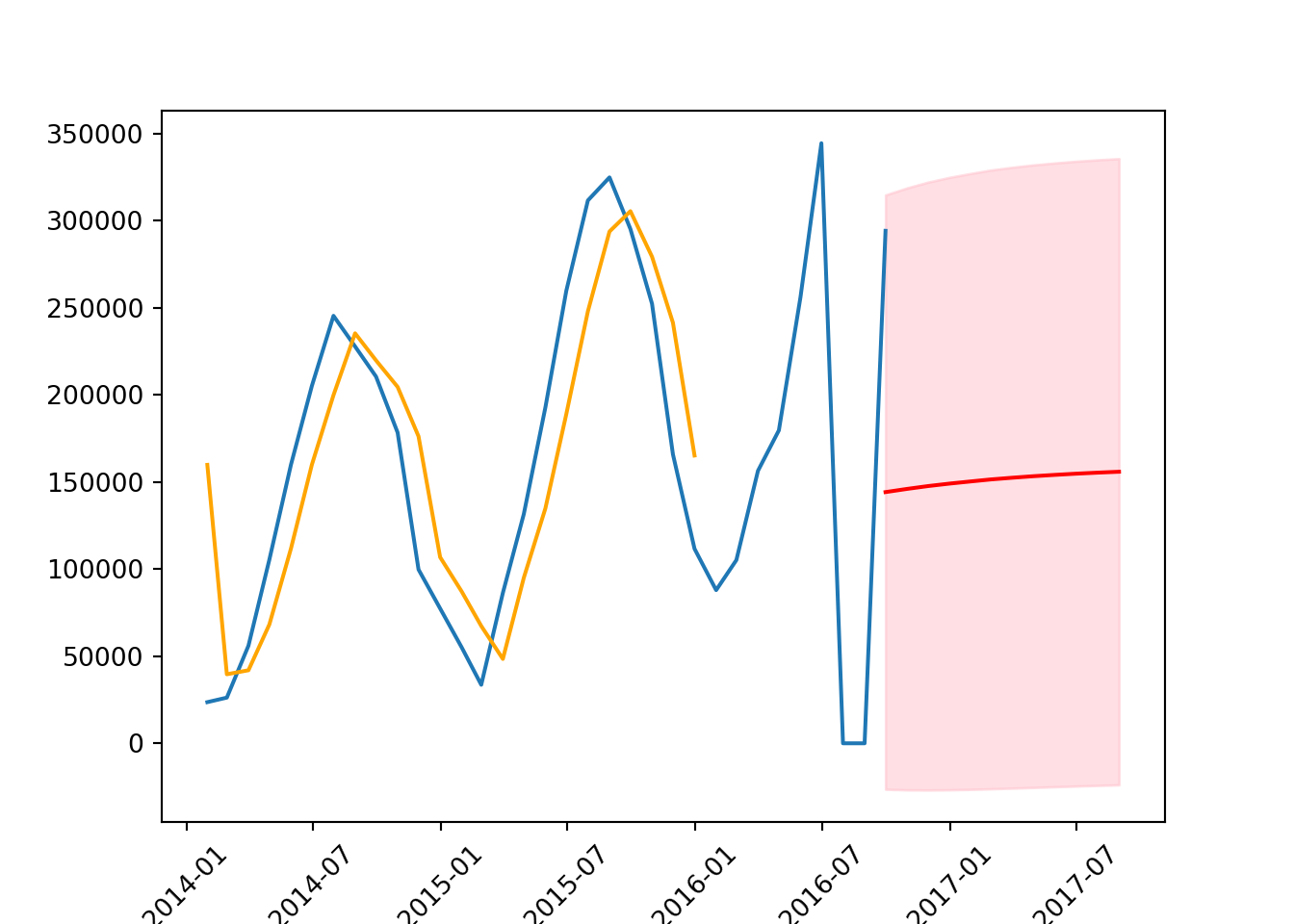

train.mean()159841.33333333334We can also get some predictions by using get_prediction, specifying the time period that we want to predict.

# get prediction

forecast = results.get_prediction(start = '2016-09-30', end = '2017-08-31')confidence_intervals = forecast.conf_int()

confidence_intervals lower count upper count

2016-09-30 -26377.582236 314771.380240

2016-10-31 -26747.095132 318817.819387

2016-11-30 -26824.853416 322140.408188

2016-12-31 -26705.767775 324884.835265

2017-01-31 -26457.795300 327163.868451

2017-02-28 -26129.625185 329065.741726

2017-03-31 -25756.012865 330660.108189

2017-04-30 -25361.562085 332002.368231

2017-05-31 -24963.450032 333136.876604

2017-06-30 -24573.414499 334099.354879

2017-07-31 -24199.215410 334918.728295

2017-08-31 -23845.716039 335618.538190Confidence intervals may be useful to us, because they represent the pessimistic and optimistic margins.

Pessimistic margins - the lower values the model has given us. They consider the worst possibilities but often overestimate the worst-case scenario

Optimistic margins - the upper values the model has given us. This would be the best case scenario.

The mean will be the average of these two values.

# mean of the forecasting values

forecast_mean = forecast.predicted_meanforecast_mean2016-09-30 144196.899002

2016-10-31 146035.362128

2016-11-30 147657.777386

2016-12-31 149089.533745

2017-01-31 150353.036575

2017-02-28 151468.058271

2017-03-31 152452.047662

2017-04-30 153320.403073

2017-05-31 154086.713286

2017-06-30 154762.970190

2017-07-31 155359.756443

2017-08-31 155886.411076

Freq: ME, Name: predicted_mean, dtype: float64We can now plot the forecasted values.

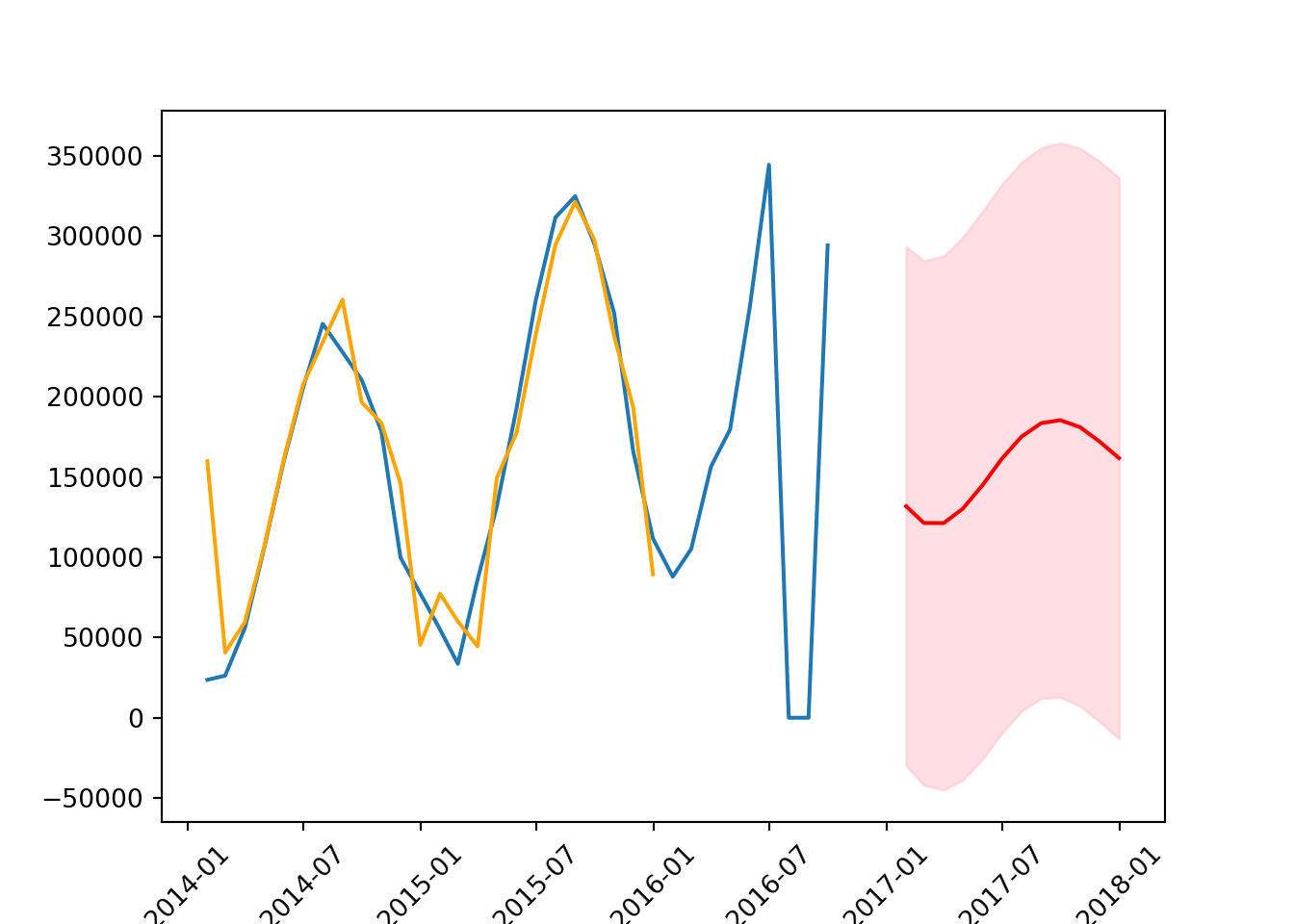

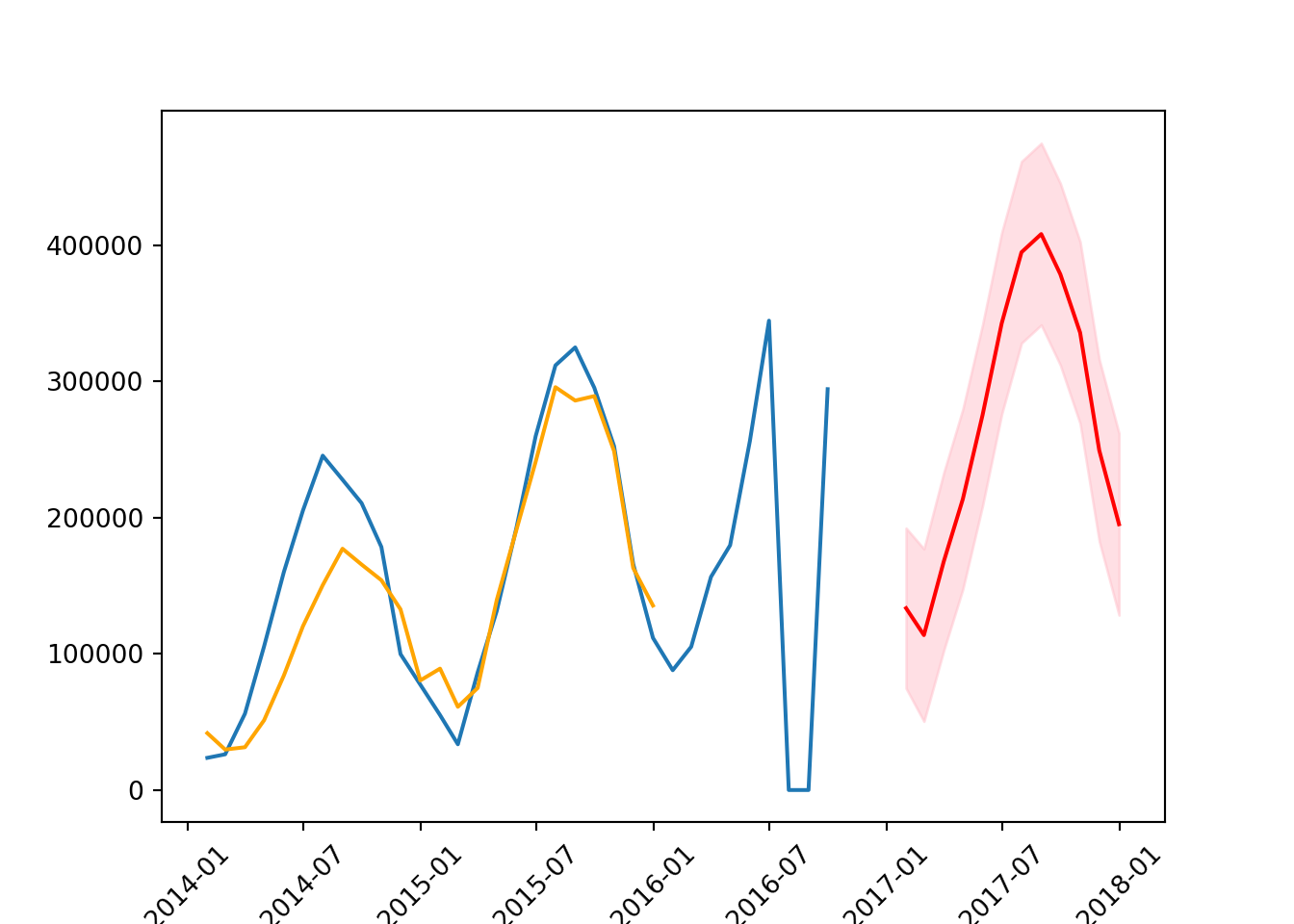

plt.plot(series) # the original data

plt.plot(results.fittedvalues, # estimated values from the model

color = 'orange',

label = 'forecast')

plt.plot(forecast_mean, color = 'red') # forecast mean

plt.fill_between(forecast_mean.index, # display the lower and upper count

confidence_intervals['lower count'],

confidence_intervals['upper count'],

color = 'pink',

alpha = 0.5)

plt.xticks(rotation = 45);

The margins are very large. This means the model is very uncertain and often the further into the future you go, the wider the margin will be.

We can also comput the mean squared error, to evaluate the accuracy of a model’s prediction. The “squared” aspect emphasises larger errors over smaller ones, meaning it punishes large errors more severely than small ones, which can be particularly useful in identifying models that might occasionally be very inaccurate.

Lower MSE: Indicates a model that predicts the observed data with higher accuracy. A lower MSE is generally preferable, as it means the model’s predictions are closer to the actual values.

Higher MSE: Indicates that the model’s predictions deviate more significantly from the actual observed values. A high MSE suggests the model may not be capturing the underlying pattern of the series effectively.

from sklearn.metrics import mean_squared_error

mean_squared_error(test, forecast_mean, squared = False) # returns root mean squared error (RMSE)105656.8487371978

C:\Users\GEORGI~1\AppData\Local\Programs\Python\PYTHON~1\Lib\site-packages\sklearn\metrics\_regression.py:483: FutureWarning: 'squared' is deprecated in version 1.4 and will be removed in 1.6. To calculate the root mean squared error, use the function'root_mean_squared_error'.

warnings.warn(In the context of bike trips, it means that, on average, the model’s predictions were about 105,656 trips different from the actual numbers.

Now we can try an AR model with two lags rather than one, to see if this will improve the results.

8.16.2 AR(2)

# create model

model = ARIMA(train, order = (2,0,0))

results = model.fit()

# summarise results

results.summary()| Dep. Variable: | count | No. Observations: | 24 |

| Model: | ARIMA(2, 0, 0) | Log Likelihood | -275.985 |

| Date: | Mon, 22 Apr 2024 | AIC | 559.970 |

| Time: | 17:09:29 | BIC | 564.683 |

| Sample: | 01-31-2014 | HQIC | 561.220 |

| - 12-31-2015 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

| const | 1.598e+05 | 2.08e+04 | 7.691 | 0.000 | 1.19e+05 | 2.01e+05 |

| ar.L1 | 1.6357 | 0.102 | 16.058 | 0.000 | 1.436 | 1.835 |

| ar.L2 | -0.8695 | 0.100 | -8.701 | 0.000 | -1.065 | -0.674 |

| sigma2 | 4.686e+08 | 0.684 | 6.85e+08 | 0.000 | 4.69e+08 | 4.69e+08 |

| Ljung-Box (L1) (Q): | 4.21 | Jarque-Bera (JB): | 0.49 |

| Prob(Q): | 0.04 | Prob(JB): | 0.78 |

| Heteroskedasticity (H): | 1.06 | Skew: | -0.13 |

| Prob(H) (two-sided): | 0.94 | Kurtosis: | 2.35 |

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

[2] Covariance matrix is singular or near-singular, with condition number 3.89e+24. Standard errors may be unstable.

# get predictions and confidence intervals

forecast = results.get_prediction(start = '2017-01-31', end = '2017-12-31')

forecast_mean = forecast.predicted_mean

confidence_intervals = forecast.conf_int()# plot the data

plt.plot(series)

plt.plot(results.fittedvalues,

color = 'orange',

label = 'forecast')

plt.plot(forecast_mean, color = 'red')

plt.fill_between(forecast_mean.index,

confidence_intervals['lower count'],

confidence_intervals['upper count'],

color = 'pink',

alpha = 0.5)

plt.xticks(rotation = 45);

The forecast is more accurate than it was with AR(1) but needs to be shifted up a little to more accurately reflect the data. Additionally, the orange line is pretty accurately estimating the values.

# RMSE

mean_squared_error(test, forecast_mean, squared = False) # smaller or larger RMSE?104316.4891780201

C:\Users\GEORGI~1\AppData\Local\Programs\Python\PYTHON~1\Lib\site-packages\sklearn\metrics\_regression.py:483: FutureWarning: 'squared' is deprecated in version 1.4 and will be removed in 1.6. To calculate the root mean squared error, use the function'root_mean_squared_error'.

warnings.warn(8.17 MA (Moving Average) model

The Moving Average (MA) model removes random movements from a time series model. Unlike models that rely solely on the historical values of the dataset (like the Autoregressive models), the MA model focuses on modeling the error term (residuals) of the predictions.

Where \(\alpha\) is the constants,

\(\phi\) is the parameters that need to be estimated (weight),

\(\epsilon\) is the white noise (error term)

8.17.1 MA(1)

# create the model

model = ARIMA(train, order = (0,0,1))

results = model.fit()C:\Users\GEORGI~1\AppData\Local\Programs\Python\PYTHON~1\Lib\site-packages\statsmodels\tsa\statespace\sarimax.py:978: UserWarning: Non-invertible starting MA parameters found. Using zeros as starting parameters.

warn('Non-invertible starting MA parameters found.'results.summary()| Dep. Variable: | count | No. Observations: | 24 |

| Model: | ARIMA(0, 0, 1) | Log Likelihood | -298.997 |

| Date: | Mon, 22 Apr 2024 | AIC | 603.994 |

| Time: | 17:09:32 | BIC | 607.528 |

| Sample: | 01-31-2014 | HQIC | 604.931 |

| - 12-31-2015 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

| const | 1.598e+05 | 4.69e+04 | 3.405 | 0.001 | 6.78e+04 | 2.52e+05 |

| ma.L1 | 0.9058 | 0.793 | 1.142 | 0.253 | -0.649 | 2.460 |

| sigma2 | 6.595e+09 | 0.047 | 1.4e+11 | 0.000 | 6.6e+09 | 6.6e+09 |

| Ljung-Box (L1) (Q): | 14.58 | Jarque-Bera (JB): | 0.84 |

| Prob(Q): | 0.00 | Prob(JB): | 0.66 |

| Heteroskedasticity (H): | 1.31 | Skew: | 0.02 |

| Prob(H) (two-sided): | 0.71 | Kurtosis: | 2.08 |

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

[2] Covariance matrix is singular or near-singular, with condition number 5.13e+27. Standard errors may be unstable.

Ljung-Box test - prob(Q) value of 0.00 suggests that there is no autocorrelation at lag 1, indicating good model fit.

Jarque-Bera test - prob(JB) value of 0.52 suggests that the residuals are normally distributed.

Heteroskedasticity test - prob(H) (two-sided) value of 0.60 suggests no significant heteroskedasticity, meaning the error variance is fairly constant.

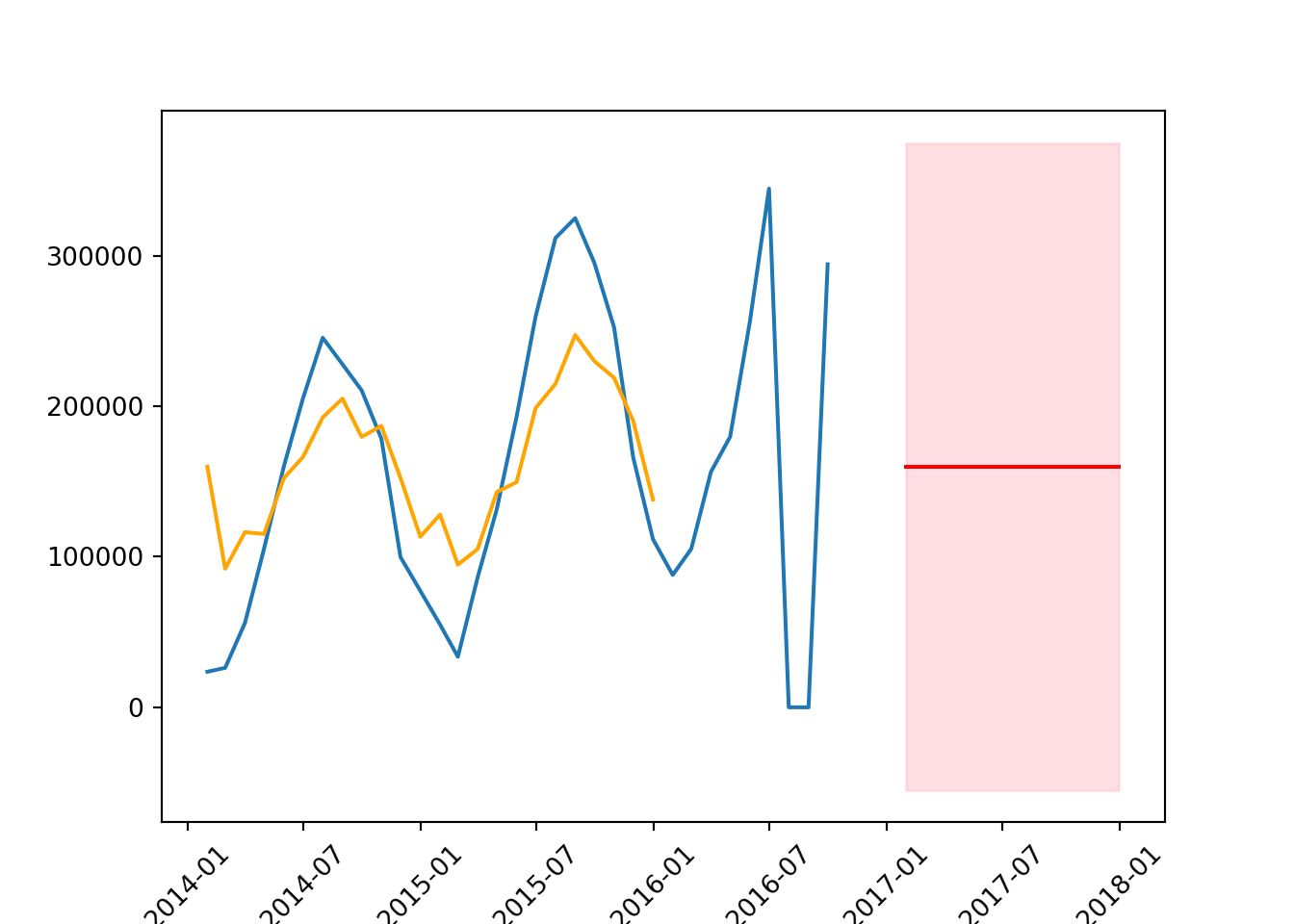

# get forecast, means, confidence intervals

forecast = results.get_prediction(start = '2017-01-31', end = '2017-12-31')

forecast_mean = forecast.predicted_mean

confidence_intervals = forecast.conf_int()# plot the data

plt.plot(series)

plt.plot(results.fittedvalues,

color = 'orange',

label = 'forecast')

plt.plot(forecast_mean, color = 'red')

plt.fill_between(forecast_mean.index,

confidence_intervals['lower count'],

confidence_intervals['upper count'],

color = 'pink',

alpha = 0.5)

plt.xticks(rotation = 45);

mean_squared_error(test, forecast_mean, squared = False)104874.51864512012

C:\Users\GEORGI~1\AppData\Local\Programs\Python\PYTHON~1\Lib\site-packages\sklearn\metrics\_regression.py:483: FutureWarning: 'squared' is deprecated in version 1.4 and will be removed in 1.6. To calculate the root mean squared error, use the function'root_mean_squared_error'.

warnings.warn(8.18 ARMA

This is a combination of the AR and MA models.

# create the model

model = ARIMA(train, order = (1,0,1))

results = model.fit()

results.summary()| Dep. Variable: | count | No. Observations: | 24 |

| Model: | ARIMA(1, 0, 1) | Log Likelihood | -285.879 |

| Date: | Mon, 22 Apr 2024 | AIC | 579.758 |

| Time: | 17:09:34 | BIC | 584.471 |

| Sample: | 01-31-2014 | HQIC | 581.009 |

| - 12-31-2015 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

| const | 1.598e+05 | 8.76e+04 | 1.825 | 0.068 | -1.18e+04 | 3.31e+05 |

| ar.L1 | 0.7809 | 0.357 | 2.190 | 0.029 | 0.082 | 1.480 |

| ma.L1 | 0.8630 | 0.413 | 2.089 | 0.037 | 0.053 | 1.673 |

| sigma2 | 1.969e+09 | 0.203 | 9.72e+09 | 0.000 | 1.97e+09 | 1.97e+09 |

| Ljung-Box (L1) (Q): | 2.57 | Jarque-Bera (JB): | 0.83 |

| Prob(Q): | 0.11 | Prob(JB): | 0.66 |

| Heteroskedasticity (H): | 1.67 | Skew: | -0.16 |

| Prob(H) (two-sided): | 0.48 | Kurtosis: | 2.15 |

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

[2] Covariance matrix is singular or near-singular, with condition number 1.11e+27. Standard errors may be unstable.

# get forecast, means, confidence intervals

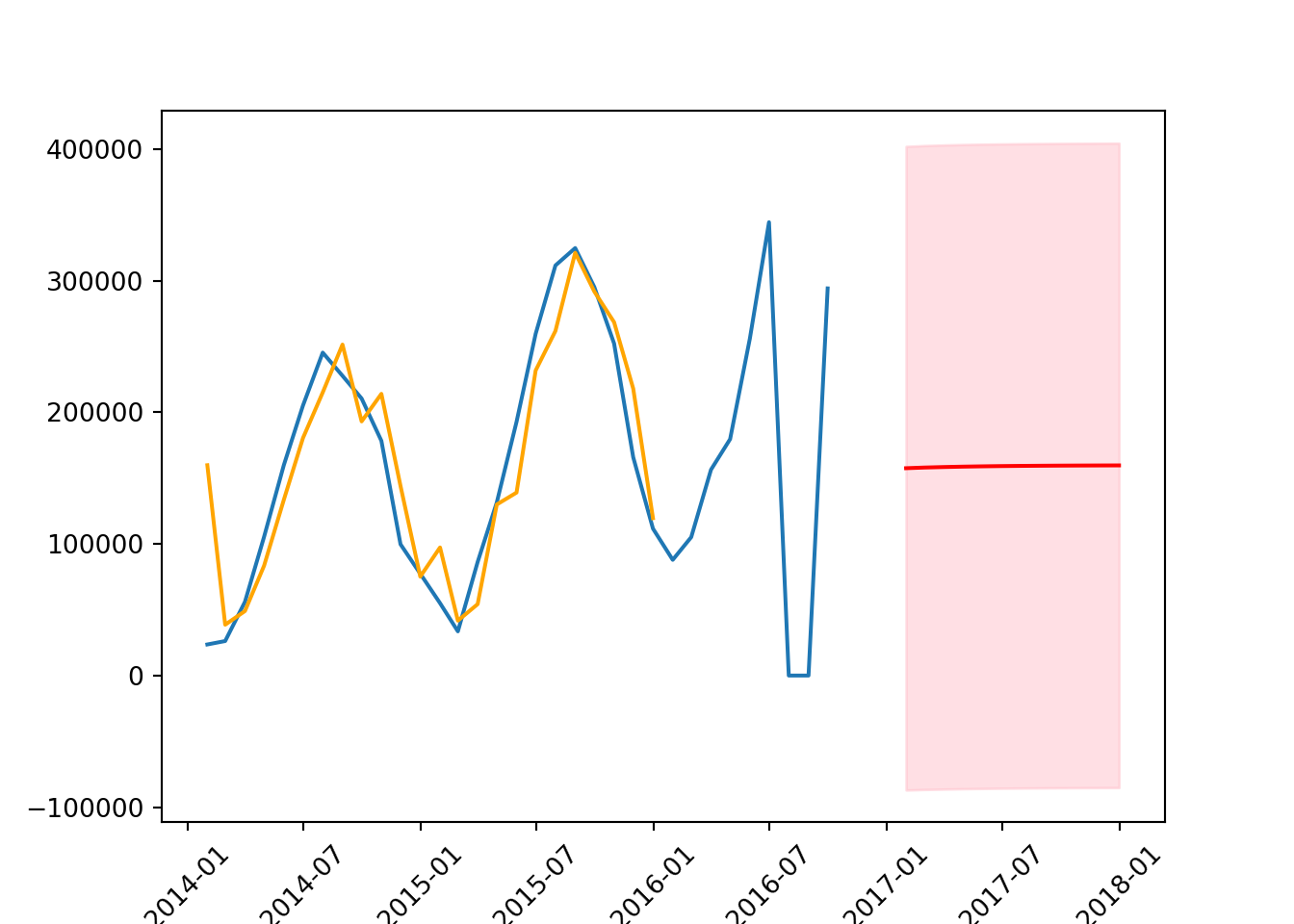

forecast = results.get_prediction(start = '2017-01-31', end = '2017-12-31')

forecast_mean = forecast.predicted_mean

confidence_intervals = forecast.conf_int()# plot the data

plt.plot(series)

plt.plot(results.fittedvalues,

color = 'orange',

label = 'forecast')

plt.plot(forecast_mean, color = 'red')

plt.fill_between(forecast_mean.index,

confidence_intervals['lower count'],

confidence_intervals['upper count'],

color = 'pink',

alpha = 0.5)

plt.xticks(rotation = 45);

mean_squared_error(test, forecast_mean, squared = False)104947.85308784364

C:\Users\GEORGI~1\AppData\Local\Programs\Python\PYTHON~1\Lib\site-packages\sklearn\metrics\_regression.py:483: FutureWarning: 'squared' is deprecated in version 1.4 and will be removed in 1.6. To calculate the root mean squared error, use the function'root_mean_squared_error'.

warnings.warn(8.19 SARIMAX Model

The Seasonal AutoRegressive Integrated Moving Average with eXogenous variables model, or SARIMAX, is an extension of the ARIMA model used for time series forecasting. It incorporates both non-seasonal and seasonal elements, as well as external factors, making it particularly useful when the data show patterns not just at different times of the year but also when external variables influence the series.

The ‘X’ in SARIMAX stands for ‘exogenous variables’. These are external variables or predictors not part of the time series itself but can influence the target variable’s values. Including exogenous variables allows the model to account for factors that could impact the forecasting accuracy.

from statsmodels.tsa.statespace.sarimax import SARIMAXThe general model for SARIMAX is as follows:

SARIMAX(p, d, q)(P, D, Q)s

Non-Seasonal Components:

p: AutoRegressive order. Number of lag observations.

d: Degree of differencing. Number of times the data are differenced to achieve stationarity.

q: Moving Average order. Number of lagged forecast errors.

Seasonal Components:

P: Seasonal AutoRegressive order.

D: Seasonal differencing degree.

Q: Seasonal Moving Average order.

s: number of lags. For example, s=7 => we will use the values from one week ago to forecast the tomorrow’s value.

model = SARIMAX(endog=train,

order=(1, 1, 1),

seasonal_order=(1, 0, 0, 12)) # monthly data with annual cycle

results = model.fit()C:\Users\GEORGI~1\AppData\Local\Programs\Python\PYTHON~1\Lib\site-packages\statsmodels\tsa\statespace\sarimax.py:997: UserWarning: Non-stationary starting seasonal autoregressive Using zeros as starting parameters.

warn('Non-stationary starting seasonal autoregressive'results.summary()| Dep. Variable: | count | No. Observations: | 24 |

| Model: | SARIMAX(1, 1, 1)x(1, 0, [], 12) | Log Likelihood | -267.575 |

| Date: | Mon, 22 Apr 2024 | AIC | 543.150 |

| Time: | 17:09:37 | BIC | 547.692 |

| Sample: | 01-31-2014 | HQIC | 544.293 |

| - 12-31-2015 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

| ar.L1 | 0.7066 | 0.445 | 1.587 | 0.113 | -0.166 | 1.579 |

| ma.L1 | 0.0768 | 0.789 | 0.097 | 0.922 | -1.470 | 1.623 |

| ar.S.L12 | 0.5016 | 0.379 | 1.324 | 0.185 | -0.241 | 1.244 |

| sigma2 | 9.846e+08 | 4.66e-10 | 2.11e+18 | 0.000 | 9.85e+08 | 9.85e+08 |

| Ljung-Box (L1) (Q): | 0.01 | Jarque-Bera (JB): | 0.01 |

| Prob(Q): | 0.91 | Prob(JB): | 1.00 |

| Heteroskedasticity (H): | 0.91 | Skew: | -0.01 |

| Prob(H) (two-sided): | 0.90 | Kurtosis: | 2.93 |

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

[2] Covariance matrix is singular or near-singular, with condition number 3.17e+34. Standard errors may be unstable.

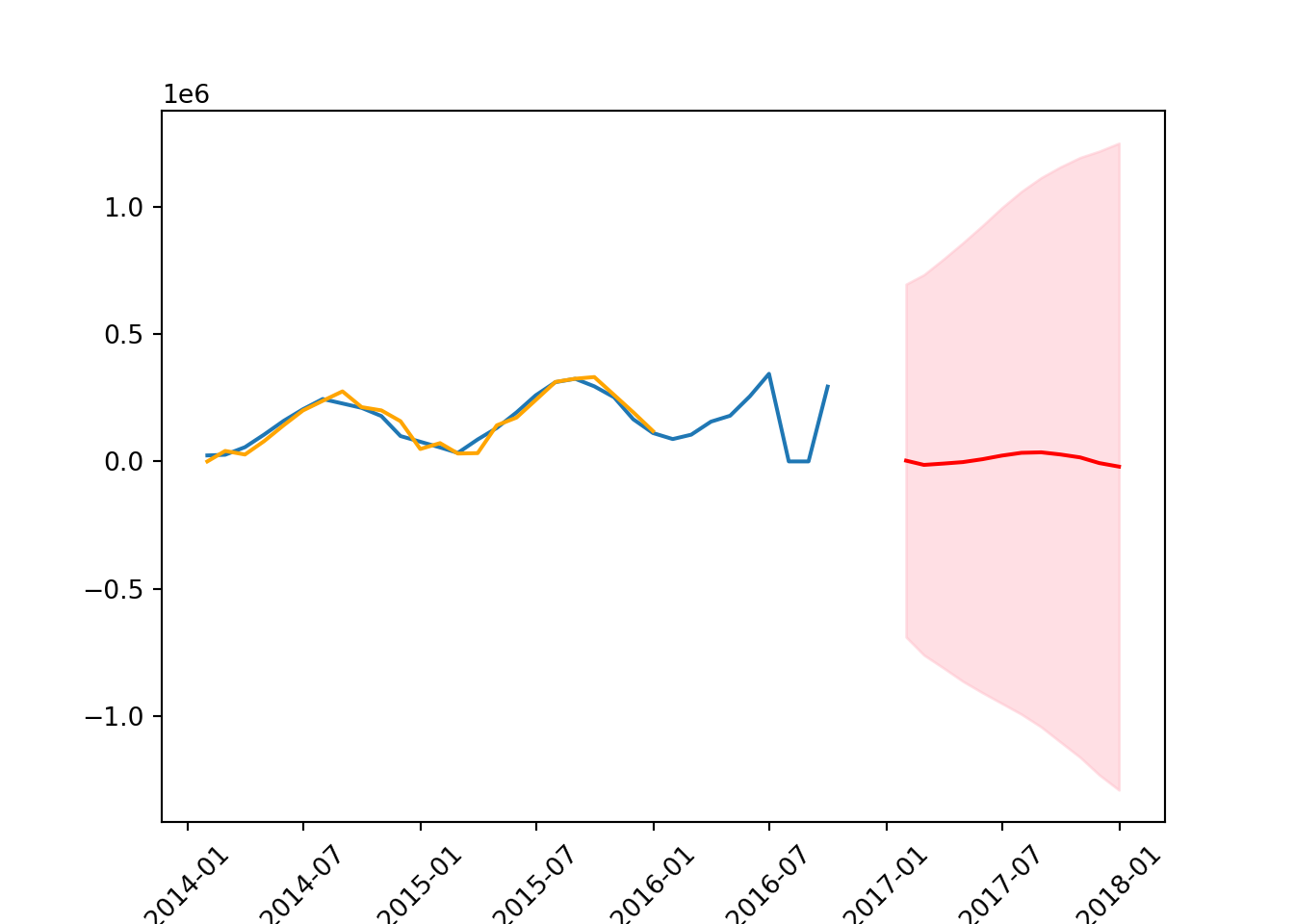

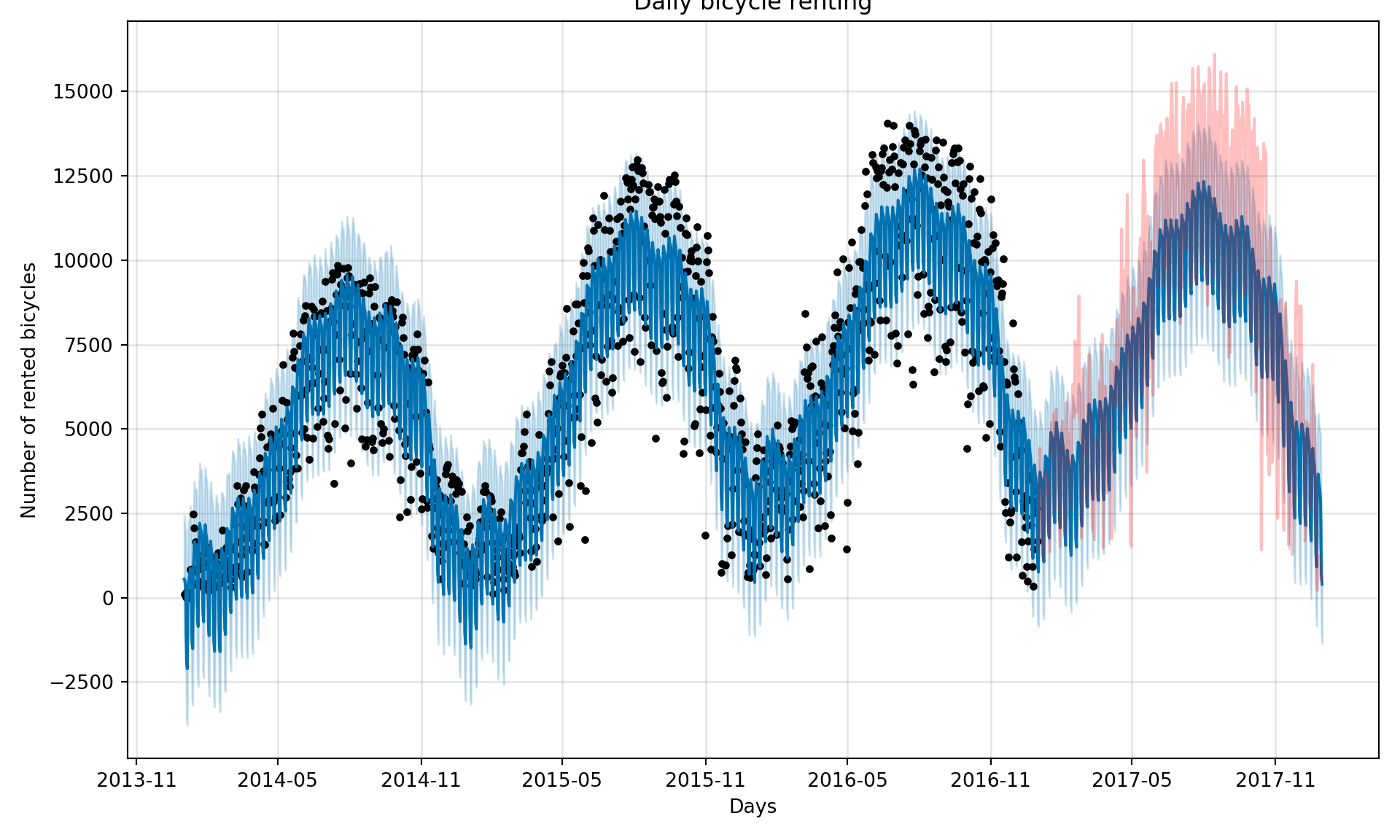

forecast = results.get_prediction(start = '2017-01-31', end = '2017-12-31')

forecast_mean = forecast.predicted_mean

confidence_intervals = forecast.conf_int()plt.plot(series)

plt.plot(results.fittedvalues,

color = 'orange',

label = 'forecast')

plt.plot(forecast_mean, color = 'red')

plt.fill_between(forecast_mean.index,

confidence_intervals['lower count'],

confidence_intervals['upper count'],

color = 'pink',

alpha = 0.5)

plt.xticks(rotation = 45);

mean_squared_error(test, forecast_mean, squared = False)185672.92610518975

C:\Users\GEORGI~1\AppData\Local\Programs\Python\PYTHON~1\Lib\site-packages\sklearn\metrics\_regression.py:483: FutureWarning: 'squared' is deprecated in version 1.4 and will be removed in 1.6. To calculate the root mean squared error, use the function'root_mean_squared_error'.

warnings.warn(8.20 Auto ARIMA

Auto ARIMA manually selects the best ARIMA model by evaluating various combinations of parameters.

It automates the following steps: 1. It tests the stationarity of the data and applies the necessary differencing to make the series stationary. 2. It iteratively explores different combinations of p, d, and q values (and also P, D, Q for seasonal data) to find the best model according to a given criterion, usually the AIC (Akaike Information Criterion), BIC (Bayesian Information Criterion), or similar. 3. Once the best parameters are identified, it fits the ARIMA model to the data, allowing for predictions to be made.

import pmdarima as pmdDocumentation: https://alkaline-ml.com/pmdarima/modules/generated/pmdarima.arima.auto_arima.html

We need to set up an initial range for the series, with the following parameters:

# set up parameters

results = pmd.auto_arima(series,

start_p=0, # initial guess for AR(p)

start_d=0, # initial guess for I(d)

start_q=0, # initial guess for MA(q)

max_p=5, # max guess for AR(p)

max_d=2, # max guess for I(d)

max_q=5, # max guess for MA(q)

m=12, # seasonal order

start_P=0, # initial guess for seasonal AR(P)

start_D=0, # initial guess for seasonal I(D)

start_Q=0, # initial guess for seasonal MA(Q)

max_P = 3,

max_D = 1,

max_Q = 3,

information_criterion='bic',

trace=True,

error_action='ignore',

stepwise = False

) ARIMA(0,0,0)(0,1,0)[12] intercept : BIC=553.755, Time=0.01 sec

ARIMA(0,0,0)(0,1,1)[12] intercept : BIC=555.356, Time=0.27 sec

ARIMA(0,0,0)(0,1,2)[12] intercept : BIC=556.037, Time=0.09 sec

ARIMA(0,0,0)(0,1,3)[12] intercept : BIC=558.952, Time=0.15 sec

ARIMA(0,0,0)(1,1,0)[12] intercept : BIC=556.615, Time=0.02 sec

ARIMA(0,0,0)(1,1,1)[12] intercept : BIC=557.199, Time=0.05 sec

ARIMA(0,0,0)(1,1,2)[12] intercept : BIC=558.958, Time=0.12 sec

ARIMA(0,0,0)(1,1,3)[12] intercept : BIC=561.996, Time=0.42 sec

ARIMA(0,0,0)(2,1,0)[12] intercept : BIC=555.865, Time=0.04 sec

ARIMA(0,0,0)(2,1,1)[12] intercept : BIC=558.900, Time=0.10 sec

ARIMA(0,0,0)(2,1,2)[12] intercept : BIC=561.925, Time=0.74 sec

ARIMA(0,0,0)(2,1,3)[12] intercept : BIC=564.903, Time=1.33 sec

ARIMA(0,0,0)(3,1,0)[12] intercept : BIC=558.907, Time=0.14 sec

ARIMA(0,0,0)(3,1,1)[12] intercept : BIC=561.795, Time=0.48 sec

ARIMA(0,0,0)(3,1,2)[12] intercept : BIC=564.840, Time=0.32 sec

ARIMA(0,0,1)(0,1,0)[12] intercept : BIC=545.422, Time=0.02 sec

ARIMA(0,0,1)(0,1,1)[12] intercept : BIC=547.185, Time=0.04 sec

ARIMA(0,0,1)(0,1,2)[12] intercept : BIC=549.993, Time=0.51 sec

ARIMA(0,0,1)(0,1,3)[12] intercept : BIC=552.946, Time=0.91 sec

ARIMA(0,0,1)(1,1,0)[12] intercept : BIC=547.866, Time=0.03 sec

ARIMA(0,0,1)(1,1,1)[12] intercept : BIC=550.087, Time=0.10 sec

ARIMA(0,0,1)(1,1,2)[12] intercept : BIC=552.998, Time=0.85 sec

ARIMA(0,0,1)(1,1,3)[12] intercept : BIC=555.989, Time=0.41 sec

ARIMA(0,0,1)(2,1,0)[12] intercept : BIC=549.900, Time=0.08 sec

ARIMA(0,0,1)(2,1,1)[12] intercept : BIC=552.944, Time=0.12 sec

ARIMA(0,0,1)(2,1,2)[12] intercept : BIC=555.986, Time=0.20 sec

ARIMA(0,0,1)(3,1,0)[12] intercept : BIC=552.945, Time=0.60 sec

ARIMA(0,0,1)(3,1,1)[12] intercept : BIC=inf, Time=2.36 sec

ARIMA(0,0,2)(0,1,0)[12] intercept : BIC=549.947, Time=0.02 sec

ARIMA(0,0,2)(0,1,1)[12] intercept : BIC=552.429, Time=0.04 sec

ARIMA(0,0,2)(0,1,2)[12] intercept : BIC=555.136, Time=0.27 sec

ARIMA(0,0,2)(0,1,3)[12] intercept : BIC=558.092, Time=0.17 sec

ARIMA(0,0,2)(1,1,0)[12] intercept : BIC=552.821, Time=0.05 sec

ARIMA(0,0,2)(1,1,1)[12] intercept : BIC=555.301, Time=0.07 sec

ARIMA(0,0,2)(1,1,2)[12] intercept : BIC=558.123, Time=0.16 sec

ARIMA(0,0,2)(2,1,0)[12] intercept : BIC=555.038, Time=0.32 sec

ARIMA(0,0,2)(2,1,1)[12] intercept : BIC=558.083, Time=0.20 sec

ARIMA(0,0,2)(3,1,0)[12] intercept : BIC=558.083, Time=0.18 sec

ARIMA(0,0,3)(0,1,0)[12] intercept : BIC=554.455, Time=0.03 sec

ARIMA(0,0,3)(0,1,1)[12] intercept : BIC=555.979, Time=0.07 sec

ARIMA(0,0,3)(0,1,2)[12] intercept : BIC=559.018, Time=0.53 sec

ARIMA(0,0,3)(1,1,0)[12] intercept : BIC=556.558, Time=0.06 sec

ARIMA(0,0,3)(1,1,1)[12] intercept : BIC=559.023, Time=0.10 sec

ARIMA(0,0,3)(2,1,0)[12] intercept : BIC=559.067, Time=0.30 sec

ARIMA(0,0,4)(0,1,0)[12] intercept : BIC=571.587, Time=0.13 sec

ARIMA(0,0,4)(0,1,1)[12] intercept : BIC=574.537, Time=0.11 sec

ARIMA(0,0,4)(1,1,0)[12] intercept : BIC=574.620, Time=0.09 sec

ARIMA(0,0,5)(0,1,0)[12] intercept : BIC=inf, Time=0.48 sec

ARIMA(1,0,0)(0,1,0)[12] intercept : BIC=551.230, Time=0.01 sec

ARIMA(1,0,0)(0,1,1)[12] intercept : BIC=553.951, Time=0.03 sec

ARIMA(1,0,0)(0,1,2)[12] intercept : BIC=556.015, Time=0.07 sec

ARIMA(1,0,0)(0,1,3)[12] intercept : BIC=559.030, Time=0.16 sec

ARIMA(1,0,0)(1,1,0)[12] intercept : BIC=554.246, Time=0.03 sec

ARIMA(1,0,0)(1,1,1)[12] intercept : BIC=556.421, Time=0.25 sec

ARIMA(1,0,0)(1,1,2)[12] intercept : BIC=559.012, Time=0.11 sec

ARIMA(1,0,0)(1,1,3)[12] intercept : BIC=562.025, Time=0.31 sec

ARIMA(1,0,0)(2,1,0)[12] intercept : BIC=555.983, Time=0.28 sec

ARIMA(1,0,0)(2,1,1)[12] intercept : BIC=559.022, Time=0.19 sec

ARIMA(1,0,0)(2,1,2)[12] intercept : BIC=562.053, Time=0.19 sec

ARIMA(1,0,0)(3,1,0)[12] intercept : BIC=559.027, Time=1.40 sec

ARIMA(1,0,0)(3,1,1)[12] intercept : BIC=561.988, Time=0.54 sec

ARIMA(1,0,1)(0,1,0)[12] intercept : BIC=548.423, Time=0.03 sec

ARIMA(1,0,1)(0,1,1)[12] intercept : BIC=550.163, Time=0.10 sec

ARIMA(1,0,1)(0,1,2)[12] intercept : BIC=552.935, Time=0.18 sec

ARIMA(1,0,1)(0,1,3)[12] intercept : BIC=555.859, Time=0.49 sec

ARIMA(1,0,1)(1,1,0)[12] intercept : BIC=550.877, Time=0.08 sec

ARIMA(1,0,1)(1,1,1)[12] intercept : BIC=553.050, Time=0.25 sec

ARIMA(1,0,1)(1,1,2)[12] intercept : BIC=555.929, Time=0.36 sec

ARIMA(1,0,1)(2,1,0)[12] intercept : BIC=552.812, Time=0.18 sec

ARIMA(1,0,1)(2,1,1)[12] intercept : BIC=555.856, Time=0.40 sec

ARIMA(1,0,1)(3,1,0)[12] intercept : BIC=555.856, Time=0.57 sec

ARIMA(1,0,2)(0,1,0)[12] intercept : BIC=552.576, Time=0.05 sec

ARIMA(1,0,2)(0,1,1)[12] intercept : BIC=555.270, Time=0.12 sec

ARIMA(1,0,2)(0,1,2)[12] intercept : BIC=557.765, Time=0.58 sec

ARIMA(1,0,2)(1,1,0)[12] intercept : BIC=555.517, Time=0.09 sec

ARIMA(1,0,2)(1,1,1)[12] intercept : BIC=558.065, Time=0.55 sec

ARIMA(1,0,2)(2,1,0)[12] intercept : BIC=557.590, Time=1.03 sec

ARIMA(1,0,3)(0,1,0)[12] intercept : BIC=555.851, Time=0.07 sec

ARIMA(1,0,3)(0,1,1)[12] intercept : BIC=557.725, Time=0.11 sec

ARIMA(1,0,3)(1,1,0)[12] intercept : BIC=558.368, Time=0.12 sec

ARIMA(1,0,4)(0,1,0)[12] intercept : BIC=572.657, Time=0.09 sec

ARIMA(2,0,0)(0,1,0)[12] intercept : BIC=548.138, Time=0.21 sec

ARIMA(2,0,0)(0,1,1)[12] intercept : BIC=549.821, Time=0.06 sec

ARIMA(2,0,0)(0,1,2)[12] intercept : BIC=551.091, Time=0.10 sec

ARIMA(2,0,0)(0,1,3)[12] intercept : BIC=553.832, Time=0.19 sec

ARIMA(2,0,0)(1,1,0)[12] intercept : BIC=550.850, Time=0.06 sec

ARIMA(2,0,0)(1,1,1)[12] intercept : BIC=551.857, Time=0.14 sec

ARIMA(2,0,0)(1,1,2)[12] intercept : BIC=553.810, Time=0.35 sec

ARIMA(2,0,0)(2,1,0)[12] intercept : BIC=550.770, Time=0.13 sec

ARIMA(2,0,0)(2,1,1)[12] intercept : BIC=553.777, Time=0.36 sec

ARIMA(2,0,0)(3,1,0)[12] intercept : BIC=553.791, Time=0.23 sec

ARIMA(2,0,1)(0,1,0)[12] intercept : BIC=551.133, Time=0.03 sec

ARIMA(2,0,1)(0,1,1)[12] intercept : BIC=552.500, Time=0.08 sec

ARIMA(2,0,1)(0,1,2)[12] intercept : BIC=555.179, Time=0.16 sec

ARIMA(2,0,1)(1,1,0)[12] intercept : BIC=553.550, Time=0.27 sec

ARIMA(2,0,1)(1,1,1)[12] intercept : BIC=555.330, Time=1.57 sec

ARIMA(2,0,1)(2,1,0)[12] intercept : BIC=554.934, Time=0.18 sec

ARIMA(2,0,2)(0,1,0)[12] intercept : BIC=553.736, Time=0.18 sec

ARIMA(2,0,2)(0,1,1)[12] intercept : BIC=556.490, Time=0.40 sec

ARIMA(2,0,2)(1,1,0)[12] intercept : BIC=557.533, Time=0.36 sec

ARIMA(2,0,3)(0,1,0)[12] intercept : BIC=inf, Time=0.39 sec

ARIMA(3,0,0)(0,1,0)[12] intercept : BIC=551.084, Time=0.03 sec

ARIMA(3,0,0)(0,1,1)[12] intercept : BIC=552.271, Time=0.07 sec

ARIMA(3,0,0)(0,1,2)[12] intercept : BIC=554.879, Time=0.11 sec

ARIMA(3,0,0)(1,1,0)[12] intercept : BIC=553.497, Time=0.07 sec

ARIMA(3,0,0)(1,1,1)[12] intercept : BIC=555.057, Time=0.14 sec

ARIMA(3,0,0)(2,1,0)[12] intercept : BIC=554.623, Time=0.27 sec

ARIMA(3,0,1)(0,1,0)[12] intercept : BIC=553.896, Time=0.04 sec

ARIMA(3,0,1)(0,1,1)[12] intercept : BIC=555.532, Time=0.10 sec

ARIMA(3,0,1)(1,1,0)[12] intercept : BIC=556.593, Time=0.12 sec

ARIMA(3,0,2)(0,1,0)[12] intercept : BIC=558.666, Time=0.65 sec

ARIMA(4,0,0)(0,1,0)[12] intercept : BIC=552.920, Time=0.54 sec

ARIMA(4,0,0)(0,1,1)[12] intercept : BIC=555.075, Time=0.09 sec

ARIMA(4,0,0)(1,1,0)[12] intercept : BIC=555.957, Time=0.14 sec

ARIMA(4,0,1)(0,1,0)[12] intercept : BIC=555.939, Time=0.17 sec

ARIMA(5,0,0)(0,1,0)[12] intercept : BIC=inf, Time=0.37 sec

Best model: ARIMA(0,0,1)(0,1,0)[12] intercept

Total fit time: 31.329 secondsresults.summary()| Dep. Variable: | y | No. Observations: | 33 |

| Model: | SARIMAX(0, 0, 1)x(0, 1, [], 12) | Log Likelihood | -268.144 |

| Date: | Mon, 22 Apr 2024 | AIC | 542.288 |

| Time: | 17:10:16 | BIC | 545.422 |

| Sample: | 01-31-2014 | HQIC | 542.969 |

| - 09-30-2016 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

| intercept | -4801.0683 | 7.38e+04 | -0.065 | 0.948 | -1.49e+05 | 1.4e+05 |

| ma.L1 | 0.8545 | 0.665 | 1.286 | 0.199 | -0.448 | 2.157 |

| sigma2 | 8.615e+09 | 1.679 | 5.13e+09 | 0.000 | 8.62e+09 | 8.62e+09 |

| Ljung-Box (L1) (Q): | 0.02 | Jarque-Bera (JB): | 224.79 |

| Prob(Q): | 0.88 | Prob(JB): | 0.00 |

| Heteroskedasticity (H): | 28.91 | Skew: | -3.87 |

| Prob(H) (two-sided): | 0.00 | Kurtosis: | 17.03 |

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

[2] Covariance matrix is singular or near-singular, with condition number 1.23e+25. Standard errors may be unstable.

We can then use what was suggested to us by AutoARIMA.

model = SARIMAX(endog=train,

order=(1, 0, 0),

seasonal_order=(0, 1, 0, 12), # same as what has been suggested to us

trend = 'c' #the intercept

)

results = model.fit()# get the forecast, mean, and confidence intervals

forecast = results.get_prediction(start = '2017-01-31', end = '2017-12-31')

forecast_mean = forecast.predicted_mean

confidence_intervals = forecast.conf_int()plt.plot(series)

plt.plot(results.fittedvalues,

color = 'orange',

label = 'forecast')

plt.plot(forecast_mean, color = 'red')

plt.fill_between(forecast_mean.index,

confidence_intervals['lower count'],

confidence_intervals['upper count'],

color = 'pink',

alpha = 0.5)

plt.xticks(rotation = 45);

mean_squared_error(test, forecast_mean, squared = False)171857.73541525897

C:\Users\GEORGI~1\AppData\Local\Programs\Python\PYTHON~1\Lib\site-packages\sklearn\metrics\_regression.py:483: FutureWarning: 'squared' is deprecated in version 1.4 and will be removed in 1.6. To calculate the root mean squared error, use the function'root_mean_squared_error'.

warnings.warn(8.21 Prophet

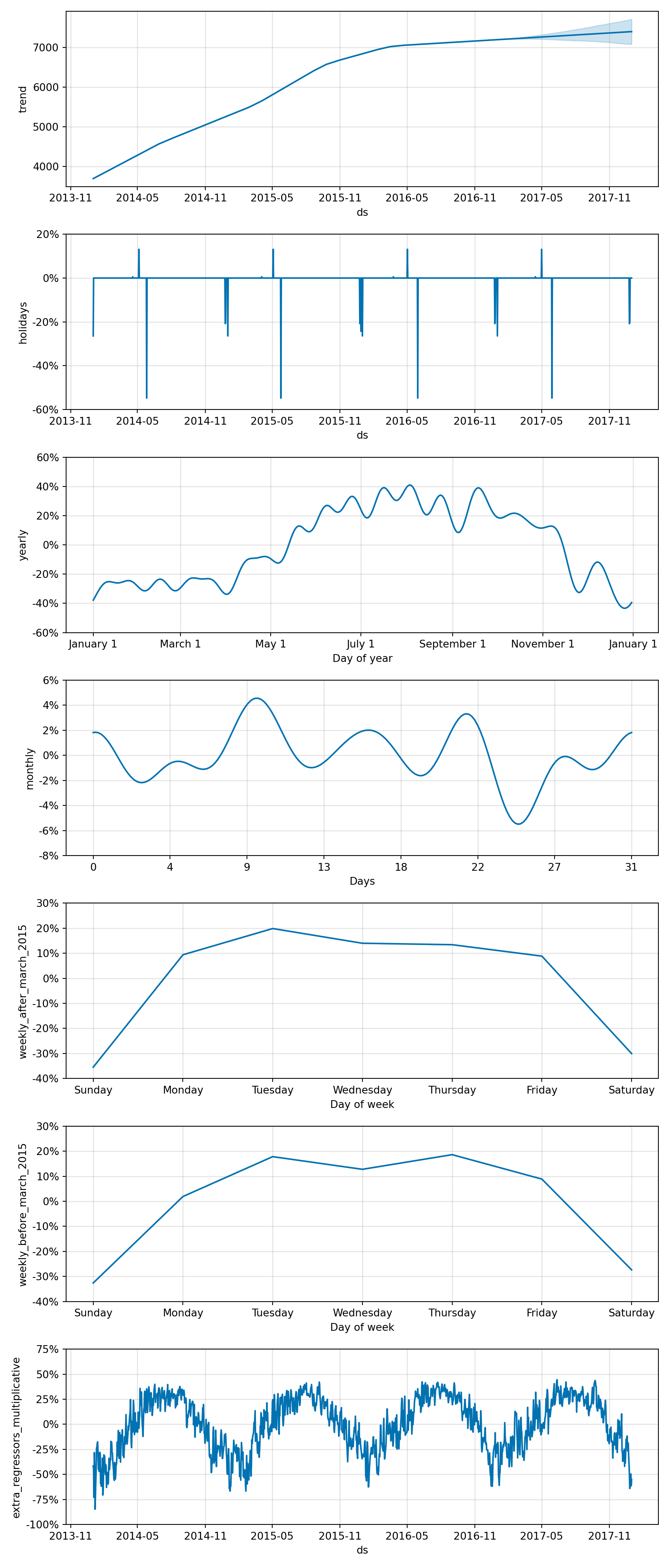

Prophet is a forecasting tool designed by Facebook’s Core Data Science team. It’s built for making forecasts for univariate time series datasets that have strong seasonal patterns and historical data. Prophet is especially useful in cases where data is affected by seasonality and other holidays or events.

The model works well with daily observations that display patterns on different time scales. It also handles missing data and trend changes well, making it robust for a variety of use cases. One of the key features of Prophet is its ability to handle the effects of holidays and special events by including them as additional regressors, thus improving the accuracy of forecasts.

8.21.1 Key Features:

- Easy to Use: Prophet requires minimal tuning and can be used straight out of the box for many forecasting tasks.

- Robust to Missing Data: It can handle missing data and outliers with little to no preprocessing.

- Flexibility: The model parameters can be easily adjusted to tune the forecast for specific needs.

- Handles Seasonality: Prophet automatically detects and forecasts seasonalities at different levels (daily, weekly, yearly).

- Holiday Effects: It can include holidays and special events, improving forecast accuracy around these times.

Prophet is based on an additive model where non-linear trends are fit with yearly, weekly, and daily seasonality, plus holiday effects.

It uses three main model components: trend, seasonality, and holidays. The trend models non-periodic changes, seasonality represents periodic changes, and holidays incorporate the effects of holidays and events.

8.21.2 Introduction to the data

# view of data

bicycles.head() starttime stoptime tripduration temperature

0 2014-06-30 23:57:00 2014-07-01 00:07:00 10.066667 68.0

1 2014-06-30 23:56:00 2014-07-01 00:00:00 4.383333 68.0

2 2014-06-30 23:33:00 2014-06-30 23:35:00 2.100000 68.0

3 2014-06-30 23:26:00 2014-07-01 00:24:00 58.016667 68.0

4 2014-06-30 23:16:00 2014-06-30 23:26:00 10.633333 68.0# information about the data

bicycles.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 9495235 entries, 0 to 9495234

Data columns (total 4 columns):

# Column Dtype

--- ------ -----

0 starttime object

1 stoptime object

2 tripduration float64

3 temperature float64

dtypes: float64(2), object(2)

memory usage: 289.8+ MB8.21.3 Data preprocessing

# convert starttime to datetime column

bicycles['starttime'] = pd.to_datetime(bicycles['starttime'], format ='%Y-%m-%d %H:%M:%S')bicycles.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 9495235 entries, 0 to 9495234

Data columns (total 4 columns):

# Column Dtype

--- ------ -----

0 starttime datetime64[ns]

1 stoptime object

2 tripduration float64

3 temperature float64

dtypes: datetime64[ns](1), float64(2), object(1)

memory usage: 289.8+ MB# create a new column which picks out date from starttime

bicycles['starttime_date'] = bicycles['starttime'].dt.date

bicycles.head() starttime stoptime ... temperature starttime_date

0 2014-06-30 23:57:00 2014-07-01 00:07:00 ... 68.0 2014-06-30

1 2014-06-30 23:56:00 2014-07-01 00:00:00 ... 68.0 2014-06-30

2 2014-06-30 23:33:00 2014-06-30 23:35:00 ... 68.0 2014-06-30

3 2014-06-30 23:26:00 2014-07-01 00:24:00 ... 68.0 2014-06-30

4 2014-06-30 23:16:00 2014-06-30 23:26:00 ... 68.0 2014-06-30

[5 rows x 5 columns]8.21.4 Resampling

# create a dataframe